An Economy Undergoing Profound Structural Reforms and Transition How Nigeria Can Unleash Its Economic Potential

Economic Overview

Nigeria, Africa’s most populous nation and 4th largest economy by purchasing power parity, is undergoing a profound economic transition driven by structural reforms, rebalancing of fiscal policy, and renewed efforts to restore macroeconomic stability. The Government has embarked on a bold reform agenda aimed at reversing years of underperformance caused by oil dependence, fiscal leakages, and currency market distortions.

The Government focuses on large-scale privatization and asset sales as part of its economic stabilization measures. These measures aim to address balance-of-payment stresses and stabilize the economy.

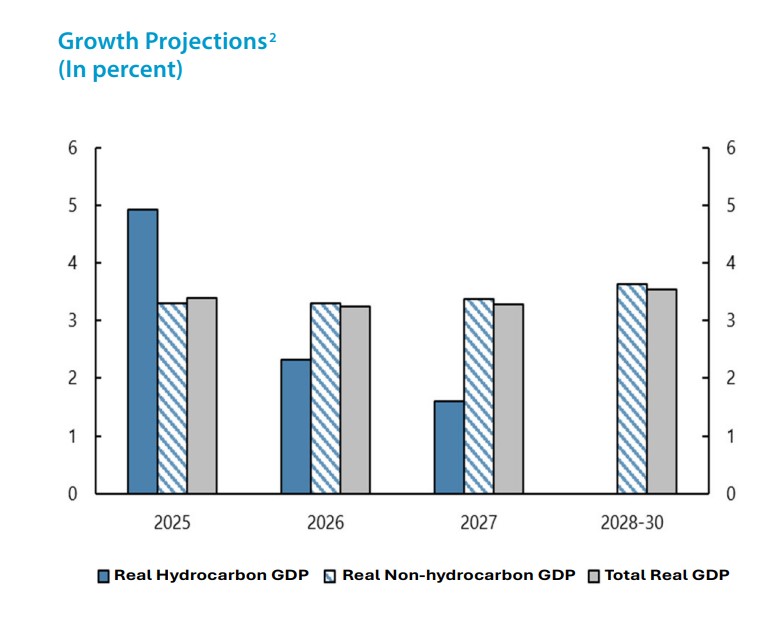

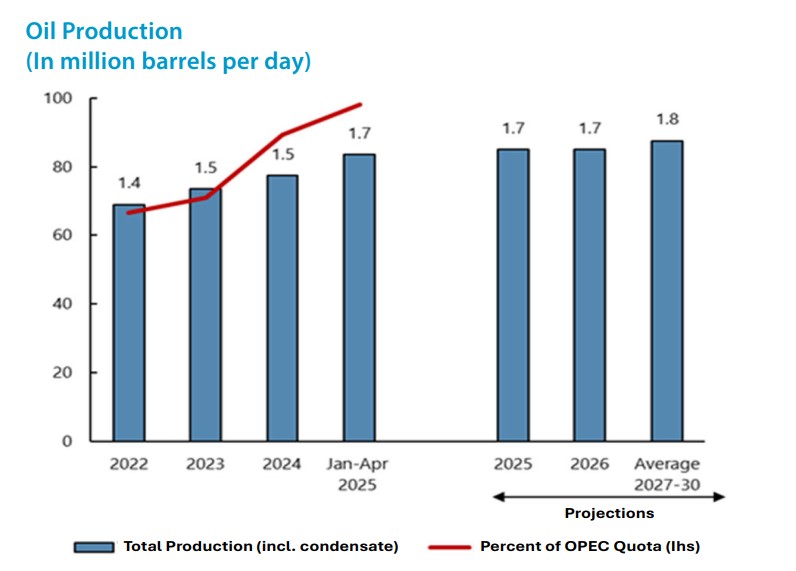

According to the Central Bank of Nigeria (CBN), the economy is projected to grow by 4.17% in 2025, up from an estimated 2.9% in 2024. The International Monetary Fund (IMF) is slightly more conservative, forecasting 3.0% real GDP growth. Growth is supported by higher oil production volumes (approaching 1.6 million barrels/day), the full commissioning of the Dangote Refinery, improved FX liquidity, and rising non-oil sector contributions – particularly in agriculture, telecommunications, construction, and financial services.

Public investment is being catalysed by high-profile infrastructure projects, including the Lagos–Calabar Coastal Highway, rail line modernizations, and rural electrification schemes. The government also seeks to drive job creation through domestic value chains in agriculture, automotive assembly, and pharmaceuticals under its “Renewed Hope” economic agenda.

Nigeria does not currently have a formal IMF programme (such as an EFF or SBA), but maintains active engagement through technical consultations, surveillance missions, and Article IV assessments. The 2024 Article IV Consultation recognized the boldness of Nigeria’s initial reform momentum including fuel subsidy removal and FX liberalization but also warned of reform fatigue, inflation risks, and the need for better-targeted social safety nets.

While Nigeria has not pursued budgetary support from the IMF, it continues to draw on IMF policy advice to guide fiscal consolidation and monetary tightening. The IMF’s Debt Sustainability Analysis (DSA) rated Nigeria’s debt as sustainable but vulnerable to interest and exchange rate shocks, underscoring the importance of revenue mobilization and FX inflow management.

Nigeria remains a significant client of the International Development Association (IDA) and the International Bank for Reconstruction and Development (IBRD) and is implementing a wide range of Results-Based Financing (RBF) operations across education, power, social protection, and state-level reforms. One of the most notable developments in early 2025 is Nigeria’s decision to prepay USD500 million of its outstanding World Bank debt.

This prepayment is politically and economically significant as it reflects the renewed FX inflows and stronger fiscal buffers due to higher oil revenues and improved investor sentiment. It is designed to reduce debt service burden over the 2025–2027 period, freeing space for critical capital expenditures and potential market issuances (e.g., Sukuk). It also sends a positive signal to credit rating agencies and international capital markets, reinforcing Nigeria’s commitment to prudent debt management.

Ultimately and according to internal reports from the Federal Ministry of Finance and the DMO, the prepayment is also aligned with Nigeria’s broader Debt Management Strategy (2024–2027), which prioritizes:

1. Extending average debt maturities.

2. Increasing concessional debt-to-commercial debt ratios.

3. Using guaranteed and insured market instruments to access affordable long-term capital.

It is worth noting that in April 2025, Fitch Ratings upgraded Nigeria’s Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘B’ from ‘B-’ citing improved FX reserve buffers, strengthened fiscal management and fuel subsidy removal and stabilized and transparent exchange rate system through implementation of Bloomberg B-Matching System, progress in reducing inflation and rebuilding investor confidence.

Tackling Inflation

Nigeria faced intense inflationary pressure throughout 2023 and early 2024 due to subsidy reforms, FX devaluation, and food supply shocks. Headline inflation peaked at 34.8% in December 2024, before gradually easing to 24.48% in January 2025, driven by tighter monetary policy and relative currency stabilization. The IMF projects average inflation at 26.5% for 2025. The Monetary Policy Rate (MPR) currently stands at 24.75%, following successive hikes by the CBN’s Monetary Policy Committee to combat price instability.

The naira has seen reduced volatility after the unification of multiple exchange rates in mid-2023, with a more market-reflective FX window now in place. CBN has prioritized clearing its FX backlog and restoring investor confidence in the I&E window.

Current Account Situation

Nigeria has recorded a notable improvement in its current account position since 2023, marking a significant turnaround in its external balance sheet. In 2024, the country achieved a current account surplus of approximately USD6.83 billion, according to data from the CBN. This is a marked reversal from the USD3.3 billion deficit recorded in 2023.

This improvement was largely driven by a USD13.17 billion trade surplus, underpinned by robust oil exports and a sharp reduction in fuel import bills. Additionally, remittance inflows surged to USD20.9 billion in 2024, representing an 8.9% year-on-year increase. While service account deficits persisted, they narrowed compared to previous years, contributing modestly to the overall improvement.

On a quarterly basis, the current account surplus expanded from USD3.38 billion in Q1 2024 to USD5.14 billion in Q2 2024, reflecting stronger oil receipts, improved non-oil exports, and moderate import growth. Looking ahead, the IMF projects that the current account surplus will moderate, falling from 9.1% of GDP in 2024 to 6.9% in 2025, and further down to 5.2% in 2026, as oil prices stabilize and imports gradually pick up.

Foreign Exchange Liquidity

Foreign exchange (FX) liquidity in Nigeria has improved significantly since mid-2023, following the Central Bank of Nigeria’s decision to unify the multiple exchange rate windows and allow the naira to trade more freely under a managed float system.

This reform—implemented in June 2023—reversed years of rigid FX policies and was one of the most critical components of the new administration’s economic stabilization agenda. In the months following the reform, Nigeria faced acute FX shortages and volatile exchange rate movements, with the naira depreciating sharply in both official and parallel markets.

However, by early 2024, FX market conditions began to stabilize, supported by improved supply from oil exports, higher remittance inflows, and increased portfolio investment. CBN also undertook clearing of the FX backlog, estimated to be over USD6 billion in Q3 2023, with most of the backlog fully repaid by April 2024. This was a critical confidence-building measure for investors and foreign suppliers, many of whom had been waiting for months to repatriate funds or receive payments.

As of May 2025, Nigeria’s gross foreign reserves are estimated at approximately USD38.45 billion, up from USD33.1 billion in mid-2024. Net reserves, after accounting for swaps, forwards, and encumbrances, stood at USD23.11 billion at the end of 2024. The increase in reserves has been attributed to a combination of higher oil revenues, reduced fuel import costs, and inflows from Eurobond repayments, World Bank disbursements, and limited FX interventions by CBN.

To further deepen FX liquidity, the CBN has reintroduced and strengthened the “Willing Buyer, Willing Seller” window, allowing exporters, investors, and banks to set rates more transparently. The gap between the Investors’ and Exporters’ (I&E) window and the parallel market has narrowed considerably in 2025, declining from a peak of over 30% to below 10%, indicating increased confidence in the formal market.

Furthermore, FX turnover on the Nigerian Autonomous Foreign Exchange Market (NAFEM) has improved, with average daily trading volumes now surpassing USD200 million, compared to just USD75– USD100 million at the height of the FX crisis in 2023. The return of foreign portfolio investors to the Nigerian debt and equity markets – following the clearance of backlogs and interest rate normalization—has also provided fresh FX supply into the system.

However, despite these positive developments, structural FX demand pressures remain, especially for capital goods, refined fuel, and machinery. The government’s push for local production and import substitution under the Industrial Revitalization Roadmap, as well as the start of operations at the Dangote Refinery and other industrial zones, are expected to reduce long-term FX demand.

Debt Sustainability

The International Monetary Fund (IMF) concluded its 2024 Article IV Consultation with Nigeria in April 2024, providing a comprehensive assessment of the country’s economic landscape and debt sustainability. The IMF acknowledged the Nigerian government’s ambitious reform agenda aimed at restoring macroeconomic stability and promoting inclusive growth.

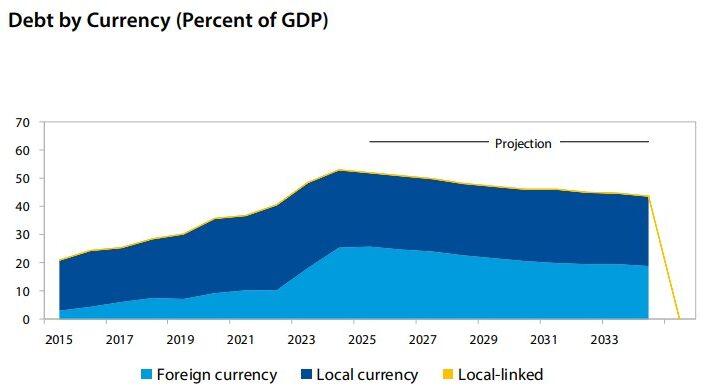

Nigeria’s public debt increased to approximately 46% of GDP by the end of 2023, largely due to the depreciation of the naira. While this debt level remains below the regional average for Sub-Saharan Africa, the burden of debt servicing has intensified. External debt accounts for roughly 16% of GDP and is primarily concessional, limiting exposure to commercial external risks. However, the country’s debt portfolio is heavily skewed toward domestic borrowing, which comes at high interest rates and presents rollover and cost-related challenges.

Nigeria: Public Debt Structure Indicators

Nigeria’s Active Cooperation with the IsDB Group

Nigeria is a significant and active member of the Islamic Development Bank (IsDB), having joined the institution on 3 November 1999. To date, Nigeria holds a capital subscription of ID4,298.51 million, representing 7.33% of total IsDB subscribed capital, making it the fifth largest shareholder in the Bank. The IsDB maintains a strong operational footprint in the country through its Regional Hub in Abuja, established in 2018, which also oversees development interventions in neighbouring West African states.

Nigeria has benefited from a wide-ranging IsDB Group portfolio, with more than 145 projects approved. Out of this, around 60% have been completed, covering critical sectors such as infrastructure, agriculture, education, and finance. The infrastructure sector alone accounts for over 89% of IsDB’s total financing in Nigeria, encompassing sub-sectors like transportation, water and sanitation, energy, information and communications, and urban development.

The Bank’s financing has been notably directed toward key national development priorities, with major investments in agriculture, education, finance and health, industry, and mining. IsDB Group entities have been active in Nigeria.

Since inception, the IsDB Group has approved a total funding of about USD2.2 billion for Nigeria. This includes USD1.24 billion in project financing by IsDB, USD333 million supported by ICD; USD537 million trade operations by ITFC, and USD90 million by other IsDB Group funds and operations.

Nigeria’s Special Relationship with ICIEC

Nigeria joined ICIEC in 2006, and since then the Corporation has insured over USD2 billion in cumulative transactions in Nigeria, historically focused on trade risk cover for Tier 1 banks. ICIEC is now expanding from traditional short-term trade finance to long-term investment guarantees and sovereign risk coverage. Since this shift, we were able to build up a comprehensive pipeline of transactions in several areas, including Islamic capital market instruments, as well as enhanced partnership with key local stakeholders.

ICIEC has successfully participated in the following initiatives and transactions:

- At the 2025 IsDB Group Annual Meetings in Algiers in May, ICIEC signed a strategic Memorandum of Understanding with NEXIM Bank, establishing a framework for collaboration in export credit insurance, reinsurance, joint product development, and institutional capacity building. The partnership aims to expand risk mitigation tools for Nigerian exporters and deepen NEXIM’s integration into the global Islamic insurance architecture.

- In 2024, ICIEC closed its first-of-its-kind sovereign-backed SOE (State Owned Enterprise) cover in Africa through Project Gazelle, a structured pre-export finance (PXF) transaction in favour of the Nigerian National Petroleum Company (NNPC). The cover mitigates payment risk while enabling NNPC to raise international financing based on its crude oil flows..

- Following the success of Project Gazelle, ICIEC has replicated this model through Project Leopard, which closed in 2025. Both transactions underscore ICIEC’s ability to innovate in complex structured trade finance and support national champions like NNPC through Shariah compliant risk mitigation..

- The Lagos-Calabar Coastal Highway, valued at USD1.067 billion (Phase 1 only), is backed by USD465.9 million in ICIEC insurance provided to major banks under a 7-year Islamic Murabaha structure with NHSFO cover. As ICIEC’s first sovereign NHSFO cover in Nigeria, the project is a milestone in regional infrastructure financing. It supports job creation, improves coastal connectivity, reduces travel time, and aligns with SDGs 8, 9, 11, and 13.