There are changing times in the global economy where no country is immune from their potentially disruptive consequences, which continue to unfold in the global trade, tariffs, and foreign direct investment (FDI) playbook. The order of the day seems to be fragmentation and reciprocity. For the credit and investment insurance industry, it means navigating new risks, but also new opportunities. Dr. Khalid Khalafalla, the CEO of ICIEC, surveys the cornucopia of current and future trends credit and political risk insurers must consider and how the industry, including ICIEC, is responding to the challenges and opportunities ahead.

Out of adversity from the uncertainties and disruptions in the ever evolving global economic, financial, and geopolitical landscape comes a remarkable propensity towards innovative out-of-the-box thinking as the credit and political risk insurance and guarantees industry become no exception.

In fact, it has doubled down in various facets with a dogged resilience, determination, and operational agility, which augurs well for the near-to-medium-term future of the industry.

The Berne Union (BU)’s Export Credit & Investment Insurance Industry Report 2024, unveiled at its Spring meeting in Dubrovnik in May 2025, for instance, reports that the new business underwritten by its members – including ICIEC in 2024, reached a record USD3.3 trillion directly supporting cross-border trade and investment. This was especially so for short-term Trade Credit Insurance (CTI) and political risk insurance (PRI), which increased year-on-year by 7% and 5%, respectively.

But beyond inherited legacy insurance models, the new playbook is already redefining and recalibrating risk metrics and approaches, including those relating to country risk, sovereign debt, and export credit and investment structures.

There is also the issue of emerging insurance taxonomies, such as the EU’s Omnibus 1 Package, aimed at helping Member States in their transition to a sustainable economy and ensuring the insurance sector is aligned with the EU climate goals and protecting financial stability.

While a proactive approach to navigating geopolitics is essential for businesses to thrive, especially in going beyond merely mitigating geopolitical risks to seizing the opportunities presented by the new world trade and investment order, they still need to contend with the manifold macroeconomic and industry trends that will impact the insurance sector in varying ways. These trends include:

1. According to Swiss Re Institute’s World Insurance Sigma Report, the global GDP growth (inflation adjusted) is expected to slow to 2.3% in 2025 and 2.4% in 2026 from 2.8% in 2024, and accordingly the global insurance industry is expected to follow the trend, with total premiums expected to slow to 2% this year from 5.2% in 2024, picking up marginally to 2.3% in 2026.

2. In the UK, the Financial Conduct Authority (FCA) is championing a more agile regulatory environment for financial services, including insurance, to become an engine for sustainable, innovation-led growth. The financial sector contributes over 8% of the UK’s GDP and represents a significant source of employment and trade. Regulation is seen as a growth catalyst, also encompassing a data-driven look at the evolving architecture of financial risk.

3. Sovereign credit ratings and OECD country risk classifications also exert a heavy influence on the ability of low-and-medium-income countries to access capital, influencing borrowing costs and investor appetites, a point that many ICIEC Member States have stressed is based on exaggerated perceptions of credit and country risk, legacy debt burdens, and short-term macro indicators, which in turn leads to higher costs of financing, including credit insurance and PRI premiums.

4. Electronic trade documentation and digitalisation facilitation, including in the insurance sector, according to a new study by UNCTAD, shows that countries continue to make progress in easing and digitising trade processes. The 6th UN Global Survey on Digital and Sustainable Trade Facilitation, conducted across 160 economies by UNCTAD, confirms that the global average implementation rate of trade facilitation measures currently stands at 72%, up from 68.6% in 2023. The survey shows improvements across all regions since 2023, with developed economies leading with an 86% implementation rate.

5. In fact, UNCTAD’s latest update reveals that global trade expanded by an estimated USD300 billion in H1 of 2025, despite a slower pace of growth, compared to a rise in global trade by about 1.5% in Q1, with a growth expected to accelerate to 2% in Q2.

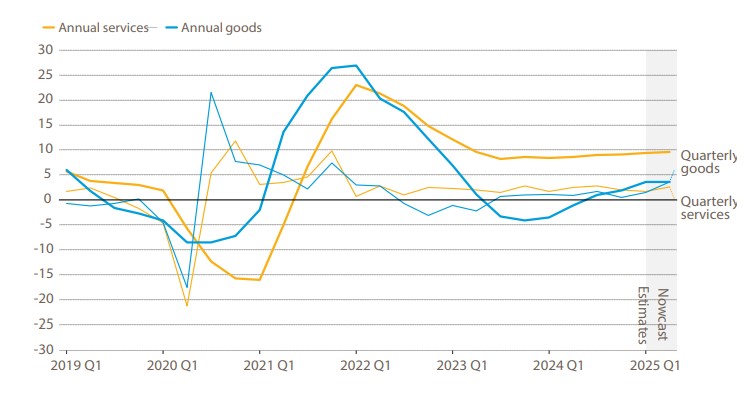

Global trade in goods and services remains strong in the first half of 2025

Annual and quarterly growth in the value of trade in goods and services, 2019–2025 Q1

Note: Quarterly growth is the quarter over quarter growth rate of seasonally adjusted values.

Annual growth is calculated using a trade-weighted moving average over the past four quarters.

Figures for Q1 2025 are estimates. Q2 2025 is a nowcast as of 17 June 2025.

Trade in services remained the main engine of annual growth, rising 9% over the last four quarters. Price increases contributed to the overall rise in trade value. Prices for traded goods edged up in Q1 and are likely to continue to rise in Q2, while trade volumes grew by just 1%.

Developed economies outpaced developing countries in Q1, reversing recent trends that had favoured the Global South. South-South trade stagnated overall, though Africa bucked the trend with exports up 5% and intraregional trade growing 16% year on year.

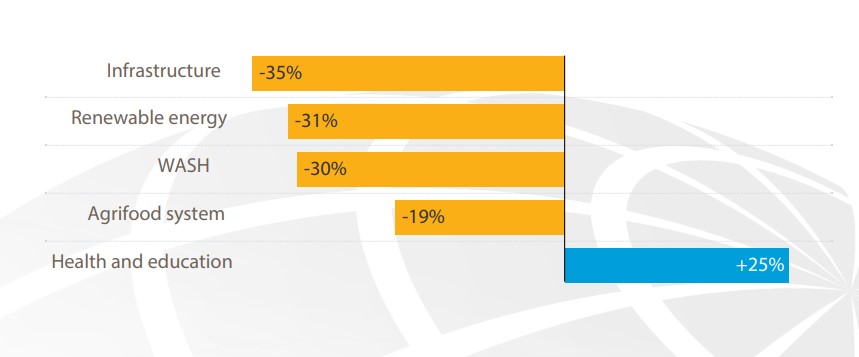

6. Similarly, global foreign direct investment (FDI) fell by 11%, marking the second consecutive year of decline and confirming a deepening slowdown in productive capital flows, according to the World Investment Report 2025, released by UNCTAD in June. Although global FDI rose by 4% in 2024 to USD1.5 trillion, the increase is the result of—among other factors—volatile financial conduit flows through several European economies, which often serve as transfer points for investments. The drop was especially steep in sectors critical to achieving the Sustainable Development Goals: renewable energy (-31%), transport (-32%), and water and sanitation (-30%).

Foreign investment in sustainable development fell sharply in 2024

International Investment in developing economies in Sustainable Development Goal sectors, percentage change of project values, 2023-2024

Note: WASH stands for water, sanitation, and hygiene

7. The credit and investment insurance preparedness playbook now encompasses several additional emerging trends. These include:

i. Digital resilience with agility by design, compliance, and automation all embedded. The bedrock remains collaboration in real time since risk, underwriting, and claims functions access the same data.

ii. In the dramatic rise in the resort to Artificial Intelligence (AI), the consensus seems to be that not every AI breakthrough warrants adoption. Insurers should focus on what delivers operational relevance and measurable added value.

iii. ECA collaboration is essential to accelerating project development and ensuring long-term resilience in critical mineral supply.

iv. The green energy industry and net zero momentum faced headwinds in 2024 from geopolitical tensions, trade barriers, and rising costs. While investments continue apace across sectors like wind, solar, and electrified transport, profitability and policy hurdles remain.

v. Rising debt burdens and tightening financing conditions are increasing pressure on low-income countries. Restructuring frameworks must now deliver greater coordination, clarity, and long-term sustainability, including possible write-offs.

vi. The Credit and Investment Insurance industry is similarly faced with rising fraud and AML/CTF risks, and fictitious trades and trade credit insurance claims are on the rise.

vii. The role of trade credit insurance in supporting SMEs, the backbone of economies worldwide, as governments are actively developing policies to support SMEs as a way of boosting productivity, innovation, and growth, albeit cost and margin management remain.

Perhaps the most interesting development emerged at the 4th International Conference on Financing for Development (FfD4), where global leaders addressed the widening gap between capital flows and development needs. The BU, UNCTAD, and the International Chamber of Commerce (ICC) convened a side event on ‘enhancing de-risking mechanisms for sustainable development’ to discuss how export credit guarantees, and political risk insurance (PRI) can be further leveraged to channel flows of long-term capital into developing economies and achieve sustainable economic development.

According to the BU, credit insurance and guarantees—both export-linked and untied—mitigate non-payment and political risks, enabling financiers to offer long-term financing for projects in developing countries that otherwise would not be feasible. These instruments support blended finance structures and improve access to affordable funding, especially in developing economies, making it possible for commercial banks to lend for renewable energy, health infrastructure, or public transport projects with reduced risk exposure. In fact, BU members currently hold USD507 billion in exposure in developing economies, a figure that has grown steadily since 2010 (USD323 billion). Within Least Developed Countries (LDCs), this figure has surged from USD15.9 billion in 2010 to nearly USD98 billion in 2024, demonstrating an increasing willingness to support the poorest countries.

UNCTAD at the FfD4 launched a policy review titled “Derisking investment for the SDGs: The role of political risk insurance.” Among investment derisking instruments, PRI, a type of insurance that protects cross-border investments from losses due to political events, such as expropriation, political violence, currency inconvertibility and breach of contract, has a critical and potentially growing role to play in fostering investment towards developing countries in general and LDCs in particular.

According to the Review, “PRI providers insured projects worth about USD150 billion in developing countries, including LDCs between 2018 and 2022. Developing countries (excluding LDCs) are the largest PRI beneficiaries (70% of the projects), where LDCs account for only 15% of projects covered by PRI. However, insured project values are equivalent to 28% FDI to LDCs, compared to 6% in other developing countries and 2% in developed countries. Export credit agencies (ECAs) are the primary providers of PRI, accounting for 78% of total issuance over the past decade, while multilateral institutions and private insurers account for 7% and 15%, respectively. Asia accounts for the largest share of PRI provided by ECAs and private insurers, reflecting China’s dual role as a major recipient of PRI and a leading provider, while Africa receives the most PRI from multilateral institutions.”

The investment gap to achieve the UN SDGs in developing countries by 2030, says UNCTAD, has widened from USD2.5 trillion to about USD4 trillion per year between 2014 and 2023. This chasm underscores the urgent need for effective solutions. The consensus is that public resources alone, including official development assistance, will be insufficient for bridging the financing gap, since mobilising private sector finance is critical, with a vital role for FDI to play.

The SDGs, in fact, have been a central tenet of ICIEC’s operations since they were introduced in 2015. We believe that trade and investment facilitation is an effective vehicle by which the SDGs could be achieved, as we are committed to supporting sustainable development, investing, and the SDGs. In this respect, ICIEC actively targets real impact and change in all its insured operations and acts as a catalyst for private sector capital mobilisation to be directed towards achieving the SDGs. This is done through ICIEC’s unique Shariah-compliant de-risking solutions, including the Non-Honouring of Sovereign Financial Obligations (NHSFO) Policy, the Foreign Investment Insurance Policy, Equity Investment Policy, and Reinsurance. This is achieved through forging Partnerships for Change in line with SDG 17 and with ICIEC’s Theory of Change strategy.