Corridors of Opportunities: From Azerbaijan to Central Asia Enabling Bankable Delivery through Risk Mitigation

H.E. MR. MIKAYIL JABBAROV

IsDB GROUP GOVERNOR FOR THE REPUBLIC OF AZERBAIJAN,

MINISTER OF ECONOMY OF THE REPUBLIC OF AZERBAIJAN

As Azerbaijan prepares to host the 2026 IsDB Group Annual Meetings in Baku, the country is reinforcing its role as a strategic bridge between Central Asia, the South Caucasus, Türkiye, Europe, and the wider Islamic world. Its growing importance in trade, logistics, energy security, investment, and regional connectivity makes it a timely focus for ICIEC’s Special Issue.

In this interview, H.E. Mr. Mikayil Jabbarov, Minister of Economy of the Republic of Azerbaijan and IsDB Group Governor for Azerbaijan, shares his perspective on the country’s economic priorities, including non-oil growth, industrial development, private-sector participation, renewable energy, and the reconstruction and reintegration of Garabagh and East Zangezur.

He also reflects on Azerbaijan’s deepening cooperation with Central Asia and the role of institutions such as ICIEC in derisking strategic investments, mobilising private capital, and helping turn regional connectivity into bankable opportunities for sustainable growth and shared prosperity.

As host country of the 2026 IsDB Group Annual Meeting, how would you assess Azerbaijan’s growing importance as a regional platform for economic dialogue, partnership, and investment cooperation?

Hosting the 2026 IsDB Group Annual Meetings in Baku for the second time is both an honor and a reflection of Azerbaijan’s growing role as a regional platform for economic dialogue, partnership and investment cooperation. This distinction demonstrates the confidence placed in Azerbaijan’s development path, modern infrastructure, institutional capacity and commitment to multilateral cooperation. This occasion also highlights the depth and continuity of Azerbaijan’s long-standing partnership with the IsDB Group.

The Islamic Development Bank Group has supported Azerbaijan’s sustainable economic journey through a comprehensive partnership that combines sovereign financing, privatesector development, trade support, and investment risk mitigation. This strong and multifaceted cooperation has played an important role in supporting Azerbaijan’s broader development objectives and economic transformation agenda.

The Annual Meetings will take place at an important stage of Azerbaijan’s economic development. Our current economic agenda places particular emphasis on expanding non-oil production and exports, improving the business environment and increasing privatesector participation. Over recent years Azerbaijan has made significant progress in strengthening the non-oil economy, expanding industrial and export capacity, and creating new opportunities across priority sectors.

Against this backdrop, the 2026 IsDB Group Annual Meetings will offer an important opportunity to present Azerbaijan’s economic progress and investment potential to a broad international audience. We expect the Meetings to generate practical discussions on financing strategic infrastructure, investment in priority sectors, regional trade and cooperation with IsDB member countries.

Azerbaijan is increasingly recognized as a strategic bridge between Central Asia, the South Caucasus, and global markets. How do you see the country’s economic role evolving in this wider regional context?

Azerbaijan’s economic role is evolving beyond that of a transit route, as the country assumes a broader role in regional trade, logistics, investment, energy security and digital exchange. Located at the intersection of the South Caucasus, Central Asia, Türkiye, Europe and the broader Islamic world, Azerbaijan is increasingly positioned as a practical economic bridge connecting production centers, consumer markets, energy systems and strategic transport corridors.

This transformation is supported by a range of strategic infrastructure projects that have strengthened Azerbaijan’s role in Eurasian connectivity. Transport assets such as the Baku–Tbilisi–Kars railway and the Baku International Sea Trade Port have enhanced East–West trade flows and reinforced the Middle Corridor. At the same time, major energy projects, including the Baku–Tbilisi–Ceyhan pipeline and the Southern Gas Corridor, have expanded Azerbaijan’s contribution to regional energy security and diversified supply routes to international markets. Together, these investments have strengthened Azerbaijan’s position as a reliable logistics, trade and energy hub serving Central Asia, the South Caucasus, Europe and other international markets.

The next stage is to translate connectivity into economic value creation. This is particularly evident in the growing importance of the Middle Corridor. Azerbaijan’s objective is to develop the corridor into a broader economic ecosystem that supports logistics services, industrial activity, processing capacity, private-sector participation and deeper regional integration.

Regulatory and operational coordination is equally important. Physical infrastructure must be supported by digitalized procedures, efficient customs and border management, transparent logistics services, and stronger coordination among corridor countries. These reforms are essential to reduce bottlenecks, shorten delivery times and make regional routes more predictable for investors and exporters.

A further dimension of this agenda is the TRIPP, which is expected to strengthen unimpeded links between the main part of Azerbaijan and the Nakhchivan Autonomous Republic. It is also worth mentioning that TRIPP has the potential to become an important component of both the Middle Corridor and North–South corridors, further enhancing regional connectivity and reinforcing the country’s role as a strategic logistics and trade hub across Eurasia.

Azerbaijan has significant potential in solar, wind, and other clean energy sources, including offshore wind in the Caspian Sea. In this context, Azerbaijan also supports several green energy corridor initiatives linking the Caspian region with European markets, including the Central Asia–Azerbaijan–Europe, Caspian–Black Sea–Europe, and Azerbaijan–Türkiye–Europe corridors.

The Black Sea Submarine Power Cable project and the trilateral cooperation among Azerbaijan, Kazakhstan and Uzbekistan are intended to expand renewable electricity generation and cross-border transmission.

At the same time, trans-Caspian digital infrastructure projects are strengthening data connectivity between Asia and Europe. Taken together, these initiatives combine transport infrastructure, energy transmission and cross-border digital networks within a broader regional framework. In this regard, the IsDB Group is a valued and natural partner for Azerbaijan as we advance this long-term vision of regional integration and sustainable development.

What are the key priorities currently shaping Azerbaijan’s economic agenda, particularly in relation to trade, investment, industrial development, and connectivity?

Azerbaijan’s current economic priorities include the expansion of the non-oil economy, higher productivity, increased private investment and the economic reintegration of the liberated territories. These priorities are supported by macroeconomic stability, continued improvements in the business environment and new opportunities arising from reconstruction and regional cooperation.

A key priority is to accelerate the development of the non-oil economy. This includes manufacturing, agriculture and agro-processing, information technologies, renewable energy, tourism and services. Growth in these sectors is important for creating skilled employment, expanding exports and reducing dependence on hydrocarbon revenues.

An equally important dimension of this agenda is the restoration and reconstruction of our liberated territories – Garabagh and East Zangezur. Beyond physical reconstruction, this process is focused on economic reintegration, the development of modern infrastructure, the return of economic activity, and the creation of new opportunities in agriculture, industry, tourism, renewable energy and logistics.

Another important priority is to improve the investment climate and expand private-sector participation through regulatory reforms, the digitalization of public services, stronger support for SMEs, public-private partnerships, and the continued development of industrial and free economic zones.

Transport and logistics also remain central to the economic agenda. Azerbaijan has invested significantly in transport and logistics infrastructure, including ports, railways, highways and air cargo capacity. The next priority is to increase the use of this infrastructure by expanding logistics services, industrial activity and exportoriented production.

Renewable energy and lower-carbon industrial development are also receiving increased attention. Ongoing solar and wind projects, together with regional electricity transmission initiatives, support energy security and create new opportunities for investment and industrial cooperation. These priorities are closely aligned with the IsDB Group’s work in infrastructure, private-sector development and trade facilitation.

Azerbaijan has been advancing major efforts in transport, logistics, and industrial development. Which sectors do you see as holding the strongest potential for future investment and cross-border collaboration?

Several sectors stand out as particularly promising for future investment and cross-border cooperation.

Azerbaijan’s position on the Middle Corridor creates strong opportunities in port services, rail and road logistics, warehousing, multimodal transport, customs modernization, and digital trade facilitation. Investment opportunities extend beyond transport infrastructure to port services, warehousing, freight operations, processing facilities and industrial production along the main routes. In this regard, Azerbaijan offers a number of important investment platforms, including the Baku International Sea Trade Port, the Alat Free Economic Zone (AFEZ), industrial parks, logistics centers and new infrastructure in the liberated territories and Nakhchivan.

Strategically located at the intersection of major railways, highways and maritime routes, and adjacent to the Baku International Sea Trade Port, AFEZ is emerging as a key industrial and logistics hub with seamless access to multimodal transport networks and international trade corridors. Supported by its tax and customs incentives, simplified administrative procedures and competitive regulatory framework, the zone provides an attractive location for high value-added, exportoriented manufacturing and internationally traded services.

The emerging peace agenda also creates an additional regional dimension for this sector. The outcomes of the Washington meeting on 8 August 2025, together with progress in the peace process, could further strengthen Azerbaijan’s role in regional transport, logistics and trade. This evolving framework is expected to enhance connectivity across the wider region and support the development of more integrated and resilient supply chains.

Industrial sectors with significant potential include petrochemicals, construction materials, pharmaceuticals and food processing linked to regional supply chains. At the same time, agriculture and agribusiness offer strong potential for value chain development, while tourism and the wider services sector present growing opportunities for investment, diversification, and employment creation. Renewable energy also offers significant investment opportunities, with Azerbaijan advancing large-scale solar and wind projects that support both domestic energy supply and regional electricity trade.

Beyond these areas, the liberated territories – Garabagh and East Zangezur – create new opportunities for investment in manufacturing, logistics, construction materials, agro-processing, renewable energy and tourism. The special incentive mechanisms applied in these territories, including tax and social insurance benefits and other support measures for entrepreneurs, are designed to encourage investment, accelerate economic reintegration and support the return of business activity.Nakhchivan is another important investment geography. With its strategic location and improving connectivity prospects, Nakhchivan can become an important platform for production, logistics and trade between Azerbaijan, Türkiye and the wider region. The tax, customs and social incentives available to entrepreneurs operating in Nakhchivan further strengthen its potential as an investment destination.

Digital trade, fintech, e-commerce, smart logistics and public-sector digitalization also offer significant scope for cooperation with IsDB member countries. These areas complement Azerbaijan’s transport and energy infrastructure by expanding crossborder data flows, digital services and innovation partnerships.

In your view, how can multilateral institutions such as ICIEC contribute more effectively to Azerbaijan’s development priorities by helping de-risk strategic investments, mobilize private capital, and support crossborder economic cooperation?

Institutions such as ICIEC can play an important role in helping Azerbaijan prepare strategic projects for financing. Access to funding depends substantially on investor confidence, including predictability, transparency and effective risk mitigation.

ICIEC’s instruments are particularly relevant to export credit, investment protection and political risk mitigation. Export credit insurance, investment JUNE 2026 07 insurance and political risk insurance can help reduce perceived risks in strategic sectors such as infrastructure, energy, logistics and industrial development. This support is especially important for crossborder projects, where investors may be exposed to regulatory, payment, currency convertibility, transfer and other noncommercial risks.

ICIEC can also encourage greater privatesector participation by improving the risk-return profile of projects. Properly structured risk mitigation can help attract commercial banks, institutional investors, export credit agencies and private companies into long-term development projects, particularly where investors require additional comfort at early stages.

Additionally, ICIEC can support trade and export development by facilitating trade finance, protecting exporters and encouraging companies to enter new markets. For Azerbaijan, this is highly relevant as we seek to expand non-oil exports and strengthen our role as a regional trade and logistics hub.

We also see strong potential for closer cooperation between ICIEC, the wider IsDB Group, the Government of Azerbaijan, and the private sector in structuring wellprepared and financially viable solutions. The goal should be to move from project concepts to effective implementation – with clear allocation of risks, strong governance,

Azerbaijan’s position on the Middle Corridor creates strong opportunities in port services, rail and road logistics, warehousing, multimodal transport, customs modernization, and digital trade facilitation. Investment opportunities extend beyond transport infrastructure to port services, warehousing, freight operations, processing facilities and industrial production along the main routes.

and measurable development impact. The 2026 Annual Meetings in Baku will be an important opportunity to advance this conversation in concrete terms.

Looking ahead, what is your vision for deeper economic cooperation between Azerbaijan, Central Asia, and international partners in order to promote sustainable growth and shared prosperity?

Azerbaijan’s accession as a full-fledged participant in the Consultative Meeting of the Heads of State of Central Asia marks an important new stage in its engagement with the region. It reflects the growing recognition of the deep historical and cultural ties between Azerbaijan and the Central Asian countries, as well as their shared interests in trade, investment, transport, energy, industrial cooperation and regional development.

This format provides a stronger institutional platform for regular dialogue, closer coordination and the advancement of joint regional initiatives. It enables Azerbaijan to contribute more actively to discussions on transport corridors, regional trade, energy security, investment cooperation and sustainable development, while complementing its expanding bilateral relations with the countries of Central Asia.

Azerbaijan is also reinforcing these relations through practical investment and financing mechanisms. The Azerbaijan–Uzbekistan Investment Company supports joint investments, facilitates access to finance and promotes partnerships between the business communities of the two countries. It provides a practical mechanism for supporting joint projects and broadening access to finance in priority sectors.

The Azerbaijan–Kyrgyz Development Fund similarly supports the implementation of joint projects and the expansion of economic cooperation with the Kyrgyz Republic. By providing financial and institutional support, the Fund can help address financing constraints and encourage stronger links between businesses in both countries, particularly in areas requiring long-term investment.

Kazakhstan is another key economic partner of Azerbaijan in Central Asia. Cooperation covers trade, investment, transport, logistics, energy and industry. Particular importance is attached to the development of the Middle Corridor, stronger transport links across the Caspian Sea and more efficient connections between Central Asia, the South Caucasus and European markets. The joint investment fund established by Azerbaijan Investment Holding and Samruk-Kazyna Joint Stock Company provides an additional practical mechanism for bilateral cooperation. The Fund is intended to support the development of the TransCaspian International Transport Route and facilitate investment in various sectors of the Azerbaijani and Kazakh economies.

Relations with Turkmenistan are particularly important in transport, transit, logistics, trade and energy. Its geographic position and connections across the Caspian Sea make Turkmenistan an important partner in strengthening east–west connectivity. Closer coordination between ports, transport operators and relevant institutions can improve transit efficiency and contribute to more reliable regional supply chains.

Azerbaijan is also expanding its strategic partnership with Tajikistan. There is significant potential to develop cooperation in trade, investment, agriculture, industry, energy and transport. Stronger contacts between the private sectors and the identification of viable joint projects can further broaden the economic basis of bilateral relations.

Cooperation among Azerbaijan, Kazakhstan and Uzbekistan in the field of green energy also demonstrates the potential for largescale regional initiatives with long-term economic and environmental benefits. Joint efforts in renewable electricity generation and transmission can strengthen regional energy security, support the transition to cleaner energy sources and create new opportunities for investment and technological cooperation.

At the regional level, further progress will require simpler procedures, more efficient customs and border processes, compatible technical standards and better-prepared infrastructure projects. The IsDB Group, ICIEC and other international partners can support these efforts through financing, insurance and risk-mitigation instruments.

Looking ahead, Azerbaijan will continue to deepen its economic relations with the Central Asian countries and facilitate their access to markets in the South Caucasus, Türkiye and Europe. Priority will be given to joint investment projects, more efficient transport links and practical cooperation in trade, energy, industry and logistics.

SHARE:

De-risking climate-resilient trade and investment in the MENA region

Climate change risk in the MENA region has evolved into a core economic and investment challenge, shaping infrastructure planning, trade competitiveness and long-term capital allocation. Risk-mitigation instruments, including specialised insurance and credit enhancement solutions, can serve as catalysts in mobilising sustainable growth across the region.

Rising temperatures, prolonged droughts, increased flooding and water scarcity are undermining agricultural output, supply chains, energy systems and investment decisions across the region. For governments, lenders, exporters and project sponsors, climate resilience has now become a central component of economic security, infrastructure planning and long-term growth.

Dr Khalid Khalafalla, Chief Executive Officer, ICIEC

MENA sits at the centre of this transition. Countries across the region see the utility in diversifying their energy mix beyond hydrocarbons through scaling renewable energy to meet ever-increasing demand for electricity. These countries are also addressing the inter-connected challenges of water and food security and secure value chains. These projects require substantial long-term financing and strong risk mitigation structures to achieve bankability and attract private capital. This is where export credit insurance, political risk insurance, reinsurance and credit enhancement can help unlock climate-resilient development.

A region of strategic opportunity

Many ICIEC Member States have programmes in renewable energy, water security, transport and logistics, food systems and industrial diversification. With the MENA region having renewable energy corridors, desalination infrastructure, green hydrogen projects and a regional logistics network, it is poised to be one of the most important markets for trade credit and investment guarantees over the coming decade. These projects often involve long maturities, require international partners and sovereign-backed counterparties. In many cases, there is a high perception of risk, which raises financing costs and limits private sector participation.

ICIEC, as a multilateral insurer, offers credit enhancement instruments that help reduce the cost of lending, whilst its risk mitigation covers non-payment risk for financing parties and project sponsors due to commercial and political risks, making transactions and projects more viable overall. The result is greater participation by international and regional banks, stronger trade resilience and more diverse sources of long-term capital providers for various sectors that are crucial to climate adaptation and green growth.

Where de-risking is needed most

The strongest de-risking needs are concentrated in the water–energy–food nexus, a central pillar of MENA’s resilience agenda. Renewable energy projects, including solar, wind, waste-to-energy, and both blue and green hydrogen, require long-term financing and dependable offtake arrangements. Desalination, water reuse and sanitation infrastructure are capital intensive and often benefit from credit enhancement. Climate-resilient irrigation systems and localised agricultural value chains are crucial to reducing food import volatility and supporting rural economies.

Sustainable transport, green industry and climate-resilient urban infrastructure and social infrastructure also require substantial de-risking support. The same is true for trade in essential goods and services. Emerging carbon markets may become another area where insurance and guarantees provide market stability as regulatory frameworks mature. Across these sectors, ICIEC’s role is not only to support capital mobilisation but also to improve project bankability by reducing commercial and non-commercial risks that might otherwise keep lenders and investors on the sidelines.

ICIEC’s mandate and instruments

ICIEC is a member of the Islamic Development Bank Group and the only multilateral insurer operating exclusively on a Shariah-compliant basis. Its mandate is to facilitate trade and investment among Member States through Shariah-compliant export credit insurance, political risk insurance, reinsurance and credit enhancement tools. These instruments enable banks, investors, exporters, contractors and sovereign-backed entities to manage payment default, currency transfer restrictions, expropriation and breach of contract as well as non-honouring of sovereign obligations in long-term projects with a transboundary investment element. In practice, ICIEC helps direct capital toward projects and trade corridors that might otherwise struggle to secure financing.

A track record anchored in climate-relevant business

ICIEC’s track record shows how risk mitigation can support sustainable development at scale. Since ICIEC’s inception in August 1994, cumulative business insured has reached $138.9bn, including $17bn in 2025 alone. These figures underline the ICIEC’s continuing relevance as Member States seek to mobilise capital for development and resilience.

MENA represents ICIEC’s largest regional footprint. Total business insured in Member States located in MENA stands at about $110.9bn, nearly 80% of ICIEC’s overall portfolio since inception. Approximately $100bn relates to trade and $10.8bn channelled to inward and outward investment. This concentration reflects both the scale of economic activity in the region and strong demand for Shariah-compliant, development-oriented risk mitigation solutions.

Over the past decade, engagement in climate-related sectors has expanded significantly. ICIEC has supported clean energy projects since its inception, with $6.8bn insured for a renewable energy mix, including solar, wind and waste-to-energy. ICIEC has also facilitated $1.42bn in clean water and sanitation projects and $7.7bn in non-energy green projects between 2015 and 2025. Regional examples supported by ICIEC include political risk insurance for equity investors in the Benban Solar Complex in Egypt, which was the largest project of its kind; reinsurance for two wind farms in Türkiye; reinsurance support for the Sharjah Waste-to-Energy Facility; and major reinsurance support for the Riyadh Metro construction project under Saudi Arabia’s Vision 2030.

ICIEC’s developmental impact goes beyond sectoral coverage. In 2025 alone, ICIEC de-risked transactions and projects worth $450m of private sector capital, supported over 294,000 jobs and enabled 5,998 small and medium-sized enterprises to access essential goods and services. ICIEC also supported with $889m in coverage for social infrastructure and $408m in other key social development categories, as reported for the year. These outcomes and positive momentum encompass climate-resilient trade and investment, which will translate into tangible benefits for people, businesses and the planet. The ICIEC Climate Change Policy continues to embed climate considerations in underwriting, risk management and impact assessment, whilst membership in global partnerships such as IRENA’s Energy Transition Accelerator Financing Platform (ETAF) synergises the origination of green projects by connecting key stakeholders.

Challenges that warrant honest reflection

Scaling climate-related insurance in MENA holds great potential and necessitates de-risking solutions. In some markets, project pipelines remain thin and feasibility studies do not always meet international lender standards. Long tenors combined with currency convertibility and transfer risks can complicate structuring. Regulatory uncertainty, evolving carbon markets, limited climate-risk data and uneven local insurance and reinsurance ecosystems also continue to slow progress.

The water–energy–food nexus also demands more innovative coordination. Governments, multilateral development institutions, export credit agencies, reinsurers, financiers, investors and project sponsors need to work together more deliberately. None of these barriers are insurmountable; overcoming the challenges requires a more integrated public-private approach.

Practical pathways forward

Several practical steps could accelerate climate-resilient trade and investment. Multilateral insurers, export credit agencies, reinsurers, development banks and private insurers can embed and systemise risk-sharing arrangements to expand capacity and extend cover. Better project planning and preparation and stronger feasibility work would improve bankability earlier in the project lifecycle. Credit and political risk insurance and credit enhancement structures can crowd in private capital where its patrons are hesitant to commit.

Progress also depends on stronger climate finance ecosystems. It is important to coordinate national diversification strategies, local and regional reinsurance capacity, enhanced climate-risk data and objective impact measurement in a more optimal manner. More widely accepted regional frameworks for carbon trading and green investment would also reinforce market confidence. An overarching objective should be to connect risk mitigation solutions offered by ICIEC and peers, public-private partnerships in renewable energy, water, agriculture and transport, and to increase awareness of how insurance and guarantees can make projects viable.

Conclusion

Scalable capital alone will not deliver MENA’s climate transition. The MENA region needs effective institutional partnerships and risk management tools that can turn climate ambition into bankable, resilient and development-oriented projects. ICIEC’s role is to reduce the barriers associated with commercial and political risk in a way that catalyses trade and investment flows within a development-focused and Shariah-compliant framework. As Member States accelerate climate adaptation and energy diversification efforts, de-risking instruments will play an increasingly important role in mobilising effective capital, strengthening investor confidence and delivering impact at scale across the region.

Dr Khalid Khalafalla is CEO of The Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC).

SHARE:

Making ratings and blended finance work for impact delivery in sustainable development

Rony Azar

Country Manager at ICIEC

The achievement of the Sustainable Development Goals (SDGs) by 2030 is dependent on the ability of the global financial system to mobilise and distribute the capital on a level never experienced before (Lagoarde-Segot, 2020). It is empirically determined that the low- and middle-income countries are facing an annual financing gap of more than four trillion United States dollars in the quest to achieve both development and climate goals (Clark, Reed & Sunderland, 2018). Despite the growth in sustainable finance, ESG investment and impact-oriented approaches, capital flows are still not right in relation to development needs and are concentrated in less-risk and more-income situations (Theodos et al., 2024).

In this milieu, two processes, namely, ratings and blended finance play an important part in influencing decision making in investments. Although the functions of both mechanisms are to alleviate the information asymmetries and risk management, the existing structure and implementation usually do not contribute to meaningful impact reporting (García‐Sánchez & Noguera‐Gámez, 2017). To enhance sustainable development finance, therefore, a thorough knowledge of the functioning of these tools, their shortcomings, and how they can be re-focused to achieve development outcomes is needed.

The Power and Limits of Ratings in Sustainable Finance

Ratings play a pioneering role in international financial markets in terms of perception, pricing, and regulation of risk. The credit rating influences the cost of sovereign and corporate bonds, the qualification of institutional portfolios and the level of capital regulation (Grittersová, 2020). ESG ratings have also become authoritative through indicative effects on sustainability performance to any investor wishing to incorporate environmental, social and governance factors in decision-making (Ziolo et al., 2019). Within the development environment, ratings are used as a gatekeeping mechanism: they carry out whether nations, project or organisations are considered investment worthy by large groups of capitals (Fini et al., 2023). To this end, ratings have significant power in creating and affecting the flow of capital to the emerging and developing economies.

Sovereign credit ratings place more emphasis on the macroeconomic indicators that are short-term in nature such as fiscal balance, inflation control and external debt indicators that are medium-term in nature (Barta, 2024). Although these factors are key to the financial stability, they do not always reflect long-term drivers of growth such as investments in education, healthcare, climate change adaptability and institutional capacity. As a result, nations that pursue the needed, but capital-intensive development projects can face the burden of ratings and high interest rates on borrowing, despite the fact that the development projects increase resilience and productivity in the long-term (Apostolou et al., 2025). This dynamism creates a structural bias that shuns accurately the outlays necessary to meet the SDGs.

Different approaches used by the providers result in variations of evaluations, thus reducing their usefulness as tools of decisions (Hellweg et al., 2023). Most of the ESG ratings are on the effect of environmental and social matters on financial risks of firms instead of the practical impact of corporate operations. Good disclosure practices and risk management systems might enhance the scores but may not be translated into any measurable social or environmental results (Landi et al., 2022). ESG ratings are therefore often meritocracy-based, as opposed to outcome-based, and offer little direction on concentrating capital in high-impact development initiatives.

Impact Blind Spots in Current Rating Frameworks

The major weakness with the current rating systems is the fact that they cannot substantively measure the impact of development. The ratings seldom put additionality into consideration where additionality is whether an investment provides the effects that would otherwise not have been the case without the capital (Salzman & Weisbach, 2024). They also have complexities in taking into consideration contextual issues, including the base level of infrastructure, income or access to services in a particular country or community. Consequently, the impact of a particular project will have significantly varied outcomes of development across the geographical region, but ratings generally have a tendency to use homogeneous standards (Wang et al., 2023). Such blind spots lead to the capital allocation systems that tend to prioritise low-risk systems over high impact opportunities, and thus subversive to the transformational impetus of sustainable finance (Udohaya, 2025).

Blended Finance: Conceptual Promise and Practical Constraints

Blended finance has become a prominent approach to tapping into the private capitals by facilitating the development goals. It aims to correct market failures that would discourage private investments through a combination of concessional capital by the public or philanthropic sources with commercial investments (Havemann, Negra & Werneck, 2022). Blended finance fits well in the areas that are associated with the need to create a sustainable world such as renewable energy, climate resilience infrastructure, agriculture, healthcare, and affordable housing (Leal-Arcas et al., 2025).

Practically, blended finance has not been able to attain the preferred size and effectiveness. Mobilisation ratios (amount of private capital inflow raised on a unit of concessional capital) are often smaller than expected (Attridge, 2022). Development finance actors and the wide variety of public actors are characterised by risk aversion, which limits their readiness to support true first loss capital or to have uncertain returns (Lulek, 2025). As a result, blended finance is also used to finance projects and initiatives that would otherwise have probably gone on without concessional finance so in additionality and efficient allocation of limited public resources are questioned.

Weak Impact Accountability in Blended Finance

Lack of strong impact accountability is also another major threat facing blended finance. Despite development goals often being offered as the justification of concessional aid, the measurement of impact is often pushed to the second position in relation to financing structuring and raising capital (Dye, 2022). This poor accountability undermines trust among investors, policymakers and citizens and inhibits the ability to learn through experience and to improve on the coming transactions (Agu, Nkwo & Eneiga, 2024).

The Disconnect Between Ratings and Blended Finance

Ratings and blended finance are rarely developed in such a way that they complement each other and thus lose the chance to appeal to the private capitals. Conventional credit rating is often unwilling to give due credit to risk reduction conferred by blended finance instruments like guarantees, political risk insurances or subordinated capital (Sharma et al., 2023). Therefore, undermining the effectiveness of the blended structures in signalling and precluding many investments complete the requirements imposed by institutional investors.

On the other hand, blended finance deals in the rule of thumb are often short of standardised, plausible indications related to quality of impact and additionality to development (Yunita et al., 2023). As such, the engagement is still limited to development-oriented investors instead of the venturing into mainstream capital markets. Such a mismatch of ratings and blended finance consequently limits the effectiveness of these two mechanisms and their general effectiveness (Attridge, 2022).

Toward Impact-Adjusted Rating Frameworks

To contribute to the sustainability of development, rating approaches should transform to denote the risks and opportunities of long-term outcome of development. It requires the shift in the risk definition that should include climatic transition and physical risks, demography, human capital formation, institutional strength, and social connectedness (Di Febo, 2025). These dimensions are becoming known to be of substance to the economic performance and financial stability, but they have not been given enough weight that they deserve in traditional measurements.

Blended finance should also evolve if it is to have an effective influence in bridging the SDG financing gap. Replacement of transactions on a case-by-case basis with standardised platforms and vehicles can diminish expenditure.

Moreover, the additionality of development and the importance of concessional capital should be specifically noted in the ratings. Additional metrics or complementary evaluations may include find out whether investments increase access to fundamental services, strengthen resilience, or inclusive development, and these results would be improbable in the absence of blended finance assistance (Udohaya, 2025). More standardisation, transparency and outside validation of impact measures would be required to guarantee credibility and avert impact washing.

Reimagining Blended Finance for Scale and Effectiveness

Blended finance should also evolve in case it is to have an effective influence in bridging the SDG financing gap. Replacement of transactions on a case-by-case basis with standardised platforms and vehicles can diminish expenditure, light speed and create an acquaintance with investors (Lagoarde-Segot, 2020). Replications can be used to enhance the learning process, efficiency, and enable more participation by institutional investors.

More importantly, public and philanthropic capital should be prepared to take a real risk in situations where the impact of development is maximised (Clark, Reed & Sunderland, 2018). At the same time, the accountability of impact should be enhanced with the help of obvious goals, outcome measures, and incentives of a dependent nature. Different strategies can be used to match the financial terms and the delivery of impacts and improve the level of transparency (Theodos et al., 2024).

The Role of Public Policy and Institutions

The key role of matching ratings and blended finance with sustainable development goals is undertaken by governments, development finance institutions, and multilateral organisations. Reform of policies to enhance data quality, transparency and regulatory predictability is capable of minimising perceived risk and contributing to the attraction of investment (García‐Sánchez & Noguera‐Gámez, 2017). This change will increase fragmentation and streamline operations and multiply the retaliation of development finance actors.

Interaction with rating agencies is especially essential as it is necessary to make sure that the approaches are based on development reality and they are not strengthening structural bias (Grittersová, 2020). Through collaboration, both the public and the private actors might be useful in reformulating the financial norms to ensure greater resilience in the long run, inclusivity, and sustainability.

Conclusion

Blended finance and ratings are potent tools in the world financial system, but they are not ready to deliver at scale and efficacy to achieve sustainable development objectives. Ensuring that ratings and blended finance can become an effective delivery tool is not a technical issue alone, but it also represents a bigger set of concerns about incentives, institutional requirements, and political will. To transform sustainable development from a dream to a basement, the financial systems need to change in terms of perceiving not only risk and profits, but also the real-life performance supporting long-term wealth and stability.

SHARE:

Making Ratings And Blended Finance Work For Impact Delivery In Sustainable Development – Via Reinsurance

Rahmatnor Bin Mohamad

Manager, Reinsurance at ICIEC

Buyers of insurance, both retail and commercial, have generally no dealings with a reinsurance company because reinsurance is a business-to-business transaction. Therefore, most people are not even aware of the existence of reinsurers who, at their end, have historically maintained a relatively low profile. This has changed as reinsurers publicly emerged as safety nets for direct insurers hit by massive disaster losses.

In its simplest form, reinsurance can be defined as insurance of insurance companies. Most insurers generally operate within their national boundaries and often offer cover that is limited to certain regions and customer segments. The capital base of many of those companies is exposed to disaster risk and cannot be simply strengthened without affecting affordability. As such, insurance companies rely on “risk capital” from third parties, in the form of reinsurance, to absorb large losses that unexpectedly deplete claims-paying resources and reduce underwriting capacity (Culp and O’Donnell 2010). Insurers transfer some of their risks to reinsurers in order to protect their balance sheets and to free up capital which, in turn, enables them to provide more risk-bearing capacity to their customers.

Reinsurers can pay for catastrophic losses because of their global diversification of risk portfolios and investment, making protection more broadly available at lower cost and higher security. This is how reinsurance creates value. The essential role of reinsurance is to support recovery efforts after disasters (such as earthquakes, typhoons, and floods) strike. Reinsurers are able to support community recovery efforts by paying claims that help communities rebuild. Equally important is the contribution of reinsurers to alleviating the financial consequences of mortality and health shocks. The recent COVID-19 pandemic serves as a case in point where reinsurers support their direct insurance customers in paying the costs of those who fall ill with the virus and require medical attention as well as by compensating families that have suffered the death of the main breadwinner.

By paying a premium to their direct insurer(s), individuals, households and corporates seek protection against a wide spectrum of specific risks, ranging from car accidents to flood disasters. Direct insurers, in the reinsurance context known as cedants, pass on entire portfolios of risks (where usually all premiums and losses are shared) or large single risks (covering losses exceeding a certain threshold) to globally operating and diversified reinsurers. The original policyholder is not involved in this transaction — the direct insurer remains the contractual partner.

Reinsurers assume the risk and add it to their portfolio of diverse risks. Typically, reinsurers are careful to diversify geographically and by type of risk. In order to limit their own exposure, reinsurers may sometimes pass on some of their risks to other reinsurers (known as retrocession) or to institutional investors who invest in insurance-linked securities.

The Economic and Societal Benefits of Reinsurance

Reducing the cost of risk on the back of global diversification

Insurance is fundamentally about pooling: individuals or companies pay a premium in return for financial compensation in the event of a covered loss. The premium paid by the insured (the ‘policyholder’) is calculated so that it allows the insurer to honour its claims payment obligations and meet its non-claims costs such as administration expenditure and the cost of capital. Insurance premiums are a function of the risk covered: the greater the probability of the risk occurring and/or the potential severity of the risk, the higher the premium.

Insurance essentially works as a redistribution mechanism: the premiums paid by policyholders who experience no (or little) claims finance the indemnification of those who are less fortunate. This mechanism works because not all policyholders suffer a large loss at the same time. It is in this sense that the ‘pluricentennial’ motto of Lloyd’s of London — which defines insurance as “the contribution of the many to the misfortune of the few” — shall be understood. This principle of “collective solidarity” which constitutes the very foundation of the insurance and reinsurance business model is rooted in science. The underlying mathematical principles are known as the ‘law of large numbers’ and the ‘central limit theorem’. Intuitively, they state that when one combines a large number of risks which, to a significant extent or at least to some extent, are independent from each other, there is a ‘compensatory’ effect between these different risks. In the case of insurance, this effect occurs between the policyholders who suffer a loss and the policyholders who are not impacted. On this basis, the aggregate loss experience over the entire risk portfolio becomes relatively ‘predictable’. In other words, aggregating a vast number of individual policyholders’ risks creates a risk portfolio which benefits from a lower volatility of claims. How does this mechanism enable the insurer to offer coverage at a lower cost?

Insurers are required by regulators to hold capital that is sufficient to absorb large losses and meet their commitments to all their policyholders with a certain probability, which can be seen as a ‘security level’. The corollary to the diversification effect is that, for a given security level, the total amount of capital that the insurer is required to hold decreases in relative terms when its risk portfolio becomes more diversified, everything else being equal. In other words, diversification reduces the amount of required capital for the coverage of a given policyholder risk and, consequently, lowers the ‘cost’ of insuring that risk.

Now enter the distinction between insurance and reinsurance. It primarily lies in the ability to pool risks. Most insurance companies — including the very large ones — have a local, national or regional footprint, due to the need to maintain distribution networks and close contact with their customers. Therefore, insurers only mutualize risks on a limited geographical scale. While this level of mutualization is sufficient for smaller risks that occur frequently, it may turn out to be insufficient for certain peak events such as a large natural catastrophe hitting a significant proportion of property insurance policies within a given country. For such a catastrophe, risk mutualization needs to be operated internationally or even globally. This is precisely the role of reinsurers. Contrary to most insurers, reinsurers generally have an international or even truly global footprint, allowing them to pool and mutualize risk exposures worldwide.

This is at the heart of the fundamental value proposition of reinsurance companies: they are able to assume a specific unit of risk at lower capital charges and cost than primary insurers who are limited to mutualization on a national level only. This differential in capital requirements for a particular block of business reduces the cost of risk and constitutes the added value of reinsurance, benefiting all insurance policyholders. It also explains why reinsurance is intrinsically a global industry, relying on diversification of risks across the globe, a wide spectrum of business lines and geographies.

Improving Availability and Affordability of Insurance

By leveraging global diversification, reinsurance is an efficient source of capital for direct insurers. Tapping into it increases insurers’ risk underwriting capacity and allows them to issue insurance policies with higher coverage limits, notably for those peak risks which need to be diversified globally and, in the absence of reinsurance protection, could remain completely uninsured. In other words, reinsurance allows insurers to provide more substantial and/or affordable insurance coverage to their individual policyholders, making the latter benefit from the diversification benefit afforded by global risk spreading through reinsurance. By enabling more and less expensive insurance, reinsurers make a vital contribution to narrowing global protection gaps, i.e. the difference between economic and insured losses.

Enabling innovation

In addition to providing cost-efficient capital, reinsurance is also an enabler or an outright source of innovation, not least due to the major players’ proprietary catastrophe modelling capabilities which have spurred the insurability of major natural disasters, for example. Efforts to model cyber exposures are a more recent example. Also, reinsurers play a major role in supporting their customers’ product development, for example in the areas of critical illness and occupational disability. Ultimately, reinsurers’ innovative credentials help expand the limits of insurability, deepening and broadening available insurance cover and narrowing protection gaps. Having said this, reinsurers face challenges, too, in this context as the frequency of non-modelled risks seems to be rising and climate change trends are blurring the ability to forecast natural disasters.

Disseminating risk knowledge and building risk awareness

Risk knowledge is in its essence, putting a price tag on risks, so society can allocate resources to risk mitigation in the most effective way. As many risks are interconnected and global in today’s world, reinsurers, based on their global pool of data and expertise, are a key resource for tracking these connections and making all stakeholders aware of them. Examples include:

Longevity, which is influenced by food security, nutrition, climate change, public health care and education. All these influencing factors vary by country and region but are interconnected at the same time. Understanding these interconnections makes it possible to design sustainable pension solutions and provide (real-time) prevention and other services to insureds.

Renewable energy is key to mitigating climate change. But the sun does not always shine, droughts make hydropower unavailable, and no wind means no energy. Insurance coverages for the lack of sunshine, water or wind smooth revenue streams and make renewable energy projects more attractive to investors. This ultimately accelerates the energy transition.

Climate change affects the frequency and severity of natural catastrophes, something that the reinsurance industry generally expects and models. For example, 2020 was another active year for natural catastrophes in the U.S. with a record-breaking 30 named storms in the Atlantic and a widespread wildfire season on the West Coast. Insuring farmers, homeowners, businesses, etc. against these perils provides economic stability even if disaster strikes, thereby assuring better livelihoods for the growing population on our planet.

The cyber space has developed into the backbone of modern economies. Today, cyber insurance helps companies to be back online fast, so that the damage from cyber attacks and incidents does not jeopardize their survival.

All of the above is only possible if risks are identified, assessed for frequency and severity, and analyzed with an eye to their potential for mitigation so that affordable premiums commensurate with the risk can be determined.

The first step in the risk management examples above is the identification of new or “emerging risks”. Emerging risks come with high uncertainty. They have still to be modelled and are potentially unquantifiable, or they evade or challenge current modelling. Examples include risks associated with new technologies like genetic engineering, nanotechnology, robotics or artificial intelligence.

By identifying and analyzing emerging risks the reinsurance industry provides a societal service. As an absorber of peak risks, reinsurance has developed a unique focus and expertise when it comes to scanning for emerging loss accumulations.

By identifying and analyzing emerging risks the reinsurance industry provides a societal service. In an important second step, reinsurance is instrumental in translating these risks into widely available and affordable insurance solutions. As an absorber of peak risks, reinsurance has developed a unique focus and expertise when it comes to scanning for emerging loss accumulations. Also, reinsurers’ emerging risk research not only enables potential prevention measures but also helps identify limits of prevention and insurability.

Enhancing Macroeconomic Shock Resilience

Re/insurance cover significantly helps economic recovery following a natural catastrophe, as shown in various academic studies (Von Peter et al 2012, Breckner et al 2016, OECD 2018). According to these studies, a higher level of coverage in general is accompanied by significantly better economic performance following a catastrophe. This effect is measured by the long-term effects of large natural disasters on economic activity. If fully insured, these events do not have a significant lasting effect on a country’s GDP level over the longer term. On the other hand, in the absence of insurance cover, there is evidence of a lasting negative effect on economic activity.

Large-scale natural catastrophes have massive economic effects, both direct and indirect. Besides the immediate negative effects resulting from the destruction of production sites, infrastructure, etc., the longer-term consequences should be considered as well. Emerging and developing economies in general are more heavily affected by extreme natural disasters than industrialized countries, not least because their resilience and preparedness levels are (much) lower.

The role of (re-)insurance in limiting the negative implications of extreme events and the resulting macroeconomic costs, especially for the most vulnerable countries, is multifaceted. First, given the global scope of reinsurance, affected countries can draw on readily available international resources to pay for losses. As shown before, this risk-bearing capacity can be provided more cost-efficiently than through self-insurance on a national level. Secondly, (re-)insurance provides incentives for loss prevention, e.g. through incentivizing better building standards. And finally, by setting a price tag on insured properties or business activities, insurance mechanisms increase the efficiency of disaster prevention — as opposed to post-event foreign aid inflows.

Contributing to Sustainable Development — via Reinsurance

By its very nature, reinsurance is an important contributor to achieving sustainable development. By mitigating major losses reinsurers smooth economic volatility and reduce economic shocks. Their extensive expertise uniquely positions them to contribute to the assessment and understanding of new, emerging and changing risks. Furthermore, reinsurers have a long record of driving innovation and the implementation of new technologies such as space technologies (satellites) or, more recently, green tech solutions.

Reinsurers are also well aware of their “corporate responsibility” and are committed to global initiatives such as the UN Sustainable Development Goals (SDGs), the Paris Agreement on Climate Change and many others. Global partnerships for sustainable development as well as voluntary commitments to standards such as those embodied by the UN Global Compact (UNGC), the Principles for Sustainable Insurance (PSI) and the Principles for Responsible Investment (PRI) are common for the reinsurance industry. A good example of cooperation between (re-)insurers and supranational organizations is the production of “Global guidance on the integration of environmental, social and governance risks into insurance underwriting” (UNEPFI PSI 2020).

As major institutional investors, reinsurers’ sustainable investing practices support sustainable development. Given the risk competency of reinsurers, the integration of ESG criteria into the investment process is well established in the industry. The establishment of sustainable investment guidelines is common practice in the investment management of reinsurers as are large-scale investments in renewable energy and sustainable real estate and infrastructure. Reinsurers have taken on innovative sustainable finance instruments such as green bonds. Also, initiatives such as the Net-Zero Asset Owner Alliance are supported by several reinsurers.

Climate change is one of the main causes of sustainability management. Its societal implications are manifold, ranging from physical and economic risks to changing business models and climate-induced migration (Munich Re 2021). The global reinsurance industry has been vocal about climate change and started to explore this phenomenon as early as in the 1970s, accumulating extensive data, knowledge and experience over the past five decades (Munich Re 2015). Reinsurers understand climate risks and are compensated for assuming such risks in order to support recovery efforts after disasters strike by paying claims that help communities to rebuild.

Reinsurers play an important role in helping societies adapt to climate change. They assume a portion of the financial burden of those affected by natural disasters, allowing them to return to their daily lives more quickly after a loss event. This role is particularly relevant for emerging and developing countries which are most vulnerable to natural catastrophes.

In addition to assuming underwriting risk, reinsurers also engage in a number of other activities and support measures that enable a more rapid adaptation to climate change. For example, they share information and provide education to raise awareness of natural catastrophe risks in both the public and private sector. They also assist in designing policy measures to incentivize the development of private sector risk transfer solutions (e.g. through conducive accounting and taxation rules) as well as Public-Private Partnerships such as catastrophe pools. In addition to risk-reducing insurance solutions geared towards loss prevention and adaptation to climate change, reinsurers also act as enablers of climate-friendly and sustainable technologies and support the transition to a low carbon economy. Knowledge and innovative coverage concepts help expand the frontiers of insurability and facilitate the breakthrough of new technologies. Insurance solutions enabled by reinsurance can protect against specific risks, thereby enhancing the appeal of green technologies for investors and strengthening their financing viability. This includes performance guarantees for renewable energy technologies (offshore wind farms and solar parks, for example) and support for hydrogen or methane fuel cell technology.

Conclusions and Recommendations

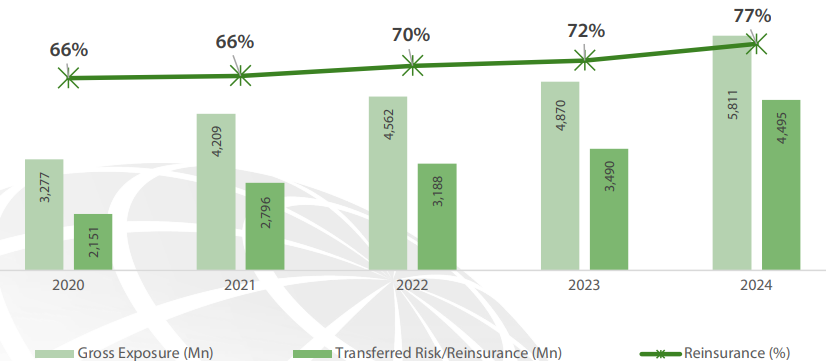

ICIEC has strategically leveraged the international reinsurance market to enhance its operational efficiency and expand its capacity. This prudent approach has strengthened portfolio diversification through effective risk transfer while improving financial flexibility. Notably, the reinsurance cession transfer rate increased from 66% in 2020 to 77% as of 2024, reflecting the continued strong support from the reinsurance market and ICIEC’s ability to optimise risk management by offloading exposures from its balance sheet. The risk transfer strategy also enhances ICIEC’s capacity and ability to support strategic and impactful projects in its Member States.

For reinsurance to benefit the economy and society it needs to operate globally. Global scale and risk diversification allows reinsurers to assume very large and complex risks in an affordable way. As such, reinsurers are a major source for stable and shock-resilient domestic insurance markets. In countries like Chile and New Zealand, for example, global reinsurers generally pay for the lion’s share of earthquake disasters, which otherwise may not be insurable at all, falling on domestic households, businesses and taxpayers in their entirety.

Reinsurance can play its economically and societally beneficial role only if certain basic policies and regulatory conditions are met. A key prerequisite is reinsurers’ unfettered ability to operate on a cross-border basis, i.e. the freedom to provide services. Reinsurers also require the ability to use their worldwide pot of premium to pay for local claims. Restrictions on the free flow of capital, e.g. through deposit requirements imposed on foreign reinsurers, impair their ability to move capital to cover major events which would ultimately drive up the cost of cover. (Source: GRF 2021)

Reinsurance Exposure (USD Mn)

SHARE:

Oman's Macroeconomic Situation And Growth Momentum

Moataz Zawam

Lead Underwriter (Operations, Sovereign Risks) at ICIEC

Oman’s economic outlook for 2025 reflects moderate growth, supported by ongoing structural reforms. Both the Ministry of Economy and the IMF estimate real GDP growth of around 2.2%–2.3%. Growth is driven mainly by the non-oil economy, which includes manufacturing, logistics, tourism, and services. These sectors continue to outperform hydrocarbon activities, which remain constrained by OPEC+ production caps.

Preliminary data from Q1 2025 showed GDP expanding by 4.7%, largely fuelled by robust non-oil activity. While crude oil production has been capped, natural gas output has partially offset this decline, helping maintain stability in hydrocarbon revenues. This diversification underscores the success of Oman’s long-term development agenda, which seeks to reduce reliance on oil while cultivating new engines of growth.

Government policy remains firmly anchored in Vision 2040, which emphasizes fiscal discipline, diversification, and structural reform. Fiscal performance has been strong, with surpluses recorded in 2024 followed by only a modest deficit projected in 2025. Public debt has fallen dramatically from a pandemic-era peak of more than 68% of GDP in 2020 to around 35% today, thanks to prudent fiscal management and conservative budgeting.

Monetary policy complements these efforts, focusing on price stability and investor confidence. Oman has one of the lowest inflation rates in the region, helping preserve household purchasing power and reinforcing business sentiment.

The manufacturing sector has become a critical driver of growth, expanding across petrochemicals, food processing, metals, and pharmaceuticals. Meanwhile, Oman’s strategic location at the crossroads of Asia, Africa, and the Middle East supports its transformation into a global logistics hub, underpinned by world-class port and transport infrastructure.

Vision 2040 and Growth Drivers

Oman Vision 2040, launched under the guidance of His Majesty Sultan Haitham bin Tariq, serves as the nation’s long-term blueprint for achieving economic resilience, social well-being, and environmental sustainability. It articulates a clear strategy to transition from an economy historically dependent on hydrocarbons toward one that is diversified, knowledge-based, and globally competitive.

Oman’s development trajectory is guided by Vision 2040 and the Tenth Five-Year Development Plan (2021–2025). Both place emphasis on non-oil sector expansion, foreign investment, and modern infrastructure. Non-oil GDP is forecast to grow by 2.7% in 2025, supported by investments in ports, industrial clusters, and logistics corridors.

Recent reforms, including the Foreign Capital Investment Law, have further liberalised the business environment and encouraged international participation. The Vision 2040 agenda enjoys support from key multilateral institutions such as the IsDB Group, IMF and World Bank, which have commended Oman’s steady progress on fiscal consolidation, legal modernisation, and private sector development.

Progress to Date

Oman has already diversified its non-oil revenues to account for more than 30% of GDP, supported by strong performance in logistics and manufacturing exports.

The successful issuance of green sukuk and the establishment of frameworks for Public-Private Partnerships (PPPs) demonstrate tangible steps toward achieving fiscal and environmental goals.

The roll-out of initiatives under the National Energy Strategy 2040 confirms Oman’s leadership in green transition within the Gulf Cooperation Council (GCC).

Creditworthiness has improved significantly. In 2025, Moody’s upgraded Oman to Baa3 and S&P confirmed BBB-, both with stable outlooks. These investment-grade ratings reflect strong fiscal discipline, lower debt ratios, and greater policy predictability.

Renewable energy is emerging as another major pillar. Large-scale solar and wind projects are underway, alongside ambitious plans in green hydrogen, positioning Oman to become a regional leader in sustainable energy. These initiatives align with global climate commitments while also generating new industries and long-term employment opportunities.

Despite ongoing global uncertainties, including volatile oil prices, geopolitical risks, and supply chain disruptions, Oman continues to deliver steady growth. Its ability to adapt to shocks highlights growing institutional capacity and a clear commitment to reform continuity.

Fiscal and Monetary Policy

Oman’s fiscal strategy remains cautious and disciplined. The 2025 budget anticipates a modest deficit of OMR 0.62 billion, consistent with conservative oil price assumptions of USD 60 per barrel. Public debt is expected to fall further below 35% of GDP, reinforcing long-term sustainability and supporting the country’s upgraded credit ratings.

The Central Bank of Oman (CBO) continues to prioritize monetary stability. Inflation has been well contained: the annual rate fell to 0.5% in August 2025, the lowest since late 2024, with an average of just 0.8% for the year through August. This reflects stable housing and fuel prices, effective supply chain management, and timely government subsidies. Price stability is central to economic confidence. By maintaining predictable inflation, the CBO provides an enabling environment for investment and supports household welfare. Together, prudent fiscal and monetary policies form a strong macroeconomic anchor for Oman’s medium-term outlook.

Development Agenda and Operational Resilience

The government’s development agenda is firmly anchored in Vision 2040, aiming to transform Oman into a diversified, innovation-driven economy. Key elements include:

Digitalization of government services to increase efficiency and transparency.

SME empowerment and entrepreneurship support to foster private sector-led growth.

Labour market reforms to improve productivity and attract talent.

Human capital investment, with a focus on education, skills, and youth employment.

Operational resilience has been evident in Oman’s capacity to maintain policy discipline despite volatile global conditions. Adequate foreign reserves and moderate debt sustainability risk provide buffers against external shocks. This resilience underpins investor confidence and strengthens Oman’s reputation as a stable destination for long-term projects.

Islamic Finance Proposition and Sukuk Developments

Islamic finance has become one of Oman’s fastest-growing financial segments. Shariah-compliant banking now represents over 16% of total sector assets, with steady growth expected as new players enter the market.

Sukuk issuance has expanded rapidly, attracting both domestic and international investors. Major issuers such as Energy Development Oman (EDO), Omantel, and the Oman Electricity Transmission Company have successfully tapped Sukuk markets to finance infrastructure and energy projects. This demonstrates the sector’s ability to mobilise long-term funding while aligning with ethical investment preferences.

Beyond traditional Sukuk, Oman has embraced Commodity Murabaha and Islamic trade finance solutions, particularly in manufacturing and logistics. Innovative instruments, including green and sustainability-linked Sukuk, are gaining traction, placing Oman at the forefront of Islamic financial innovation in the region.

By broadening funding channels and deepening the capital market, Islamic finance is helping diversify Oman’s financial system and support national development priorities.

Infrastructure and Project Pipeline

Oman maintains a strong pipeline of strategic projects designed to enhance connectivity, industrial capacity, and renewable energy integration. Key initiatives include:

Expansion of Sohar, Duqm, and Salalah ports, creating world-class maritime and logistics hubs.

Development of new highways and rail networks to improve regional connectivity.

Modernisation of airports to accommodate rising passenger and cargo volumes.

Upgrading of electricity transmission grids, supporting renewable integration and industrial growth.

Special Economic Zones (SEZs), particularly in Duqm and Sohar, are attracting international investment through public-private partnerships and targeted incentives. These clusters are set to become anchors of Oman’s diversification strategy, boosting export competitiveness and job creation.

Oman’s Relationship with the IsDB Group

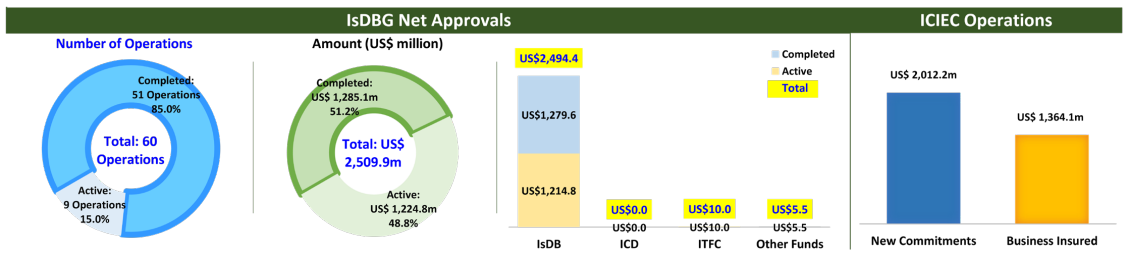

Oman has been a founding member of the Islamic Development Bank (IsDB) Group since 1974, with a subscribed capital share of ID 185 million (≈USD 530 million). Over the decades, Oman has received more than USD 2.5 billion in cumulative approvals from the Group, financing projects across transport, health, water, social infrastructure, and industrial development. These engagements are closely aligned with Vision 2040, supporting diversification, private sector growth, and sustainable development.

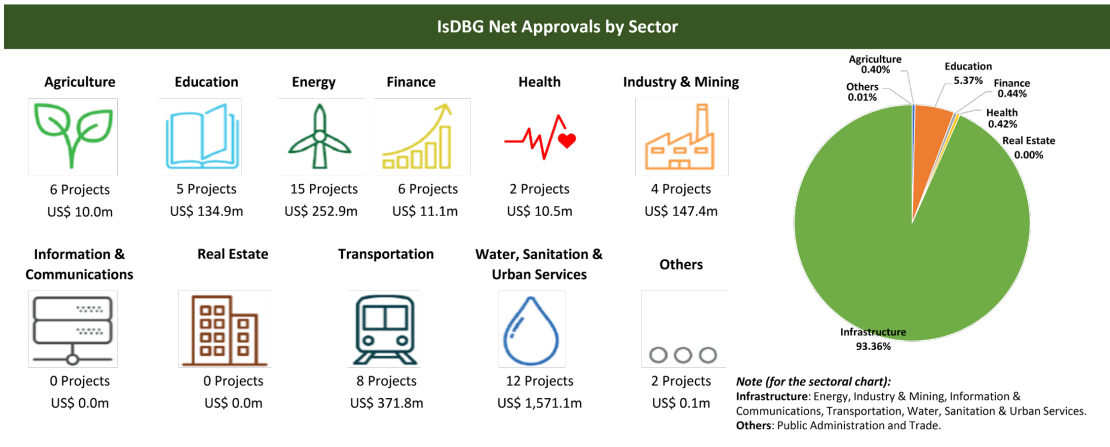

IsDB Group net approvalsIsDB Group net approvals by sector

ICIEC’s Engagement with Oman

Oman joined ICIEC in 2009 and has since developed a strong working relationship with the institution. ICIEC provides risk mitigation and credit enhancement tools that support both sovereign and private transactions in Oman. Coverage spans short-term trade credit, medium-term investment guarantees, and customized products for infrastructure and energy projects.

Selected Case Studies

Duqm Port Project (2018): ICIEC provided USD 114 million in reinsurance cover to Atradius, supporting the construction of a liquid bulk berth terminal in the Duqm Special Economic Zone. This project strengthened Oman’s logistics competitiveness by reducing transport distances and costs and enhancing export potential.

Sohar Port Expansion (2025): ICIEC signed a USD 40 million policy with Royal Boskalis for dredging and development works at the Sohar Port and Freezone South Expansion. The project will deepen navigation channels and upgrade jetty infrastructure, positioning Sohar as a leading regional maritime hub. It also supports the launch of MARSA LNG, the Middle East’s first LNG bunkering facility, underscoring Oman’s commitment to clean energy solutions. ICIEC’s coverage enabled smoother access to financing and ensured project bankability.

Through such transactions, ICIEC plays a catalytic role in mobilising foreign investment, promoting sustainable trade, facilitating Oman’s broader diversification strategy, and contributing directly to Vision 2040 objectives.

Opportunities for Deeper ICIEC–Oman Collaboration

Green and sustainable projects: ICIEC can support Oman’s ambitious renewable energy and green hydrogen agenda, particularly in attracting global investors to solar, wind, and hydrogen clusters.

PPP frameworks: As Oman advances public-private partnerships in ports, utilities, and logistics, ICIEC’s guarantees can help mobilise Foreign Direct Investment (FDI) and support the financial sustainability of these ventures.

Export diversification: With non-oil exports already accounting for over a third of Oman’s trade, ICIEC’s credit insurance products can further expand access to new and higher-risk markets in Africa and Asia.

SME support: By tailoring risk mitigation solutions for small and medium exporters, ICIEC can contribute directly to job creation and private sector empowerment, both key pillars of Vision 2040.

Outlook and Strategic Implications

Oman’s economy is projected to grow at 2.4%–3.4% in 2025, accelerating to as high as 3.7% in 2026 as OPEC+ production caps are gradually eased and non-oil momentum builds further.

Key Growth Drivers

Ambitious investments in logistics and industrial clusters.

Expansion of renewable energy, with a special focus on green hydrogen.

Digital transformation and SME development.

Continued reforms to the business environment and labor market.

Fiscal and external buffers will remain strong, supported by cautious budgeting and a policy of channelling hydrocarbon surpluses into debt reduction and infrastructure upgrades. Public debt is projected to remain below 35% of GDP, compared to more than 68% just five years ago, a clear sign of reform success.

Risks persist, including global oil market volatility, potential trade disruptions, and regional geopolitical uncertainties. However, the growing share of non-hydrocarbon exports (over one-third of the total), coupled with steady gains in manufacturing and services, provides important safeguards.

Over the medium term, Oman is set to redefine the Gulf development model—transitioning from resource dependence to a balanced, innovation-driven economy. Strategic partnerships with multilateral institutions such as the IsDB Group will continue to play a pivotal role, ensuring access to risk mitigation tools, strengthening investor confidence, and accelerating the realization of Vision 2040 objectives.

Conclusion

Oman’s economic transformation is gaining traction. The combination of fiscal discipline, strong credit ratings, growing Islamic finance, and an ambitious infrastructure agenda positions the Sultanate for sustainable and inclusive growth. With Vision 2040 as its compass and active partnerships with the IsDB Group, particularly ICIEC, Oman is steadily emerging as a regional benchmark for economic sustainability and diversification.

SHARE:

The Republic of Iraq – Economictransition and Development Priorities

Zaid Hiyasat

Country Manager, MENA Region Division Azzam Al Zahrani

Associate, Risk Management at ICIEC

Following years focused on reconstruction and stability, the Republic of Iraq is working to transition its economy from heavy dependence on oil exports toward a more diversified and sustainable growth model. The government’s development priorities include strengthening the private sector, improving infrastructure such as electricity and transportation, and modernising public financial management. Investment in agriculture, manufacturing, and digital services is seen as essential to create jobs for Iraq’s young and rapidly growing population. Anticorruption reforms and regulatory improvements are also central to attracting foreign direct investment and rebuilding investor confidence. This transition agenda is guided by Iraq’s Vision 2030 and translated into action plans through the National Development Plan (NDP) 2024–2028, which sets medium-term priorities across infrastructure, public services, and institutional reform. Long-term economic stability depends on fiscal reform, human capital development, and reducing vulnerability to fluctuations in global oil prices.

Hydrocarbons continue to play a central role in Iraq’s economy, providing the bulk of fiscal revenues and foreign exchange earnings. As a result, economic performance remains influenced by oil prices and production levels. At the same time, the authorities are increasingly focused on strengthening the foundations for broader-based growth, supported by gradual reforms and targeted investment.

Iraq enters this phase supported by stable financial foundations. Foreign exchange reserves remain sizeable, and external debt service obligations are relatively low. These conditions provide flexibility to manage volatility and support medium-term priorities, particularly in areas that enhance productivity, service delivery, and private sector participation.

At the institutional level, progress has been made in streamlining budget approval and improving execution rates, particularly for priority infrastructure programmes. Continued efforts to strengthen coordination, improve administrative effectiveness, and support implementation capacity are helping to sustain reform momentum.