The theme of the ICIEC Quarterly magazine’s Q1 2025 edition, ‘Unlocking Development Finance – The Power of Sukuk and Syndicated Murabaha’ could not be more pertinent and opportune. At a time of great uncertainties in the global geopolitical, economic and financial landscape, largely exacerbated by the US administration’s tariff rises on 2 April , decision makers in the 57 OIC member countries could do well by re-thinking their development fund raising strategies – both for sovereign and corporate debt – to urgently embrace alternative mechanisms such as Sukuk and Murabaha transactions. Mushtak Parker, Consultant Editor, considers how the Islamic finance sectors in general and the takaful-based credit and investment insurance industry in particular can enhance the synergy of these instruments with the wider trade and infrastructure sectors and help withstand macro volatilities and crises.

It has already been illustrated in an iconic paper published by then IMF economists Mohsin Khan and Abbas Mirakhor a few decades ago that in times of crises the Islamic system of financial intermediation may be in a better position to withstand the associated shocks than its conventional counterparts. Similarly, at the G20 meeting in Antalya in November 2015, the leaders in their final communiqué stressed the suitability of “alternative financing structures, including asset-based financing (namely Sukuk),” for urban regeneration and infrastructure investment, and for funding SMEs, usually the backbone of economies. It was the first time Islamic finance was so mentioned by the organisation.

Fast forward to 2023 when ICIEC, the only Shariah-compliant multilateral credit and political risk insurer in the world, member of the Islamic Development Bank (IsDB) Group, surpassed the USD100 billion landmark with a cumulative business insured since inception of USD121billion and going strong.

Sukuk Market Dynamics

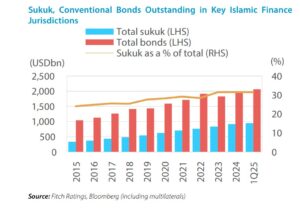

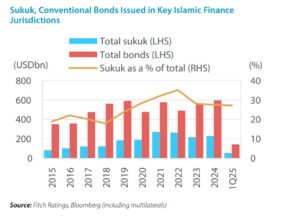

The data for the global Sukuk market is outstanding. According to Fitch Rating’s ‘Global Sukuk Market Monitor: 1Q25’, global Sukuk volumes grew by 10.8% y-o-y to USD961 billion, despite geopolitical escalations.

Going forward, Global Sukuk is set to surpass USD1 trillion outstanding in 2025, solidifying its role in OIC countries and emerging markets. Sukuk will remain a key part of the debt capital markets (DCM) in several OIC countries, and stay significant in emerging markets (EM), after representing 12% of all EM US dollar debt issued in 2024 (excluding China). However, growth could be affected by risks including Shariahcompliance requirements, geopolitical events, rising rates, and higher oil prices,” emphasises Bashar Al Natoor, Global Head of Islamic Finance at Fitch Ratings.

Sukuk were 25% of total dollar DCM issuance in the core markets of GCC countries, Malaysia, Indonesia, Türkiye, and Pakistan. ESG Sukuk reached USD44.5 billion outstanding, up 23% y-o-y.

Despite the current vagaries of the Sino-US tariff and trade war, the overall Sukuk funding environment seems favourable, driven by local demand and domestic issuance conditions. Around 28% of global Sukuk outstanding will mature in 2025–2027 with good potential of new issuances, supported by lower oil prices expected in 2025. While not their traditional funding source, Islamic banks and corporates could opportunistically diversify through Sukuk.

Sukuk Standards

AAOIFI Shariah Standard No. 62 (Draft) requires ownership transfer of the underlying sukuk assets to sukuk holders. which after initial consultations with the market will hold two final hearings in the coming months to present the draft developments. Among key proposals are the transfer of legal ownership and associated risks of the underlying Sukuk assets to the Sukuk holders, granting investors asset recourse to ensure closer adherence to Shariah principles.

“Any impact of AAOIFI Standard 62 implementation on Sukuk pricing compared to bonds,” maintains Bashar Al Natoor, “depends on the final version, which jurisdictions and entities adopt it, and, most importantly, how it is incorporated in Sukuk documentation. New Shariah-related requirements in Sukuk documents, which are not usually seen in conventional bonds, did not appear to have an impact on pricing in 2024. These includes terms in the Sukuk documentation related to asset-inspection, asset takeover, Shariah-compliant hedging, and partial payment of the periodical distribution amount in certain circumstances and for limited period.”

From a rating point of view, these factors will determine impact on Sukuk credit profiles, debt rankings, obligor IDRs, Sukuk issuance trends, issuer willingness, and market appetite. Investors however like clarity and certainty especially in policy, regulatory, accounting and legal matters. In the Islamic debt and capital market this pertains to documentation, standards and Shariah matters and governance. The question arises who regulates the Islamic Capital Market? Is it the securities regulators such as the Capital Markets Authorities or the Securities Commissions or the standard setting bodies and their Shariah advisories? The sooner the issues pertaining to AAOIFI Standard 62 are resolved the better for the market. It is not clear to what extent the regulators of those countries in which Islamic finance and Sukuk are of systemic importance are involved in the AAOIFI consultation.

Standard setting bodies and Shariah advisories are important players in the financial ecosystem and its stability and growth. All Islamic Finance standard setting bodies need to cooperate together in a synergetic framework in order to efficiently contribute to providing full transparency to the market.

No doubt, the assets ownership by the Sukuk investors substantiates the specific nature of Sukuk as an Islamic financial paper and differentiates it from the conventional Bond. It is quite expectable to witness some market resistance as it is not a familiar requirement in the conventional bonds. The gestation with the market regarding the Sharia standards is normally driven by the market players perspectives and should remain under the Islamic Finance precepts and fundamentals.

The Islamic Financial Services Board (IFSB) as the standard-setting body of regulatory and supervisory agencies that have vested interest in ensuring the soundness and stability of the Islamic financial services industry, should complement AAOIFI standards to cover this aspect. Indeed, IFSB has already issued standard 21 dealing with the Core Principles for Islamic Finance Regulation related to the Islamic Capital Market Segment. IFSB should clearly guide the financial supervisory authorities on the Sukuk structure including the required ownership transfer of the Sukuk underlying assets to the investors.

Democratising Capital Markets to Ultra Retail Investors

Two interesting trends are in democratising access to capital markets for SMEs and ultra retail investors in infrastructure related projects under financial inclusion policies. In Malaysia, for instance, Dana Infra Nasional, the infrastructure financing entity, has issued a number of Sukuk aimed at ultra retail investors which are guaranteed by the Ministry of Finance complete with tax and stamp duty remission incentives, the proceeds of which were used to fund the MRT1 Sungai Buloh-Kajang section, MRT2 Sungai Buloh-Serdang-Putrajaya section, and Phase 1 of the Pan Borneo Sarawak highway project.

Similarly, the Nigerian Debt Management Office of the Ministry of Finance in the period 2017 to 2023, has to date raised NGN 1,092.557 billion (USD1.43 billion) though six Naira-denominated Sukuk Al Ijarah issuances which are guaranteed by the Federal Government of Nigeria (FGN).

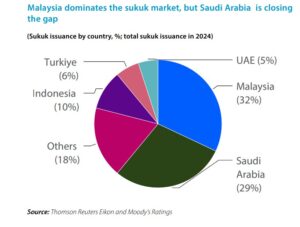

In a potentially important development in Saudi Sukuk origination, small and medium-sized enterprises (SMEs) are now turning to raise funds through small ticket Sukuk issuances. Hitherto, the preferred route to raising funds and credit facilities was through Murabaha credit facilities.

Saudi Arabia’s Rawasi Albina Investment Co. issued a 5-Year SAR50mn (USD13.3mn) in February 2025, the first in a series of riyal denominated Sukuk programme worth a total SAR500mn.

The total number of Sukuk subscriptions was 249,491 Sak, with a Bid-toCover ratio of 499.0%, and 15,991 subscribers.

Saudi multi-sector company Waja similarly issued a 2-year SAR10mn (USD2.7mn) Sukuk offering on 13 February 2025 via a private placement. The minimum subscription amount for both Sukuk transactions was pegged at SAR1,000, thus making the offering available to a wider universe of qualified retail and individual investors.

Murabaha Syndications Trend

Sukuk may yet turn out to be a preferred choice for Saudi SMEs to raise funds than even the seasoned Murabaha credit facilities which are dominated by the Kingdom’s Islamic banks and conventional banks’ Islamic banking windows.

Not that the days of Big Ticket Murabaha Syndications are numbered. On the contrary these have seen a huge proliferation in Q1 2025 with major new corporates now regularly accessing Murabaha financing in addition to Sukuk issuances as part of their fund-raising mix, which in some instances also include bond issuances and financing facility syndications. A case in point is the massive debut USD7bn Commodity Murabaha facility raised by the Public Investment Fund (PIF), the Saudi sovereign wealth fund (SWF) in January 2025.

In fact, the three main trends in the global Islamic finance market in Q1 2025 has been:

- Proliferation of Big Ticket Syndicated Murabaha transactions.

- The entry of Sovereign wealth funds into the Sukuk market.

- Sovereign Sukuk offerings continue to dominate.

Big ticket Murabaha transactions in Q1 2025 include:

A. The USD7 billion Syndicated Commodity Murabaha Facility raised by the Public Investment Fund (PIF), the sixth largest Sovereign Wealth Fund (SWF) in the world from a syndicate of 20 international, regional and local banks. The proceeds will be used to further diversify its sources of funding under its medium-term capital strategy, ensuring flexibility, competitive financing terms, and risk mitigation – initiatives which are all aligned with the Kingdom’s Vision 2030 plan.

B. The SAR3bn (USD800mn) Murabaha facility arranged by Al Rajhi Bank for Bahri, an affiliated company of the Saudi sovereign wealth fund, PIF, and a global leader in maritime transportation and logistics.

C. Renewal of an existing Murabaha credit facility amounting to SAR8.1bn (USD2.1bn) in March for Saudi Kayan Petrochemical Company by Alinma Bank, Saudi National Bank, and Banque Saudi Fransi.

D. The five-year SAR1.934bn (USD515mn) Murabaha credit facility extended by Al Rajhi Bank in February to Mobile Telecommunication Company Saudi Arabia (Zain KSA) the proceeds of which will be used to repay a current Murabaha facility with the Saudi Ministry of Finance.

E. A similar SAR2.5bn (USD670mn) Murabaha credit facility extended by Al Rajhi Bank in February to real estate developer Tatweer Company KSA) to support its expansion and development projects.

F. A USD400 million Commodity Murabaha facility for Africa Finance Corporation arranged by a consortium of 11 banks led by ADIB, Al Rajhi Bank and Emirates Islamic in February.

G. Ittihad International Investment LLC, an investment firm based in Abu Dhabi, successfully completed the arrangement of a USD450mn Islamic revolving credit facility (RCF), further strengthening its liquidity and working capital position.

H. Al Moammar Information Systems Co. (MIS), a regular user of Islamic finance facilities, renewed with amendments a 5-Year SAR1.65bn (USD440mn) Murabaha facility with Banque Saudi Fransi on 2 February 2025.

Sukuk Issuances in Q1 2025:

Perhaps the most important development is the entry of PIF in Sukuk origination, which opens huge new possibilities across the Sukuk playbook including increased Sukuk volumes and Assets Under Management thus also attracting new investor cohorts, unlocking of liquidity through secondary trading especially of AAA-rated debt paper, risk mitigation and credit enhancement opportunities.

The standout SWF Sukuk issuances in Q1 2025 include:

- The USD2.75bn dual-tranche senior unsecured Reg S Sukuk Murabaha/ Ijara issued in February by Saudi Electricity Company (SEC), majority owned by PIF.

- The maiden USD1.25bn Sukuk Ijarah/Murabaha issued by Ma’aden, the largest multi-commodity mining and metals company in the Middle East and one of the fastest growing in the world and also a subsidiary of PIF.

- The aggregate maiden USD2bn Sukuk issued by The Saudi Real Estate Refinance Company, similarly a subsidiary of the Public Investment Fund (PIF) in February.

- The National Central Cooling Company (Tabreed’s) USD500mn Sukuk Ijarah/Murabaha. Tabreed is majority owned by Abu Dhabi SWF, Mubadala Investment Company.

Similarly, the standout Sovereign Sukuk issuances in Q1 2025 include:

- Kingdom of Bahrain 7-year USD1.25bn Sukuk Ijarah/Murabaha.

- Bapco, the energy investment and development holding entity of the Government of Bahrain, issued a USD1bn Sukuk Ijarah/Murabaha.

- The Government of Ras Al Khaimah (RAK) USD1bn Sukuk Ijarah.

- The aggregate SAR9,434.322mn (USD2,515.36mn) raised in the First Quarter of 2025 by the National Debt Management Center of the Saudi Ministry of Finance through three Saudi riyal-denominated sovereign Sukuk issuances consecutively in January, February and March.

These issuances were complemented by regular Sukuk offerings by seasoned issuers in Q1 2025 such as Al Rajhi Bank (USD1.5bn AT1 Capital Sukuk), Kuwait Finance House (USD1bn Sukuk Wakala/Murabaha), First Abu Dhabi Bank (USD600mn Wakala/Murabaha), Banque Saudi Fransi (BSF) (USD750mn Wakala/Murabaha), Bank Al Jazira (SAR1bn AT1 Capital Sukuk), Riyad Bank (SAR2bn AT1 Capital Sukuk), DAMAC Real Estate Development Limited (USD750mn Sukuk Ijarah/Murabaha), Sharjah Islamic Bank (USD500mn Sukuk Ijarah/Murabaha), Aldar Investment Properties (USD500mn Green Sukuk Wakala/Murabaha), Emirates Islamic (5-year fixed rate USD750mn Sukuk Murabaha), and Arab National Bank (SAR3.35bn (USD 890mn AT1 Capital Sukuk)

By far the most proactive Sukuk issuer is the supranational IsDB which issued its first offering of 2025 in March – a USD1.75bn SOFR Public Benchmark Wakala Sukuk with a tenor of 5 years. The proceeds of this issuance will be used by the Bank continue supporting projects that deliver socio-economic growth in its 57 Member Countries and Muslim communities globally.

The projects are aligned with the Bank’s three overarching objectives under the Bank’s Realigned Strategy, i.e., (a) boosting recovery, (b) tackling poverty and building resilience, and (c) driving green economic growth.

The Way Forward

Looking ahead, the challenges are clear and present. The Sukuk market is at its most dynamic phase and the trend will continue for the next few years if not beyond. There is an urgent need for dramatically upscaling both the Sukuk market and the syndicated Murabaha market. This can be done through committed policy adoption, capacity building, technical advice, market education and synergies among the entities of the IsDB Group.

A significant development for the IsDB Group synergy and cooperation, is the signing of a landmark Documentary Credit Insurance Policy (DCIP) agreement on 2 March 2025 between ICIEC, and ITFC. “The policy will provide critical coverage for ITFC transactions, enhancing trade confidence and facilitating smoother financial operations in global trade involving Shariah-compliant products and services, thereby benefiting the broader economic landscape of the member states. It is designed to provide ITFC with a comprehensive risk management tool to safeguard its LCs Confirmation transactions,” explained Dr. Khalid Khalafalla, CEO of ICIEC.

ICIEC as a risk absorber and mitigator has an impressive business development and risk underwriting record for transactions whether Murabaha facilities, or lines of financing or any other such trade and project financing facilities, very often successfully crowding in private sector funding and making transactions and projects both ‘bankable’ and ‘affordable’.

The importance and efficacy of ICIEC risk mitigation and credit enhancement for its member states cannot be underestimated. Indeed, through its dedicated Sukuk Insurance Policy (SIP), ICIEC is willing to help sovereign Sukuk origination in member states especially those unrated or rated below investment grade, which has since also been refined and expanded into Green Sukuk Insurance Policy as Risk Mitigation, Credit Enhancement and Shariah-Compliant Third-Party Guarantee Solutions.

Therefore, the IsDB Group including a Shariah-Compliant Third-Party Guarantor, such as ICIEC is in a unique position to act as a market maker and help attract a new cohort of potential investors in member country sovereign Sukuk, especially the low-and-medium-incomecountries (LMICs). The knock-on effect could be positive through greater involvement in helping to develop the Islamic Capital Market in LMICs, and in the process dispel the biased, over valuation and hype of sovereign risk metrics about LMICs harboured by the major international credit rating agencies.