COUNTRY MANAGER, ASIA REGION

Bridging Markets and Mitigating Risks in the CIS Region

Since joining ICIEC in July 2023, I have focused on driving business initiatives across the CIS region, particularly in Kazakhstan, Uzbekistan, Azerbaijan, and Turkmenistan. In this role, I am dedicated to attracting Foreign Direct Investment (FDI) and facilitating vital trade and investment transactions. By strategically mitigating political and commercial risks, I help our partners navigate complex markets while fostering sustainable economic growth and regional cooperation.

My interest in development finance and risk mitigation stems from a longstanding passion for enabling cross-border investments in emerging markets. Having spent more than a decade in Kazakhstan’s financial sector, I have witnessed firsthand how access to innovative financial solutions can unlock investor confidence and accelerate economic transformation. This experience shaped my belief that risk mitigation is not simply a protective mechanism, but an enabler of growth and long-term development.

I am a results-oriented professional with over a decade of experience in credit analysis, asset management, and risk management, and I earned my CFA charter in 2016. My professional foundation is deeply rooted in corporate banking, where I led Corporate Business divisions and specialized in structuring and financing large-scale projects across sectors such as energy, mining, and FMCG. Throughout my career, I have also held leadership positions in risk management, including roles at an investment brokerage and the National Mortgage Company of Kazakhstan, which gave me a comprehensive perspective on financial modeling, deal structuring, and trade finance instruments.

Joining ICIEC was a natural next step in my professional journey, as it brought together my expertise in financial risk management with a broader development mandate. I was particularly drawn to ICIEC’s mission of supporting trade and investment flows in markets with strong economic potential, yet often underserved by political and commercial risk insurance solutions.

The Central Asia and Azerbaijan markets are dynamic and full of opportunity, particularly in infrastructure, energy, logistics, and industrial development. However, many investors remain cautious due to perceived market risks and limited awareness of available risk mitigation tools. This creates both a challenge and an opportunity: building trust, educating the market, and demonstrating how investment insurance and export credit solutions can support sustainable business growth.

In my daily work at ICIEC, I collaborate closely with colleagues across our global hubs and headquarters to promote our solutions and expand investment activity in Central Asia and Azerbaijan. Because investment insurance and export credit remain relatively new concepts in the region, a significant part of my role involves market education, stakeholder engagement, and raising awareness of Islamic finance solutions.

To achieve this, I work with a broad range of partners, including state-owned enterprises, private sector companies, financial institutions, and exporters involved in regional investment projects. My objective is to ensure that our initiatives are impactful, commercially viable, and sustainable in the long term. Beyond insurance solutions, I am equally committed to strengthening the visibility of the IsDB Group across the region. I believe that closer collaboration with sister entities, particularly ICD in private sector development, can significantly amplify our collective impact.

As Country Manager for the region, I am also focused on diversifying ICIEC’s project portfolio to ensure our presence extends beyond the banking sector into large-scale infrastructure projects. While infrastructure transactions are inherently more complex and require longer execution timelines, institutions such as ICIEC have a critical role to play in enabling these transformational investments by providing the necessary risk mitigation framework. Beyond their economic impact, such projects also contribute to the professional growth of our teams, allowing us to strengthen our expertise, build institutional knowledge, and leverage these experiences to support even more ambitious initiatives in the future.

Looking ahead, I remain optimistic about the continued expansion of ICIEC’s presence in the region, including the potential accession of the Republic of Kyrgyzstan and the Republic of Tajikistan as new member states. I believe the CIS region has tremendous, untapped potential, and with the right partnerships and robust risk mitigation frameworks in place, it can attract significantly greater volumes of investment and trade.

What motivates me most is seeing projects evolve from initial discussions into real economic activity that creates jobs, strengthens regional connectivity, and supports long-term resilience. I am proud to contribute to ICIEC’s mission of fostering economic growth, regional cooperation, and investor confidence through specialised Shariah-compliant risk mitigation solutions.

MANAGER, ASIA REGION DIVISION, ICIEC

I rejoined ICIEC in October 2025 after a gap of 10 years, during which I worked for international banks, ECAs and investment promotion offices across the Middle East. I have brought over two decades of global experience in trade finance, structured trade, project finance, trade credit and political risk insurance, ECA-backed financing, and Takafulbased solutions.

Coming back to ICIEC after 10 years was a big personal and professional decision. Transitioning from an investment promotion agency, an ECA, and commercial banking to a multilateral environment like ICIEC has indeed allowed me to pivot from policymaking, profit-driven, transactional lending to high-impact developmental finance on a global scale. ICIEC, in particular, has an amazingly strong impact-driven, respectbased culture, which provides a collaborative environment where long-term strategic relationships are valued over high-pressure, short-term targets. By joining ICIEC, I am looking at leveraging and capitalising on my structured trade finance expertise to bridge global funding gaps and champion major regional infrastructure and green energy transitions. Ultimately, this move combines professional purpose with cultural alignment, allowing me to lead complex, cross-border risk management within an institution that prioritises mutual respect, ethical governance, and sustainable economic development.

In my current role, I am leading a team of highly professional individuals with a clear focus on Asia, originating business and supporting businesses in ICIEC member states to grow globally and penetrate new markets, particularly from the perspective of protecting exports, enabling strategic imports and facilitating trade finance and project finance. This exciting role also entails attracting foreign direct investment into ICIEC member states whilst mitigating political risk for international investors, coupled with structuring complex trade and project finance transaction flows in partnership with banks and financial institutions, followed by strong coordination and cooperation with government institutions in delivering cost-effective riskmitigating solutions contributing towards developmental impact.

Asia brings a multitude of opportunities across diverse and very exciting existing and newly emerging sectors and products. Our strategic roadmap includes building a portfolio consisting of a healthy mix of short-term trade credit along with a sizeable exposure to structured medium- and longterm (MLT) solutions to capture the region’s massive industrial growth. During the next couple of years, we will mobilise regional banks’ liquidity by deploying our bespoke solutions like DCIP, BMP and NHSO, which are essentially buyer-credit programmes. In addition, an important part of our strategy is penetrating these frontier markets, which are fairly volatile, through co-insurance syndications with multilaterals like the ADB, AIIB and other multilaterals. In the long term, our growth will be anchored in the region’s multi-decade green transition and structural infrastructure spend. Furthermore, we are looking at establishing reciprocal strategic alliances with leading regional export credit agencies (such as JBIC, NEXI, Malaysia EXIM, Indonesia EXIM, Sinosure and K-SURE) to secure multi-sourcing megaprojects, while utilising ICIEC’s credit enhancement solutions to wrap sub-investment-grade infrastructure opportunities into bankable assets. This dualphased approach effectively insulates our regional aspirations against macroeconomic volatility while positioning us as the premier or preferred risk-mitigating partner for Asia’s evolving trade corridors, particularly for ICIEC member states, thus contributing towards ICIEC’s overall objectives.

With my diversified global experience of over two decades in trade credit and political risk insurance, ECA-backed financing, supply chain finance, and structured trade and project finance, I am indeed looking forward to contributing towards the division’s success and the organisation’s objectives. With a career spanning leadership roles at institutions including Abu Dhabi Investment Office, Etihad Export Credit Insurance Company PJSC, The Saudi British Bank (SABB) and ICIEC – IsDBG, I have spearheaded strategic initiatives across Asia, the Middle East, and Africa, including large-scale infrastructure and energy and renewable energy projects in Iraq, Angola, Uzbekistan, and Senegal. My expertise includes structuring complex trade finance solutions, launching Shariah-compliant products, articulating project finance instruments and building partnerships with global ECAs such as UKEF, Bpifrance, US EXIM and SACE. I was also elected Vice-Chair of the Berne Union MLT Committee during the annual meeting in Kigali in 2022.

I hold a Master’s degree in Commerce (M. Com. major in Finance) from Punjab University, Pakistan, followed by Cost and Management Accountancy (CMA) from the Institute of Cost and Management Accounts (ICMA) of Pakistan. I also hold an Advanced Certificate (full-year programme) in Trade Credit Insurance from Offenburg University, Germany, with distinction in Structured Trade, along with an advanced certificate from INSEAD on Leading Effective Sales Forces.

Central Asia is no longer a region defined only by geography. It is becoming a strategic corridor of growth, connectivity, resources, and reform, linking markets across Asia, Europe, and the wider OIC region.

Comprising Kazakhstan, Uzbekistan, Turkmenistan, Tajikistan, and the Kyrgyz Republic, Central Asia represents one of the most strategically significant and rapidly evolving development regions on the global map. With a combined population of more than 80 million, vast natural resources, and growing demand for infrastructure, finance, energy, trade, and private sector development, the region offers a compelling opportunity for risk-mitigated investment.

For ICIEC, Central Asia’s momentum presents a clear development opportunity. The Corporation’s engagement is anchored in its Member States in the region, namely Kazakhstan, Uzbekistan, and Turkmenistan, where its risk mitigation solutions are already supporting trade, investment, and priority development sectors. Tajikistan and the Kyrgyz Republic also form part of Central Asia’s wider development landscape, with growing potential for future engagement as regional connectivity, investment needs, and economic integration continue to advance.

Across the region, ICIEC’s role is to help convert opportunity into bankable delivery by providing Shariah-compliant insurance and reinsurance solutions that support trade, investment, and capital mobilisation. Through instruments such as Non-Honouring of Sovereign Financial Obligations, Bank Master Policies, Non-Honouring of Financial Obligations by State-Owned Enterprises, NonHonouring of Sovereign Obligations, Political Risk Insurance, and Reinsurance arrangements, ICIEC helps bridge the gap between ambition and execution, enabling complex projects and trade flows to move from concept to implementation.

ICIEC’s Global Context: Where Central Asia Fits

To understand the significance of ICIEC’s Central Asia engagement, it is useful to situate the region within the Corporation’s wider global portfolio.

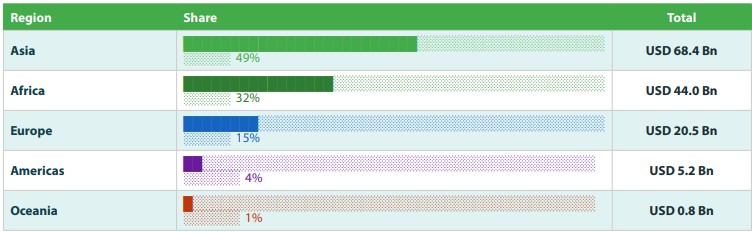

Since inception, ICIEC has insured USD 138.9 billion in business globally, comprising USD 31.1 billion in investment support and USD 107.8 billion in trade facilitation. Asia represents the largest share of ICIEC’s portfolio, with USD 68.4 billion in cumulative business insured, followed by Africa at USD 44.0 billion, Europe at USD 20.5 billion, the Americas at USD 5.2 billion, and Oceania at USD 0.8 billion.

Within this global footprint, Central Asia represents an important and growing part of ICIEC’s Asian portfolio, supported by the region’s strategic location, expanding trade corridors, and rising demand for investment, infrastructure, and private sector development.

ICIEC’s Central Asia Portfolio & Regional Footprint

ICIEC’s Central Asia portfolio is concentrated in Kazakhstan, Uzbekistan, and Turkmenistan, which together account for approximately USD 14.8 billion in cumulative business insured. This reflects the Corporation’s role in supporting development finance across energy, mining, agriculture, transport, financial inclusion, and strategic imports.

- 3ICIEC Member States in Central Asia

- 10+Active transactions across Kazakhstan, Uzbekistan, and Turkmenistan, 2022–2025

- USD 14.8 Bn+Combined cumulative business insured across Kazakhstan, Uzbekistan, and Turkmenistan

- 12Agreements & MoUs related to Central Asia and regional cooperation platforms, 2022–2025

The table below offers a snapshot of ICIEC’s regional presence in Central Asia, showing the scale of cumulative business insured and the main sectors of engagement across Kazakhstan, Uzbekistan, and Turkmenistan.

| Member State | Cumulative Business Insured | Key Sectors of Engagement |

|---|---|---|

| Kazakhstan | USD 12.3 Bn | Energy, trade finance, mining, intra-OIC exports, agricultural commodities |

| Uzbekistan | USD 2.47 Bn | Islamic finance, SME development, energy, gold mining, infrastructure |

| Turkmenistan | USD 63 M | Agricultural machinery, public transport modernisation, sovereign cover |

Across Central Asia, ICIEC’s support has focused on turning development potential into bankable opportunities. The snapshot below highlights selected transactions, institutional partnerships, and key areas of engagement across the region.

Major Transactions & Sectoral Interventions

The period from 2022 to 2025 marked a decisive phase in ICIEC’s Central Asian engagement. Across major transactions in Uzbekistan, Kazakhstan, and Turkmenistan, the Corporation supported more than USD 11.7 billion equivalent in aggregate insurance coverage, helping mobilise financing from commercial banks, export credit agencies, and international financial institutions.

These interventions span Islamic finance and SME development, essential imports, energy infrastructure, mining, agricultural modernisation, public transport, and intra-OIC export facilitation. Each transaction is linked to national development priorities and demonstrates how ICIEC’s Shariah-compliant insurance and reinsurance solutions help convert complex opportunities into bankable delivery.

Through its risk mitigation solutions, ICIEC bridges the gap between opportunity and financing, helping projects move from ambition to implementation.

The full transaction register for the period is set out below, with each entry capturing the instrument deployed, the financing value, the counterparties, and the development rationale. Taken together, they constitute compelling evidence base for ICIEC’s catalytic role across the region.

Year2025

Country Uzbekistan

Uzbekistan

Coverage amountEUR 194.84 mn

NHSFO-SOE Policy, Agrobank Murabaha facility (SCB/SMBC); 7-year tenor, 95% cover. Islamic finance for SMEs & retail via digital platforms ‘OPEN’ and ‘B2B Marketplace’; supports financial inclusion and Uzbekistan’s market transition strategy.

Year2025

CountryUzbekistan

Coverage amountUSD 20 mn

Bank Master Policy (BMP-UK-00005), Mopane Securities PLC; 3-year, 95% cover. Import of capital equipment, medicine, wheat, and edible oil for Aloqabank clients strengthens essential supply chains and economic stability.

Year2025

CountryUzbekistan

Coverage amountUSD 20 mn

Bank Master Policy, Frontera Capital Group; SME liquidity facility to JSC Aloqabank. Provides much-needed liquidity for SME expansion, innovation, and sustainable economic development in Uzbekistan.

Year2024

CountryUzbekistan

Coverage amountEUR 50 mn

Bank Master Policy, Credit Europe Bank line to JSCB Microcredit Bank; 3-year, 90% cover. Uzbekistan SME Assistance Programme: supports job creation, export growth, and economic diversification across multiple sectors.

Year2023

Country Kazakhstan

Kazakhstan

Coverage amountUSD 78.8 mn

Insurance cover for Eurasian Machinery (EMBV, Netherlands), import of Hitachi excavators and dump trucks to Kachary Ruda iron ore mine, Rudny. Supports Kazakhstan’s strategic mining sector under the ‘import of capital goods from non-member states’ scheme; ICIEC–EMBV cooperation since 2014.

Year2023

CountryKazakhstan

Coverage amountUSD 28.8 mn

Reinsurance support to KazakhExport JSC, financial leasing of diesel TE33A locomotives to Azerbaijan Railways. Flagship example of intra-OIC trade facilitation.

Year2022

CountryUzbekistan

Coverage amountUSD 75 mn

NHFO-SOE cover, ICBC Standard Bank facility to Navoi Mining and Metallurgical Company (NMMC); supports NMMC capital expenditure programme, gold mining capacity, export earnings, and fiscal resilience amid global economic volatility.

Year2022

CountryUzbekistan

Coverage amountEUR 60 mn

Political Risk Insurance, USD 40 mn equity + USD 20 mn revenues for Hidro Enerji A.S. 174 MW combined cycle power plant, Khorezm region. Covers expropriation, breach of contract, and transfer restrictions; enhances energy security and industrial capacity.

Year2022

Country Turkmenistan

Turkmenistan

Coverage amountUSD 40 mn

NHSO cover, ING Bank Tokyo Branch facility to State Bank for Foreign Economic Affairs (TFEB); procurement of Komatsu agricultural machinery. Improves irrigation efficiency, food security, and rural productivity; supports water sustainability and climate resilience.

Year2022

CountryTurkmenistan

Coverage amountUSD 20 mn

NHSO cover, ING Bank Tokyo Branch / Sumitomo Corporation; procurement of Toyota buses, taxis, and minibuses. Modernises public transport fleet in Ashgabat and nationwide; enhances social mobility, urban connectivity, and transit corridor development.

Every transaction in this register is aligned with one or more of the United Nations Sustainable Development Goals, from SDG 1 (No Poverty) and SDG 2 (Zero Hunger) to SDG 8 (Decent Work and Economic Growth), SDG 9 (Industry, Innovation and Infrastructure), and SDG 13 (Climate Action), underscoring ICIEC’s commitment to delivering development outcomes alongside financial returns.

Across these transactions, several themes stand out. In Uzbekistan, ICIEC has supported financial inclusion, Islamic finance, SME development, energy security, and mining sector competitiveness. The €194.84 million Agrobank facility represents the largest single Central Asia transaction in the period and a landmark in expanding Shariah-compliant financing for SMEs and retail customers.

In Kazakhstan, the Corporation has supported both industrial productivity and export activity, including mining equipment imports for Kachary Ruda and reinsurance support for KazakhExport’s locomotive export transaction, which completed its full 10-year lifetime cover following the 2023 renewal. In Turkmenistan, sovereign cover instruments have helped unlock critical imports of agricultural machinery and public transport vehicles, contributing to food security, rural productivity, and mobility.

Every transaction in this register is aligned with one or more of the United Nations Sustainable Development Goals, from SDG 1 (No Poverty) and SDG 2 (Zero Hunger) to SDG 8 (Decent Work and Economic Growth), SDG 9 (Industry, Innovation and Infrastructure), and SDG 13 (Climate Action), underscoring ICIEC’s commitment to delivering development outcomes alongside financial returns.

Strategic Alliances & Institutional Partnerships

ICIEC’s transactional reach in Central Asia is reinforced by a growing network of institutional partnerships. Since 2014, the Corporation has concluded agreements and memorandum of understanding with counterparts in Kazakhstan, Uzbekistan, and Central Asia-focused regional platforms, covering export credit agencies, investment promotion authorities, state financial institutions, food security institutions, and bilateral export finance partners.

These partnerships play a practical role in strengthening ICIEC’s regional engagement. They expand underwriting capacity, improve market intelligence, support transaction origination, and build confidence among governments, financiers, and private investors. Together, they help create the institutional foundation needed to transform regional opportunities into bankable projects.

Year2014

CountryKazakhstan

Memorandum of Understanding (MoU)

KazakhExport, Export Credit Agency of Kazakhstan

Scope & Key Objectives

Promote cooperation and expand insurance capacity for KazakhExports, including facultative reinsurance and wider support for export credit insurance cooperation with ICIEC.

Year2020

CountryUzbekistan

Memorandum of Understanding (MoU)

Uzbekinvest, Uzbekistan National Export-Import Insurance Company

Scope & Key Objectives

Expand insurance capacity of both institutions; supports larger trade transactions and development projects.

Year2021

CountryUzbekistan

Memorandum of Understanding (MoU)

Invest Uzbekistan, Investment Promotion Agency under the Ministry of Investment, Industry and Trade of the Republic of Uzbekistan (formerly UzIPA)

Scope & Key Objectives

Cooperate in attracting FDI; promote ICIEC risk-mitigation tools to foreign investors; joint visits, workshops, and capacity building.

Year2021

CountryUzbekistan

Trilateral Memorandum of Understanding (MoU)

Uzbekinvest, National Export-Import Insurance Company & Uzbekinvest International Insurance Company Ltd (UK)

Scope & Key Objectives

Further expand insurance capacity and support Uzbekistan’s export and investment ecosystem.

Partnership Agreement

IOFS, Islamic Organisation for Food Security

Scope & Key Objectives

Signed at the 46th IsDB Annual Meeting, Tashkent. Enhance agri-food trade and investment; IOFS to advise on export credit insurance for wheat and food exports from Central Asia to OIC member states.

Year2023

CountryUzbekistan

Master Facultative Reinsurance Agreement

Uzbekinvest, National Export-Import Insurance Company

Scope & Key Objectives

Provides reinsurance services for exports of goods and services from Uzbekistan worldwide; enhances Uzbekinvest’s underwriting capacity and promotes Uzbek export growth.

Year2023

CountryUzbekistan

Memorandum of Understanding (MoU)

UzSAMA, State Assets Management Agency of the Republic of Uzbekistan

Scope & Key Objectives

Collaborate on privatisation expertise exchange, including the banking sector; attract investors for privatised state assets; advance trade and investment facilitation.

Year2023

CountryUzbekistan

Memorandum of Understanding (MoU)

MKBANK, MicroCreditBank

Scope & Key Objectives

Support trade, exports, and SME financing; develop joint trade and investment initiatives; enhance private sector access to finance.

Year2023

CountryKazakhstan

Quota-Share Treaty Renewal (2024–2026)

KazakhExport, Export Credit Agency of Kazakhstan

Scope & Key Objectives

Renewed reinsurance coverage for KazakhExport’s Documentary Credit Insurance Policy (DCIP); expands underwriting capacity for trade-finance risks; supports SMEs and non-oil export diversification under Baiterek National Investment Holding.

Memorandum of Understanding (MoU)

JBIC, Japan Bank for International Cooperation

Scope & Key Objectives

Signed at the ‘Central Asia and Japan’ forum, Astana. Strengthen cooperation in environmental preservation and green projects across all five Central Asian republics.

Amended Memorandum of Understanding (MoU)

NEXI, Nippon Export and Investment Insurance

Scope & Key Objectives

Amended strategic alliance specifically includes Turkmenistan; extends bilateral cooperation to boost exports and FDI across Central Asia.

Memorandum of Understanding (MoU)

Credendo, Belgian Export Credit Agency

Scope & Key Objectives

Expand risk-sharing capacity for trade transactions in OIC markets, explicitly including Central Asia; enhances reinsurance capacity and broadens market coverage for regional exporters.

Several partnerships merit particular attention. The 2024–2026 Quota-Share Treaty renewal with KazakhExport, built on a decade of cooperation since the original 2014 MoU, directly supports Kazakhstan’s non-oil export diversification agenda under the Baiterek National Investment Holding, channelling reinsurance capacity into the Documentary Credit Insurance Policy that underpins SME trade finance across the country.

The 2024 agreement with the Japan Bank for International Cooperation (JBIC), signed in Astana on the sidelines of the ‘Central Asia + Japan’ forum, establishes a green project cooperation framework spanning all five republics, a forward-looking platform for climatealigned financing across the sub-region.

The 2025 amendments to the NEXI agreement (now explicitly including Turkmenistan) and the new Credendo partnership reflect a conscious strategy to internationalise ICIEC’s risk-sharing infrastructure, drawing European and Japanese export credit institutions into a collaborative framework that amplifies the financing available to Central Asian Member States.

In Uzbekistan, the depth of partnership is particularly notable: MoUs with Uzbekinvest, Invest Uzbekistan, (formerly UzIPA, Uzbekistan Investment Promotion Agency), UzSAMA, and MicroCreditBank, complemented by the 2023 Master Facultative Reinsurance Agreement, have created a multi-layered ecosystem in which ICIEC’s tools are embedded across investment promotion, privatisation, SME finance, and export credit. This ecosystem approach is increasingly the template for ICIEC’s engagement across the wider region.

Looking Ahead: A Region Defined by Shared Opportunity

Central Asia’s development story is gaining momentum. While its five republics differ in economic structure, reform pace, and investment readiness, they share a common ambition to build more diversified, resilient, and sustainable economies that are better connected to regional and global markets.

This ambition is already visible across the region. Kazakhstan’s mining, energy, and export activity continues to support its role as a major regional economy. Turkmenistan’s priorities in agriculture, machinery, and transport modernisation point to the importance of strengthening productive capacity and essential services. Uzbekistan’s growing focus on SME finance platforms, energy, infrastructure, and industrial development reflects a broader reform agenda aimed at mobilising investment and expanding private sector participation. Looking ahead, Tajikistan and the Kyrgyz Republic also present important potential as connectivity, trade facilitation, and investment readiness continue to evolve.

Across these markets, ICIEC’s role is to help turn regional ambition into bankable delivery. Through Shariah-compliant risk mitigation and strategic partnerships, the Corporation supports transactions that strengthen trade, mobilise capital, and give lenders and investors the confidence to participate in priority sectors. As Central Asia becomes increasingly important to global trade and development corridors, ICIEC remains committed to supporting projects that advance resilience, connectivity, and sustainable growth across the region.

Uzbekistan’s growing focus on SME finance platforms, energy, infrastructure, and industrial development reflects a broader reform agenda aimed at mobilising investment and expanding private sector participation. Looking ahead, Tajikistan and the Kyrgyz Republic also present important potential as connectivity, trade facilitation, and investment readiness continue to evolve.

THE CAPITAL

Baku: A City of Winds

Few cities in the world so seamlessly stitch together centuries of history with bold architectural modernity. Baku achieves this effortlessly. Standing along its Caspian Boulevard, a visitor’s gaze moves from the medieval ramparts of the Old City to the shimmering curves of the Heydar Aliyev Centre, as if two eras were holding a quiet conversation across time.

A UNESCO World Heritage Site, Baku’s ancient walled inner city harbours the Maiden Tower and Palace of the Shirvanshahs, stones that reflect centuries of civilisation.

Three soaring glass skyscrapers clad in LED panels evoke the natural flames associated with Azerbaijan’s historic identity as the ‘Land of Fire.’ By night, they illuminate the skyline in rippling ribbons of colour.

Designed by the late Zaha Hadid, this undulating white masterpiece, defined by sweeping curves and fluid forms, has become a global icon of contemporary architecture.

To walk from the cobblestones of Icherisheher to the reflective glass of the Flame Towers is to traverse a thousand years in a single journey and to understand that Azerbaijan has always been a place where worlds meet.

CULTURAL HERITAGE

Woven in Time: Art, Craft & Identity

Azerbaijan’s cultural identity is rich, layered, and deeply felt. Long a crossroads on the ancient Silk Road, the country absorbed and gave back to Persian, Turkic, Arab, Russian, and Ottoman civilisations, producing a culture that is uniquely, unmistakably Azerbaijani.

INTANGIBLE HERITAGE

Recognised by UNESCO, Azerbaijani carpet weaving is one of the country’s most refined and historically significant textile traditions. Each carpet is a language; its geometric motifs encode tribal stories and centuries of history. The Azerbaijani Carpet Museum in Baku, shaped like a rolled carpet, is itself a tribute to this living art form.

ARCHITECTURE & CRAFTS

The carved stone facades of Old Baku’s caravanserais, the distinctive ornamental brickwork of Sheki’s Khan Palace, and the centuries-old craft of copperwork in the village of Lahij speak to a civilisation that placed beauty at the centre of everyday life.

PERFORMING ARTS

The carved stone facades of Old Baku’s caravanserais, the distinctive ornamental brickwork of Sheki’s Khan Palace, and the centuries-old craft of copperwork in the village of Lahij speak to a civilisation that placed beauty at the centre of everyday life.

LITERATURE

A Legacy of Poets & Scholars

From the 12th-century poet Nizami Ganjavi, whose works have influenced literary and artistic traditions across the East and beyond, to satirist Mirza Fatali Akhundov, Azerbaijan has long nurtured a deep tradition of letters, philosophy, and intellectual life.

NATURAL WONDERS

Land of Fire, Sea & Mountain

Beyond the capital, Azerbaijan reveals a geography of startling contrasts: subtropical lowlands, alpine peaks, semi-desert steppes, and a vast inland sea all within one compact territory. Nature here is never simply a backdrop; it is part of the national story.

The world’s largest landlocked body of water defines Baku’s horizon. Its shoreline promenade, the Baku Boulevard, stretches for kilometres, alive with cafés, gardens, and the gentle lapping of silver waves.

A UNESCO site housing over 6,000 rock carvings dating back 40,000 years. Nearby, bubbling mud volcanoes, of which Azerbaijan hosts one-third of the world’s total, create an otherworldly, primordial landscape.

A UNESCO site housing over 6,000 rock carvings dating back 40,000 years. Nearby, bubbling mud volcanoes, of which Azerbaijan hosts one-third of the world’s total, create an otherworldly, primordial landscape.

FOOD & HOSPITALITY

The Table as a Welcome

In Azerbaijan, hospitality is not a custom; it is a philosophy. A guest, the old saying goes, is sent by God. To be welcomed into an Azerbaijani home or restaurant is to be enveloped in warmth, generosity, and an abundance of flavour. The Azerbaijani table is a testament to its geography and history. Plov, a saffronscented rice dish adorned with dried fruits and chestnuts, is the undisputed centrepiece of the national kitchen, with over 40 regional varieties. Dolma (grape leaves stuffed with spiced lamb and herbs), dushbara (tiny hand-crafted dumplings in a rich broth), and the tangy pomegranate-based sauce narsharab all speak of a culinary tradition shaped by Persian elegance and Caucasian heartiness. A glass of strong black tea, poured into an armudu (pear-shaped) glass with sour cherry preserves on the side, is the quiet, ever-present ritual of daily life.

This harmonious blend of tradition and modernity is evident throughout Azerbaijan. While the country embraces the latest technologies and international trends, the core values of heritage and hospitality remain deeply rooted. Visitors will find a country that is proud of its past and excited about its future, offering a unique experience that lingers long after the journey ends.

In Azerbaijan, hospitality is not a custom; it is a philosophy. A guest, the old saying goes, is sent by God. To be welcomed into an Azerbaijani home or restaurant is to be enveloped in warmth, generosity, and an abundance of flavour.

Source note: Prepared with reference to publicly available sources, including UNESCO World Heritage and Intangible Cultural Heritage materials, official cultural resources, and reputable publications on Azerbaijan’s history, architecture, and cultural heritage.

According to the Energy Institute Statistical Review of World Energy (2025), OPEC, and the IEA, Azerbaijan ranks 20th globally in terms of proven crude oil reserves, holding approximately 7 billion barrels. This represents roughly 0.4% of the world’s total reserves. In terms of average daily production, Azerbaijan is among the top 25 global producers, accounting for about 0.6% of the global oil supply. Furthermore, the country ranks 23rd worldwide in proven natural gas reserves, with approximately 2.5 trillion cubic meters. Azerbaijan is recognised as a key exporter due to its advanced infrastructure, notably the Southern Gas Corridor, and currently leads the region in the growth rate of gas exports to Europe.

In 2025, Azerbaijan’s GDP amounted to approximately $75 billion. The primary sectors contributing to the GDP include the industrial sector (including oil and gas) at 41%, Trade at 10%, Transport at 7%, Construction at 6%, Agriculture at 4%, and the Banking sector at 3%. Azerbaijan’s export profile remains dominated by the hydrocarbon sector, which accounted for approximately 87% of total export revenues in 2025. However, during 2024–2025, the non-oil and gas sector achieved a sustained majority share of the national economy, reaching 52.7% of GDP.

While Azerbaijan has traditionally utilised its hydrocarbon wealth as the primary engine of economic expansion, contemporary policy frameworks are increasingly focused on fostering diversification away from the oil and gas sectors. Leveraging its strategic location and abundant natural resources, the country is now pivoting towards a diversified, knowledge-based economy, bolstered by robust international partnerships and a favourable investment climate.

Azerbaijan continues to maintain a strong credit profile as of April 2026, holding investment-grade ratings from Fitch (BBB-, Stable) and Moody’s (Baa3, Positive), while S&P Global maintains a BB+ rating with a Positive outlook.

AZERBAIJAN 2030: NATIONAL PRIORITIES

In February 2021, the President of the Republic of Azerbaijan issued a decree approving the “National Priorities for Socio-Economic Development: Azerbaijan 2030”. This foundational document defines five key vectors for the country’s strategic development:

- A Sustainably Growing, Competitive Economy: A strategic focus on the non-oil sector, innovation, and export diversification.

- A Dynamic, Inclusive Society Based on Social Justice: Emphasis on poverty reduction and comprehensive regional development. 3) Competitive Human Capital and a Modern Innovation Space: Implementation of educational reforms and support for the startup ecosystem.

- The “Great Return” to Liberated Territories: Full economic and social reintegration of the Karabakh and East Zangezur regions.

- A Clean Environment and a “Green Growth” Country: Transitioning to renewable energy sources and the reduction of carbon emissions.

As the initial implementation phase of “Azerbaijan 2030”, the 2022–2026 Socio-Economic Development Strategy serves as a strategic roadmap to increase the private sector’s economic share to 88%. Key pillars include SOE optimisation, judicial reforms, and the expansion of industrial parks and FEZs. Complementing this, the “Great Return” programme (est. 2022) focuses on the economic reintegration of liberated territories, which are projected to generate 25% of the national GDP by 2030.

STRATEGIC CONNECTIVITY AND REGIONAL PARTNERSHIPS

Beyond its domestic agenda, Azerbaijan serves as a critical geostrategic bridge between Asia and Europe through several large-scale international projects:

- The Middle Corridor (TITR): A flagship multimodal transport route bypassing Russia to connect China and Central Asia with Member Country Profile: Azerbaijan Bounded by the Caspian Sea and the Caucasus Mountains, Azerbaijan, often referred to as the ‘Pearl of the Caspian’, stands as a natural bridge between East and West. Azerbaijan is bordered by Russia, Georgia, Armenia, Türkiye, and Iran. The nation’s geography features a diverse mix of rugged mountain ranges and fertile lowlands, supported by a vast natural resource base centred on its significant oil and gas reserves. COUNTRY AND REGION FOCUS 22 ICIEC SPECIAL ISSUE COUNTRY AND REGION FOCUS Europe. By digitising customs and expanding the Port of Alyat, transit times have been reduced to 12-15 days.

- Railway Infrastructure Modernisation: To support these corridors, Azerbaijan is upgrading its rail network:

- East-West Axis: The Baku-Tbilisi-Kars (BTK) railway has been expanded to a capacity of 5 million tons annually, serving as the backbone of the Middle Corridor.

- North-South Axis: The reconstruction of the Baku-Yalama and Baku-Astara lines facilitates seamless transit between Russia, Iran, and the Persian Gulf.

- Reconstruction of Liberated Territories: The construction of the Horadiz-Agbend line is a priority, designed as a key segment of the future Zangezur Corridor to link mainland Azerbaijan with Nakhchivan and Türkiye.

The Digital Silk Way: A strategic initiative to transform Azerbaijan into a regional digital hub. This involves laying a subsea fiber-optic cable across the Caspian Sea (connecting Azerbaijan and Kazakhstan) to provide a high-speed data corridor between East Asia and the EU.

- Green Energy Corridor: A multi-stage project to export renewable energy to Europe. This includes a high-voltage Caspian subsea cable (integrating the power grids of Uzbekistan, Kazakhstan, and Azerbaijan) linked to the Black Sea submarine cable reaching Romania and Hungary.

- Southern Gas Corridor (SGC) Expansion: A vital pillar of EU energy security. Ongoing efforts aim to double gas export capacity to 20 billion cubic meters annually by 2027 through the modernisation of the TANAP and TAP pipelines.

- North-South Transport Corridor (INSTC): Azerbaijan is the only country participating in both the East-West and NorthSouth axes, facilitating trade between India, the Persian Gulf, and Northern Europe.

FISCAL AND MONETARY POLICY: AZERBAIJAN AND CENTRAL ASIAN COUNTRIES

Compared to Central Asian economies, Azerbaijan’s growth dynamics appear more moderate. In Kazakhstan, after a period of accelerated growth, expansion is projected to gradually converge to around 3.5-4% by 2030-2031, while Uzbekistan is expected to maintain higher growth rates of approximately 5.5-6% throughout the forecast horizon. At the same time, Turkmenistan shows growth rates comparable to Azerbaijan, in the range of 2-3% in 2026-2031, indicating broadly similar macroeconomic parameters within the IMF projections. Thus, through 2031, Azerbaijan is characterised by a stable economic growth trajectory.

Based on the analysis of the latest data from national statistical agencies and the United Nations Population Division, Azerbaijan presents a distinct demographic profile characterised by maturity and high density. With a population of approximately 10.5 million, Azerbaijan is significantly more compact than Kazakhstan (~21.1 million) or Uzbekistan (~37.7 million), resulting in the highest population density in the group at 122 people per km². While Uzbekistan and Turkmenistan maintain a “younger” demographic with median ages under 27, Azerbaijan – much like Kazakhstan – has transitioned into a more mature stage with a median age of 32.4 years. Furthermore, while Uzbekistan leads in absolute annual growth at 2.0%, Azerbaijan demonstrates a more stable and moderate growth rate of approximately 0.5%, reflecting an advanced stage of demographic transition and a higher level of urbanisation compared to its Central Asian neighbours.

Azerbaijan demonstrates a high degree of fiscal liquidity and a stable inflationary environment relative to its regional peers. In 2025, Azerbaijan effectively stabilised its inflation rate at ~6%. In contrast, regional peers faced significantly higher pressures: Kazakhstan recorded a year-end inflation rate of 12.3%, driven largely by rising costs in utilities and food services, while Uzbekistan reported inflation at ~7-8%.

For the period spanning the 2025 fiscal year through the first quarter of 2026, the regional economic landscape reveals that Azerbaijan maintains the highest ratio of reserves relative to its economic output among its peers. Azerbaijan’s total sovereign assets – consisting of Central Bank reserves and the State Oil Fund of Azerbaijan (SOFAZ) – reached a record $85.15 billion, an amount that represents approximately 112% of its annual GDP. In comparison, Kazakhstan holds the highest absolute financial buffers in the region at $100.6 billion, comprising both National Bank reserves and the assets of the National Fund of the Republic of Kazakhstan; however, due to the larger size of its economy, this total is equivalent to roughly 38-40% of its GDP. Meanwhile, Uzbekistan’s total sovereign assets, which include the Fund for Reconstruction and Development and gold-forex reserves, are estimated to be between $52 and $55 billion, accounting for approximately 50-55% of its GDP.

It is estimated that by the end of 2025, Azerbaijan demonstrated a high degree of fiscal stability by maintaining a budget surplus of 2.4% of GDP, driven by disciplined expenditure and robust hydrocarbon exports. In contrast, Kazakhstan and Uzbekistan recorded fiscal deficits of approximately 3.1% and 4.0% of GDP, respectively, during the same period.

ICIEC’S ENGAGEMENT WITH AZERBAIJAN

ICIEC’s involvement in Azerbaijan began prior to its membership in 2023. ICIEC reinsured KazakhExport for the export of diesel locomotives from Kazakhstan to Azerbaijan Railways and insured several member country banks and exporters for transactions involving Azerbaijan. In 2024, ICIEC supported a transaction in the telecommunication sector of Azerbaijan. In summary, since Azerbaijan joined ICIEC, approximately USD 164 million in cumulative business has been insured.

Potential areas of cooperation:

- Middle Corridor and Regional Partnerships: Azerbaijan actively cooperates with the countries of Central Asia and Türkiye. Located on the route connecting Europe and China, Azerbaijan is one of the beneficiaries of this trade path. Locomotive supply deals in the railway industry may be expanded to support Azerbaijan’s logistics sector. Support can also be provided in maritime logistics in the Caspian Sea.

- PPP frameworks: The development of PPP is one of the key instruments for implementing the Azerbaijan 2030 strategy. Azerbaijan’s main focuses in the application of PPP are 1) green energy, 2) infrastructure and logistics, 3) the social sphere, and 4) water desalination. In April 2024, an agreement was signed for the implementation of a project for the desalination of Caspian Sea water based on the PPP model (investor: ACWA Power).

- Digitalisation: The experience of implementing ICIEC projects with world-leading communication equipment suppliers in Central Asian countries can be actively utilised in Azerbaijan.

Dr. Khalid Khalafalla, CEO of ICIEC, highlighting the transformative role of Islamic finance and export credit insurance in advancing sustainable investment across the Trans-Caspian International Transport Route (TITR). The article examines how Shariah-compliant financial structures and ICIEC’s risk mitigation solutions can catalyse private sector participation, support strategic infrastructure and energy projects, deepen regional connectivity, and foster greater investor confidence throughout Central Asia and the South Caucasus.

Islamic finance and export credit insurance together form a mutually reinforcing development architecture that is highly relevant to unlocking investment across the Trans-Caspian International Transport Route. In this corridor, Islamic finance, anchored in asset-backing and risk-sharing principles, naturally directs capital toward real-economy sectors such as infrastructure, logistics, energy, and trade facilitation. Instruments like sukuk and Murabaha-based trade finance are particularly well suited to the region, as they provide long-term, stable financing aligned with productive investment needs while avoiding excessive leverage in markets where debt sustainability is already constrained.

Within this ecosystem, export credit insurance functions play a critical catalytic role by de-risking cross-border investment flows and converting potential into bankable reality. By covering political, credit, and commercial risks, such as non-payment, currency inconvertibility, or contract frustration, ICIEC enables cross-border investments into higherrisk but high-impact markets, including Kazakhstan, Uzbekistan, Azerbaijan, and Georgia. This de-risking function is especially critical in enabling infrastructure corridors, energy interconnections, and SME trade flows that would otherwise struggle to achieve financial close.

Strategically, the integration of Islamic finance and ICIEC-backed insurance supports three core development outcomes in the corridor. First, it crowds in private capital by improving risk-return profiles for investors, particularly in transport infrastructure, renewable energy, SME-focused investments and industrial development zones. Second, it strengthens intra-OIC and South–South trade connectivity, reducing dependence on traditional financial and logistics corridors while enhancing regional value chain integration across Eurasia. Third, it enables financial inclusion and SME and mid-sized exporters’ participation, especially when insured Islamic trade finance is extended through banks and fintech-enabled platforms in underserved markets.

The most scalable opportunity lies in building blended finance ecosystems, where Islamic financial instruments provide Shariah-compliant capital, ICIEC provides credit and political risk mitigation, and development finance institutions act as anchor investors. This structure is particularly effective for public–private partnerships, crossborder logistics infrastructure, and green energy projects, which are central to the corridor’s transformation agenda. However, scaling remains dependent on enabling conditions such as regulatory harmonisation, stronger project preparation pipelines, and deeper capital market development across participating countries.

Ultimately, the integration of Islamic finance and export credit insurance provides a coherent financial and risk mitigation framework for the Central Asia–South Caucasus corridor. It combines capital mobilisation with risk absorption, enabling structurally important but higher-risk investments to proceed. In doing so, it positions ICIEC as a catalytic intermediary, bridging liquidity and risk to unlock sustainable, inclusive, and resilient investment flows across one of the most strategically significant emerging corridors.

Looking forward, ICIEC is well-positioned to prioritise high-impact countries, sectors, and instruments that align with corridor development. Priority geographies are likely to include Kazakhstan and Uzbekistan (scale and reform momentum), alongside Azerbaijan and Georgia (transit and logistics hubs). Key sectors include transport infrastructure (rail corridors, ports, and logistics hubs), renewable energy (solar, wind, and green hydrogen), conventional energy exports, and digital connectivity. Product selection will centre on political risk insurance, foreign investment insurance, and export credit guarantees, particularly for PPPs and cross-border projects requiring credit enhancement. Flagship opportunities may include upgrades along the Middle Corridor, Caspian-linked energy projects, and integrated trade facilitation platforms that reduce bottlenecks and improve regional competitiveness.

From a geopolitical perspective, the corridor sits at the intersection of competing and converging regional interests, shaping both current and future risk dynamics. Ongoing shifts in global trade patterns, sanctions regimes, and regional alignments are increasing the corridor’s relevance while also introducing volatility. The diversification away from traditional northern routes has elevated the importance of the Caspian pathway, but risks remain linked to regional disputes, border sensitivities, and external power competition. Over the medium term, however, continued economic cooperation, infrastructure investment, and policy alignment among corridor countries could gradually reduce friction and enhance stability. For ICIEC, this means maintaining a forwardlooking risk posture, leveraging its risk mitigation toolkit to navigate uncertainty while anchoring investor confidence in a corridor that is becoming central to Eurasian trade and investment flows.

The geopolitical environment adds both opportunity and complexity. The corridor is increasingly relevant due to sanctions-driven trade rerouting, regional realignment, and diversification strategies by global and regional powers. While this enhances its strategic value, it also introduces volatility linked to geopolitical tensions, regional disputes, and policy fragmentation. Over time, gradual integration efforts and infrastructure investments may improve stability, but near-term risk remains elevated and asymmetric across countries.

Within this context, ICIEC’s risk appetite and cover attitude are best described as ‘selective catalytic’. The Corporation maintains a moderate-to-high risk appetite in strategic member states, particularly where its participation can unlock otherwise unbankable investments, but this is done within clearly defined capital protection boundaries. ICIEC continues to cover political and credit risks in higher-risk jurisdictions, while insisting on strong risk structuring, such as sovereign or quasisovereign backing, robust contractual frameworks, and diversified risk-sharing arrangements. This approach avoids binary risk acceptance and scales exposure dynamically based on country limits, project quality, and mitigation strength.

ICIEC’s underwriting approach already reflects rigorous country risk assessment frameworks, which are critical in this corridor given varying sovereign risk profiles and political dynamics. These include evaluating macroeconomic stability, debt sustainability, regulatory quality, and exposure to external shocks such as commodity price volatility. For instance, energy-dependent economies like Azerbaijan and Kazakhstan require careful assessment of fiscal buffers and diversification efforts, while reformorientated markets like Uzbekistan present improving but still evolving risk environments. In the South Caucasus, geopolitical considerations and regional tensions necessitate enhanced political risk analysis, particularly for longterm infrastructure and foreign direct investment projects. These risk diagnostics inform ICIEC’s exposure limits, pricing, and structuring of guarantees and insurance products.

Ultimately, ICIEC’s strategy in the corridor reflects a dual objective: enabling development while preserving capital adequacy and financial sustainability. This will be achieved by deploying risk mitigation instruments to crowd in private capital, prioritising sectors with strong developmental and cash-flow fundamentals and continuously adjusting exposure in response to geopolitical and macro-financial signals. This disciplined yet enabling posture allows ICIEC to act as a stabilising risk intermediary, unlocking corridor opportunities while safeguarding long-term financial viability.

However, to fully realise this potential, several enablers are needed: stronger regulatory harmonisation across jurisdictions, deeper local capital markets, improved project preparation pipelines, and greater awareness among global investors of Islamic finance structures. Without these, scale will remain constrained.

In essence, Islamic finance provides the values-based capital architecture, while export credit insurance provides the confidence mechanism, and together, they can accelerate sustainable, inclusive, and resilient development across emerging and frontier economies.

THE CHAIRMAN OF THE MANAGEMENT BOARD AT AGROBANK

As Uzbekistan continues to expand its engagement with international capital markets and Islamic finance, strategic partnerships are playing an increasingly important role in mobilising investment and supporting sustainable economic growth. In this interview, Mr. Erkin Azizzhonovich Kakhorov, Chairman of the Management Board of Agrobank, reflects on the Bank’s successful cooperation with ICIEC and how this partnership enabled a landmark Islamic financing transaction. He discusses the value of risk mitigation in attracting international investors, the growing importance of Shariah-compliant financing solutions, and the opportunities that closer collaboration between financial institutions and multilateral partners can create for trade, investment, and development across Uzbekistan and the wider region.

Could you share the Bank’s perspective on its cooperation with ICIEC and explain how this partnership contributes to the achievement of Agrobank’s strategic objectives?

Before addressing this question directly, allow me to briefly elaborate on how Agrobank arrived at its cooperation with ICIEC. As you may know, since 2010 Agrobank has maintained close and productive cooperation with institutions of the Islamic Development Bank Group. In particular, collaboration with ICD and ITFC enabled Agrobank to make a meaningful contribution to the promotion of Islamic financing mechanisms for entrepreneurs and businesses across the Republic.

With the growing demand for Shariahcompliant financial products among the Bank’s clients, Agrobank identified the strategic necessity of accessing capital markets that operate in accordance with Islamic finance principles. The solution was found through cooperation with ICIEC, which is also a member of the Islamic Development Bank Group. Furthermore, the experience gained through our engagement with other institutions of the Group enabled us to establish a mutually beneficial partnership with ICIEC within a relatively short period of time.

As a result, Agrobank became the first bank in the country to access the international Islamic capital market through a Commodity Murabaha transaction, thereby establishing a strong presence both within the Republic and among international Islamic investors.

With the growing demand for Shariahcompliant financial products among the Bank’s clients, Agrobank identified the strategic necessity of accessing capital markets that operate in accordance with Islamic finance principles.

What were the key advantages of cooperation with ICIEC in facilitating the respective transaction and arranging the financing?

I t would not be an exaggeration to state that Agrobank’s cooperation with ICIEC and the resulting Commodity Murabaha transaction supported by the Corporation’s coverage, represents one of the most significant financial events of the year. This milestone enabled Agrobank not only to access the international Islamic liquidity market, but also to overcome the limitations associated with country exposure limits.

This partnership has substantially strengthened the Bank’s standing in international financial markets, enhanced confidence among foreign investors and Islamic financial institutions, and expanded Agrobank’s capacity to finance entrepreneurs while broadening the availability of banking services through Islamic financial products.

One of the key advantages of cooperation with ICIEC has been the implementation of effective commercial and political risk mitigation instruments. This enabled Agrobank to attract more accessible and longer-term financial resources, which are critically important both for the Bank and for the broader national economy. In addition, the insurance coverage and guarantees provided by ICIEC contributed to more efficient transaction structuring and strengthened cooperation with international counterparties.

Through this mechanism, the Bank has been able to provide greater support to agriculture, the processing industry, and infrastructure development projects, as well as small and medium-sized enterprises. This is particularly important amid the growing demand for financial resources from entrepreneurs and exportoriented companies.

Based on Agrobank’s experience, partnerships between banks and international institutions such as ICIEC play a significant role in promoting sustainable trade and investment in Uzbekistan. Such cooperation contributes to strengthening the investment climate, enhancing confidence in the national banking system, and facilitating the country’s deeper integration into international financial markets.

Based on your experience, what role can partnerships between banks and institutions such as ICIEC play in promoting sustainable trade and investment in Uzbekistan?

In this regard, I would emphasise that such mechanisms create additional opportunities for financing sustainable development projects and introducing modern financial instruments. Cooperation with ICIEC has also provided Agrobank with valuable practical experience that may serve as a useful benchmark for other financial institutions across the region.

By mitigating investor risks, ICIEC and similar institutions serve as an important catalyst for attracting investment into Uzbekistan in general and for advancing Islamic banking and financing instruments in particular.

What lessons and insights have been gained from Agrobank’s cooperation with ICIEC that could be valuable for other financial institutions?

First and foremost, as previously mentioned, this was the first transaction of its kind in Uzbekistan. Agrobank has effectively established a benchmark that may serve as a reference point for other financial institutions across the region. Building upon the experience gained, Agrobank intends to continue developing new capital attraction mechanisms and further strengthen its engagement with international investors.

Secondly, through the successful execution of this transaction, the Bank demonstrated to international investors its high standards of corporate governance, operational transparency, and effective risk management framework. Experience confirms that long-term partnerships built on mutual trust and a strategic approach are essential for the successful implementation of major international projects.

Looking ahead, which areas of future cooperation with ICIEC do you consider the most promising in supporting Agrobank’s development priorities?

Speaking about future prospects, Agrobank sees significant potential in expanding joint initiatives in the areas of green finance, support for the agroindustrial sector, and Islamic finance, as well as the further development of programmes aimed at supporting small and medium-sized enterprises.

The Bank is confident that continued cooperation with ICIEC will not only strengthen Agrobank’s financial resilience but will also make a substantial contribution to the implementation of Uzbekistan’s priority socio-economic development objectives.

Partnership with ICIEC constitutes an important component of the Bank’s long-term strategy aimed at expanding international cooperation and attracting sustainable long-term financing.

EXECUTIVE DIRECTOR, DEVELOPMENT & AGENCY FINANCE, STANDARD CHARTERED BANK

In Central Asia, the gap between ambition and investment often comes down to one thing: risk. In this conversation, Ms. Desislava Radeva of Standard Chartered Bank explains how partnership with ICIEC is closing that gap, turning complex, capital-intensive projects into bankable opportunities, drawing international capital into Uzbekistan’s industrial base, and widening access to finance for the SMEs that drive inclusive growth. Her message is clear: where risk is well managed and partners align, the region’s potential becomes investable.

Standard Chartered Bank has partnered with ICIEC on important transactions in Central Asia, including the Agrobank and Uzbek Steel deals. How do you assess the value of this cooperation in supporting strategic financing in the region?

Our cooperation with ICIEC has proved highly valuable in enabling strategic, development focused financing in Central Asia, particularly in Uzbekistan, where access to long term capital and effective risk mitigation are of high importance.

In the Agrobank transaction, ICIEC’s support was instrumental in mobilising EUR 160.4 million of Islamic financing to expand access to Shariah-compliant funding for retail customers and SMEs across Uzbekistan. By combining Standard Chartered’s structuring and arranging expertise with ICIEC’s insurance support, the transaction helped unlock financing for sectors that are central to economic growth, financial inclusion and job creation, while also introducing a first-of-its-kind Murabaha structure for the market.

Similarly, in the Uzbek Steel (Uzmetkombinat) financing, our partnership with ICIEC enabled a EUR 132.5 million facility to support the completion of Uzbekistan’s new Casting and Rolling Complex in Bekabad. With ICIEC providing risk mitigation, the financing supports a strategic industrial project that reduces reliance on imports, strengthens domestic supply chains and underpins long term industrial resilience and employment in the region.

Together, these transactions demonstrate the tangible value of our collaboration with ICIEC: combining complementary strengths to de-risk complex financings, attract international capital and support projects that deliver lasting economic and social impact. This partnership plays an important role in supporting Central Asia’s development priorities and provides a strong foundation for continued collaboration in the region.

From your perspective, how did ICIEC’s risk mitigation solutions contribute to the successful structuring and execution of the Agrobank and Uzbek Steel transactions?

I CIEC’s risk mitigation solutions were central to both the structuring and successful execution of the Agrobank and

In the Uzbek Steel (Uzmetkombinat) financing, our partnership with ICIEC enabled a EUR 132.5 million facility to support the completion of Uzbekistan’s new Casting and Rolling Complex in Bekabad. With ICIEC providing risk mitigation, the financing supports a strategic industrial project that reduces reliance on imports, strengthens domestic supply chains and underpins long term industrial resilience and employment in the region.

Uzbek Steel transactions, particularly in a market where long Tenor financing and investor confidence are essential.

In the Agrobank financing, ICIEC’s support provided the credit enhancement needed to mobilise Islamic financing into Uzbekistan. By mitigating political and credit risk, ICIEC enabled Standard Chartered to structure a Murabaha facility for the market with confidence. This risk cover was critical in allowing funding to be channelled at scale into retail and SME segments, supporting financial inclusion and economic growth while ensuring the transaction remained commercially viable and robust for all participants.

For the Uzbek Steel (Uzmetkombinat) transaction, ICIEC’s provision of insurance support again played a pivotal role. The facility benefited from ICIEC’s sovereign-backed risk mitigation, which helped unlock long term financing for a strategic industrial project vital to Uzbekistan’s economic development. By reducing investment risk, ICIEC enabled the financing of a complex, capitalintensive project that strengthens domestic steel production, improves supply chain resilience and delivers meaningful social and economic impact at a national level.

Across both deals, ICIEC’s risk mitigation solutions acted as a catalyst, de-risking transactions, broadening investor participation and enabling innovative financing structures that might otherwise have been challenging to deliver. This partnership allows Standard Chartered to support clients and sovereign priorities with confidence, while ensuring that critical projects in Central Asia can access sustainable, long term capital aligned with development goals.

What do these transactions reveal about the financing needs and investment potential of priority sectors in Central Asia, particularly in relation to industrial development and private sector growth?

These transactions underline that priority sectors in Central Asia combine strong growth potential with a clear need for structured, long term financing that supports economic development in a sustainable and resilient way.

The Uzbek Steel financing highlights the scale of investment required to modernise and expand industrial capacity in the region. Heavy industry remains central to economic growth, job creation and supply chain resilience, yet projects of this nature are capital-intensive and require long tenors, robust structuring and effective risk mitigation to be bankable. The transaction demonstrates that there is significant appetite to invest in strategic industrial assets when financing solutions are aligned with national development priorities and designed to support more efficient, locally anchored production.

At the same time, the Agrobank transaction illustrates the depth of opportunity within the private sector, particularly among SMEs and retail customers. Expanding access to financing for these segments is critical to unlocking inclusive growth and entrepreneurship across Central Asia. The demand for scalable, Shariah-compliant solutions also reflects the evolving sophistication of financial markets and a growing willingness to adopt innovative financing structures to meet local needs.

These deals show that Central Asia’s priority sectors require capital that goes beyond short term funding, combining commercial discipline with development impact. Industrial development, private sector growth and sustainability objectives are increasingly interconnected: modern industry requires investment in efficiency and resilience, while SMEs need reliable access to finance to participate in and benefit from broader economic transformation.

Crucially, the transactions also demonstrate that investment potential is strong when risks are appropriately managed and public-private collaboration is effectively mobilised. With the right frameworks, risk mitigation tools and international expertise, Central Asia can continue to attract private capital into sectors that support diversification, productivity and long term prosperity.

How can partnerships between international banks and multilateral risk mitigation institutions such as ICIEC help unlock more bankable opportunities and attract greater cross-border financing into the region?

Partnerships between international banks and multilateral risk mitigation institutions such as ICIEC play a critical role in transforming opportunity into investable, bankable transactions across Central Asia.

These partnerships help address fundamental risk constraints that often limit cross-border financing into emerging markets. Institutions like ICIEC provide the credit enhancement needed to reduce perceived and actual risks. This allows international banks to structure longer-tenor financings, mobilise larger pools of capital and bring a broader range of lenders and investors into transactions that might otherwise struggle to reach financial close.

Close collaboration also supports the development of bankable structures for complex projects. Multilateral partners bring local and regional insight, while international banks contribute structuring expertise, distribution capability and sector knowledge. Together, this enables financing solutions that are aligned with national development priorities, robust from a risk and credit perspective, and attractive to international capital markets.

In regions like Central Asia, where growth ambitions are strong and financing needs are evolving, partnerships of this nature provide a scalable model for attracting international investment while supporting orderly and sustainable development.

Looking ahead, what role do you see for Standard Chartered Bank in further supporting sustainable trade, investment, and economic development across Central Asia through similar partnerships and structures?

We see Standard Chartered playing an active role in mobilising sustainable trade and investment across Central Asia, building on the same partnership-led approach demonstrated in transactions such as Agrobank and Uzbek Steel.

These partnerships allow us to blend international banking expertise with risk mitigation and development alignment, creating bankable structures for projects that support economic diversification, local value creation and long term competitiveness. As demonstrated in recent transactions, this approach can unlock repeat investment and help deepen financial markets over time.

We also expect to play an increasing role in transition and sustainable finance, particularly as industrial and infrastructure investment in the region evolves. Sectors critical to economic growth, such as manufacturing, transport and trade-linked industries, require capital to improve efficiency, resilience and sustainability. By applying disciplined risk management and robust sustainability frameworks, we can help clients access financing that supports both near-term growth and longer-term transition objectives.

Ultimately, our ambition is to act as a long-term partner to the region, using partnerships, innovative structures and our cross-border capabilities to help attract private capital, support sustainable trade flows and contribute to inclusive economic development across Central Asia. Through continued collaboration with multilaterals, governments and clients, we believe this model can be scaled to support the region’s next phase of growth.

By applying disciplined risk management and robust sustainability frameworks, we can help clients access financing that supports both nearterm growth and longer-term transition objectives.

CHAIRMAN OF THE MANAGEMENT BOARD AND CEO, JSC “UZBEK METALLURGICAL PLANT”

Steel is not just another industrial product. It has a multiplier effect across the economy. Mr. Abdullayev describes Uzbek Steel’s evolution from a producer of long products into a national steel platform delivering both long and flat steel, with the ICIECsupported Casting and Rolling Complex marking the company’s entry into flat steel production and strengthening domestic supply, localisation and export potential. He highlights how ICIEC’s risk mitigation helped make a strong project bankable by aligning its risk profile with international lenders’ requirements while looking beyond financing to Uzbekistan’s wider development value and points to future cooperation on raw material security and deeper downstream processing.

Could you share with us the strategic vision of Uzbek Steel and its role in supporting Uzbekistan’s industrial development and economic diversification?

Our strategic vision is to develop Uzbek Steel, JSC Uzbek Metallurgical Plant, widely known as Uzmetkombinat, from a producer of long steel products into a national steel platform supplying both long and flat products. This means expanding capacity, strengthening domestic supply, reducing exposure to external shocks and supporting deeper industrial processing in Uzbekistan.

Uzmetkombinat currently produces more than 1 million tonnes of metal products a year. With the ramp-up of the Casting and Rolling Complex, our annual steel production capacity is expected to increase to about 2 million tonnes. The purpose is clear: to meet domestic demand more reliably, reduce imports and strengthen export potential. A key part of this strategy is moving further along the value chain. Supported by ICIEC, the Casting and Rolling Complex marks Uzmetkombinat’s entry into flat steel production. The complex has been built and is now in ramp-up. It will create capacity for high-quality flat products, helping support localisation, downstream

A key part of this strategy is moving further along the value chain. Supported by ICIEC, the Casting and Rolling Complex marks Uzmetkombinat’s entry into flat steel production.

manufacturing and products aligned with international standards, including DIN.

Steel is essential for housing, infrastructure, mining, energy, machinebuilding and manufacturing. For Uzbekistan’s growing economy, a stronger domestic steel base improves supply reliability, cost predictability and economic diversification.

Uzmetkombinat has been part of Uzbekistan’s industrial base for more than 80 years. Commissioned in 1944, it is now the country’s largest ferrous metallurgy enterprise and supplies more than one third of the steel products consumed in Uzbekistan. In 2025, it was among the top 20 taxpayers in the manufacturing sector.

I came to this role after spending my professional life in private business and entrepreneurship. When the President entrusted me with leading Uzbek Steel in August 2025, the task was to bring a more business-oriented approach into a major state-owned industrial enterprise. In a short period, we have already achieved meaningful operational results, including a 25% increase in production volumes and an 18% reduction in production cost.

Uzmetkombinat is also Bekabad’s anchor industrial enterprise. The city of roughly 100,000 people developed around the plant. Our responsibility therefore goes beyond steel output and includes employment, skills and social stability. Our task is to modernise this base with financial discipline, operational reliability and a long-term view.

What are the main priorities currently guiding the company’s growth, modernisation, and competitiveness in both domestic and export markets?

Our priorities today are executionfocused. The first is the disciplined ramp-up of the Casting and Rolling Complex. Construction is complete; the focus now is on stable equipment performance, trained operating and maintenance teams, reliable process control and consistent product quality. This is the stage where long-term competitiveness is built not by installed capacity alone but by how predictably and efficiently that capacity operates.

The second priority is the modernisation of our existing production base. We are working to reduce production costs, improve energy and material efficiency, remove operational bottlenecks and make output more predictable. These improvements are important in the domestic market, where customers value reliability and delivery discipline, and in export markets, where cost, quality and timing determine competitiveness.

A further priority is raw material security. As production volumes increase, the company needs a more secure raw material base and better protection from fluctuations in scrap availability and pricing. We are therefore preparing projects that can strengthen supply stability, improve cost control and support higher production volumes over the long term.

Overall, our growth is guided by a simple principle: modernisation must translate into measurable operating results – stable quality, lower costs, reliable deliveries and a stronger position in both domestic and selected export markets.

How do you assess the role of the steel industry in supporting infrastructure, industrialisation, and broader economic development in Uzbekistan and the region?

Steel has a direct role in Uzbekistan’s growth. It is one of the basic inputs for construction, transport, infrastructure, energy, mining and machine-building. Demand is driven by population growth of around 2% a year, active construction and economic expansion of approximately 6 to 8% annually. Housing, roads, bridges, industrial facilities, utilities and energy infrastructure all require reliable steel supply.

For large projects, availability matters as much as price. When a country depends too heavily on imported steel, investors and contractors face greater exposure to logistics delays, external price movements and supply disruptions. Local production does not remove all risks, but it gives the economy more control, reduces pressure on foreign currency outflows and supports national manufacturers.