Chief Executive Officer, ICIEC

Mobilising private sector finance remains a critical requirement for sustaining development outcomes, with foreign direct investment playing a central role. Yet private investment in developing economies, particularly in least developed countries (LDCs), continues to be constrained by elevated real and perceived risks. Over the period 2015-2023, foreign direct investment flows recorded only modest growth of approximately 17 per cent in developing countries excluding LDCs, while declining by nearly 20 per cent in LDCs, underscoring persistent structural and risk-related barriers to capital mobilisation (UNCTAD, 2025).

The OECD recently highlighted that emerging markets and developing economies (EMDEs) are confronted with a historic annual investment requirement of USD 7.5 trillion to promote economic growth, reduce poverty and realise the broader Sustainable Development Goals (SDGs). Although publicly financed investments are essential, substantial evidence shows that private capital must provide the majority of resources needed to close this gap (OECD, 2025). However, elevated risk perceptions and high financing costs remain among the key deterrents for private investors, limiting the flow of long-term capital into priority sectors.

Additionally, macroeconomic and political instability, ineffective operations, and financial constraints remain major barriers that fuel protectionist policies, disrupt trade flows, and exacerbate supply-chain vulnerabilities (UNCTAD, 2025). As uncertainty increases, investors typically respond by demanding higher risk premiums, shortening loan maturities, or withdrawing from markets altogether, which directly raises the cost of finance for sovereigns and private borrowers alike.

These overlapping challenges emphasize the need for sophisticated risk-mitigating mechanisms such as political risk insurance (PRI) to facilitate long-term investment in fragile contexts. By covering risks such as expropriation, breach of contract, currency inconvertibility, and political instability and conflict-related disruptions, PRI reduces exposure to non-commercial risks that private investors are often unable or unwilling to absorb on their own. Export Credit Agencies (ECAs) as well as credit insurers operate on established pricing models, and credit and political risk insurance helps make projects bankable by enabling longer tenors, improving borrowing terms, and mobilising private funds. In the absence of such risk coverage, lenders often reduce exposure, impose shorter maturities, or increase pricing to levels that undermine project viability, particularly in high-risk environments.

Over recent years, analytical evidence has increasingly validated the role of political risk insurance in mitigating cost-of-capital challenges in developing economies. In 2022, an independent study by S&P Global and Marsh Specialty demonstrated that PRI can materially reduce country risk premiums by addressing specific non-commercial risks that are otherwise embedded in investors’ required returns. By quantifying how insurance coverage stabilises projected cash flows and improves valuation metrics, the study challenges the long-held perception of PRI as merely an added cost. Instead, it shows that effective risk transfer can enhance project viability and financing terms, particularly when perceived country risk weighs heavily on investment decisions.

In light of this context, lowering the overall cost of finance through PRI can therefore be achieved, in part, through coordinated partnerships with Multilateral Development Banks (MDBs), development institutions, and the private insurance and reinsurance market. As emphasized by UNCTAD, PRI constitutes a critical policy-relevant instrument for mitigating non-commercial risks and mobilising foreign direct investment. This pattern is particularly evident in low-income and fragile economies, where effective utilisation of PRI can significantly enhance investment viability and accelerate progress toward the SDGs.

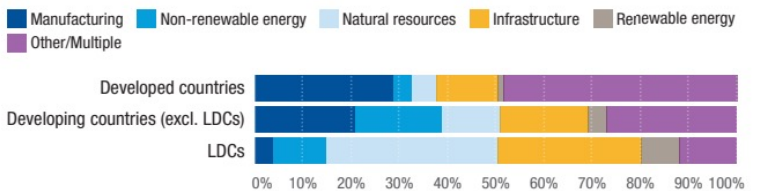

Sectoral composition of political risk insurance (PRI) coverage differs markedly across countries at different stages of development. In developing countries excluding LDCs, the distribution of PRI coverage becomes more balanced across sectors. While manufacturing and energy projects remain important, there is a growing share of coverage directed toward natural resources and infrastructure, reflecting higher investment. For many low- and middle-income economies, elevated financing costs continue to represent a binding constraint on trade, investment, and infrastructure development. In LDCs, PRI coverage is heavily concentrated in infrastructure and natural resource projects, with a relatively small share allocated to manufacturing. Such concentration reflects the structure of investment opportunities in LDCs, but also the heightened perception of risk, and thus financial costs, associated with long-gestation projects that are critical for development. These costs are shaped by a combination of global financial conditions, sovereign credit assessments, and prevailing risk perceptions, which together restrict access to affordable and sustainable capital flows. Addressing these constraints requires coordinated partnerships capable of mitigating structural barriers, reallocating risk, and expanding the availability of finance, thereby supporting sustained growth in trade and productive investment.

As the hurdle of excessive financing costs remains a systemic barrier to development, ICIEC has been working towards mitigating these constraints through a comprehensive approach that extends beyond direct underwriting.

As the hurdle of excessive financing costs remains a systemic barrier to development, ICIEC has been working towards mitigating these constraints through a comprehensive approach that extends beyond direct underwriting. Supported by its strong credit standing, ICIEC acts as a catalyst for mobilising additional capacity across low- and middle-income Member States (MSs). By pooling resources and sharing risks, ICIEC helps expand financing availability, facilitate longer tenors, and secure more appropriate pricing for MSs.

ICIEC’s partnerships generate added value through coordinated action, aligned objectives, and integrated approaches that support inclusive and balanced sustainable development. The agreement signed in October 2025 with Afreximbank is an example of such partnerships that will reinforce momentum toward deeper Arab-African economic integration and enable MSs (particularly low- and middle-income countries) to leverage innovative financial instruments, shared expertise, and coordinated development strategies to participate more effectively in regional and global value chains.

Looking ahead, reducing financing costs in developing and least developed countries will depend less on the availability of capital and more on the effective allocation and mitigation of risk. As global uncertainty persists, mobilising private investment at scale will require coordinated action that strengthens investor confidence, extends maturities, and improves pricing through targeted risk-sharing mechanisms. Political risk insurance, blended finance structures, and partnerships with Multilateral Development Banks and development institutions are no longer complementary tools, but central pillars of sustainable financing strategies in high-risk environments. ICIEC will continue to play a focused role within this ecosystem, convening capacity and partnerships across public and private stakeholders to crowd in private capital where it is most needed. Through deeper collaboration with the IsDB Group, regional financial institutions, and global insurers and reinsurers, ICIEC is committed to enabling affordable, long-term, and de-risked financing for MSs. Such solutions will help unlock resilient investment flows that will generate tangible development outcomes and sustain progress toward Sustainable Development Goals.