The global climate crisis requires investment on an unprecedented scale for both mitigation and adaptation. At the centre of this challenge lies the energy transition, shifting from fossil fuels to renewable and clean technologies. Yet in many developing and climate-vulnerable economies, mobilising private capital faces major headwinds due to perceived and real risks.

Among the institutions seeking to address this gap is the Islamic Corporation for the Insurance of Investment and Export Credit (ICIEC), the insurance arm of the Islamic Development Bank (IsDB) Group and a committed Berne Union member. Through its Shariah-compliant credit and political risk instruments, ICIEC is working to de-risk investments in renewable energy and climate-resilient infrastructure in its 50 member states. Over the past year, ICIEC has refined its approach to climate finance, introducing new risk-sharing mechanisms. These initiatives aim to make climate projects more bankable by addressing constraints that limit private investment.

Global risk landscape: Scale and barriers

According to the International Energy Agency, annual clean energy investment must reach

USD 4.5 trillion by the early 2030s to remain on track for net-zero by 2050. Meanwhile, adaptation finance needs in developing countries could hit USD 340 billion annually by 2030. Public funds alone are not up to meeting this demand.

Yet for private investors, particularly in the markets where ICIEC operates, political and regulatory risks ranging from shifting policy frameworks to permitting delays continue to stall critical projects. Credit risk is another constraint, with concerns about off-taker solvency and sovereign payment reliability undermining project bankability. Currency convertibility and performance risks around newer low-carbon solutions such as green hydrogen and advanced storage add further layers of uncertainty. All of this is compounded by physical climate risks, including severe weather events that directly threaten infrastructure and livelihoods, and by transition risks such as the impacts of stranded assets and market shifts on economies that rely on traditional sectors. These risks deter investors and escalate capital costs, threatening the viability of essential climate projects.

ICIEC’s climate change framework

In 2024, ICIEC launched its comprehensive Climate Change Policy, fully aligned with the Islamic Development Bank Group and Paris Agreement principles and integrating sustainability across operations, products, risk management, capacity-building, and communication.

The policy’s pillars include improving internal operations by reducing ICIEC’s carbon footprint, optimising travel, and digitising workflows; prioritising insurance and reinsurance for renewable energy, circular economy, disaster risk management, and resilient infrastructure; embedding climate risk management across the entire risk framework; building capacity via training and knowledge-sharing; active engagement in the InsuResilience Global Partnership (IGP); and enhancing communication and transparency through Annual Sustainability and Development Effectiveness Reports.

De-risking and innovating in climate investment

ICIEC surpassed its target of dedicating 13% of total insured business to climate-friendly initiatives, reflecting a shift in portfolio composition towards sustainable sectors. As a multilateral insurer focused on development, ICIEC deploys and adapts robust, tailored solutions. Political risk, credit, and project finance insurance represent ICIEC’s core products for addressing investor concerns over expropriation, breach of contract, payment default, and currency inconvertibility, all of which continue to weigh heavily on clean energy projects in emerging markets. Through co-insurance and reinsurance partnerships with ECAs and MDBs, the corporation also extends capacity for larger and more complex transactions.

Recent projects highlight the measurable impact these tools are having. In Egypt, ICIEC’s provision of USD 68 million in equity insurance across four solar plants in the Benban Solar Park, one of the world’s largest photovoltaic complexes, helped attract international investors. The Benban project has enabled hundreds of megawatts of clean power and stimulated local job creation and supply chain development. In Senegal, ICIEC’s EUR 103 million insurance supported the installation of 50,000 off-grid solar-powered streetlamps in rural communities, boosting safety, extending productive hours, fostering rural economic growth, and contributing substantially to Senegal’s climate and energy goals. And in Türkiye, approximately USD 80 million in reinsurance supported the expansion of solar and wind energy, diversifying the national energy mix, improving energy security, and creating sustainable employment.

Circular economy and urban sustainability

Waste management and urban infrastructure are often overlooked in climate finance but vital for reducing emissions and improving quality of life. ICIEC’s cover for the Sharjah Waste-to-Energy plant, the region’s first commercial facility of its kind, helped divert more than 300,000 tonnes of waste from landfill and avoid roughly 460,000 tonnes of CO₂ emissions annually, while advancing Sharjah’s zero-waste target and creating green jobs.

In Saudi Arabia, a Shariah-compliant reinsurance facility of USD 360 million, arranged jointly with Atradius Dutch State Business, enabled global participation in one of the world’s largest urban transit developments. This transformative PPP modernises Riyadh’s transportation, cuts emissions and traffic congestion, and supports KSA Vision 2030’s urban sustainability objectives. Both cases highlight how risk-sharing can catalyse investment in large-scale initiatives with measurable environmental and social returns.

Resilience, water and food security

Across water and agricultural sectors, ICIEC has used political and credit insurance to support adaptation and livelihoods. In Côte d’Ivoire, EUR 107 million in cover facilitated the development of climate-resilient water infrastructure, enhancing health outcomes and agricultural productivity for millions. In Egypt, insurance for strategic desalination and sanitation projects supported adaptation to water scarcity in a changing climate. And in the West Bank, ICIEC partnered with MIGA to provide reinsurance cover for investment in seven date farms, packaging, solar energy, and cold storage. The project is a lifeline for local employment, women’s empowerment, and economic resilience through international export of premium Medjool and Barhi dates – all in a climate-stressed, fragile district.

Driving impact through partnerships and Islamic finance

In 2024, ICIEC inked 138 partnership agreements and deepened its collaboration with the IsDB Group entities, ICD (private sector), ITFC (trade), and major innovators like Masdar and IRENA through the Energy Transition Accelerator Financing programme. These alliances support climate finance mobilisation, technical innovation, and knowledge exchange across member states. The corporation is extending the reach of Islamic finance with Shariah-compliant solutions such as the Green/Sustainability Sukuk Insurance Policy. Green and sustainability-labelled sukuk now represent around 5% of total issuance, and volumes continue to grow as standards mature. The wider Islamic finance sector, valued at over USD 4 trillion, remains an immense but under-utilised source of capital for climate projects.

Scaling through project finance and PPPs

In 2024, ICIEC expanded its risk solutions to cover non-payment risks in project finance and public-private partnerships (PPPs), recognising their growing importance in scaling sustainable infrastructure. By combining public and private capital, PPPs enable risk-sharing and technical collaboration essential for the delivery of energy, water, and transport projects. As transition projects grow in scale and complexity, PPPs are emerging as the preferred model for mobilising foreign direct investment and driving innovation in emerging economies.

Providing the ‘oxygen’ for a sustainable future

Mobilising private capital to address the climate crisis remains one of the defining challenges of the years ahead. With an AA- rating and a developmental mandate focused on the most vulnerable regions, ICIEC is enabling member states to transform climate ambition into bankable, insurable reality. Through collaboration and its evolving de-risking toolkit, ICIEC is helping to build resilient, low-carbon economies; its recent initiatives illustrate how such models can align commercial and developmental objectives, drawing in private investment. These experiences point to the broader potential of partnership-based finance in building a greener, more equitable future.

In an era marked by relentless technological disruption-driven by advances in AI, blockchain, and digital trade-and compounded by shifting global trade patterns and mounting geopolitical tensions, the complexity of the global risk landscape has reached unprecedented levels.

In this dynamic environment, robust and adaptive risk management is not just important—it is indispensable. For ICIEC, the credit and political risk insurance arm of the AAA-rated Islamic Development Bank (IsDB), this challenge is especially acute.

With a core mandate to catalyse investment and trade across its Member States- often in high-risk markets-ICIEC must navigate this volatility with precision and foresight. Recognizing that traditional risk models are no longer sufficient, ICIEC has embraced a transformative approach. Moving beyond the conventional “one-size-fits-all” paradigm, the Corporation has redefined risk as a strategic lever-one that enhances capital efficiency, drives institutional agility and fosters resilience.

This new risk ecosystem balances capital preservation with optimization, guided by a calibrated risk–return lens tailored to its non-funding development mandate.

At the heart of this transformation, ICIEC’s risk management function has evolved into a forward-looking enabler of growth and innovation. From embedding dynamic portfolio analytics to advancing enterprise-wide resilience, risk now sits at the core of the Corporation’s transformation agenda.

Strong Institutional Foundation, Now Reimagined

Since its founding in 1994, ICIEC has served its 50 Member States through Shariah-compliant risk mitigation tools, solidifying its status as a global player in the Credit and Political Risk Insurance (CPRI) industry.

While historically focused on preserving capital and minimizing loss, ICIEC is now leveraging its risk function to optimize performance, unlock capital, and enhance insurance capacity—while maintaining conservative risk parameters to ensure all-time solvency and resilience.

Its strength is further magnified by the IsDB’s AAA-rated umbrella effect, benefiting from Preferred Creditor Status (PCS) and Preferred Creditor Treatment (PCT), which provide enhanced credit protection through sovereign support from Member States. As of 2024, PCT-backed exposures, from Sovereigns, State Owned Entities (SOEs), and Financial Institutions (FIs) of Member States, account for 88% (gross) and 80% (net) of ICIEC’s portfolio, reinforcing the quality and resilience of its insurance book.

Recent years have challenged the boundaries of risk management amid rising geopolitical volatility, climate-related shocks, inflation, and debt vulnerabilities. For ICIEC, this marked not just a moment for reflection, but a turning point for strategic transformation.

Risk Management as a Strategic Lever

ICIEC remains committed to operational excellence, continuously enhancing its underwriting, reinsurance, risk management, reserving, and internal audit functions. By maintaining a balanced approach, ICIEC supports Member States while ensuring a sound and resilient portfolio.

To align with evolving global risk dynamics, ICIEC has refined its Risk Appetite Statement (RAS 2.0) and Risk Management Framework (RMF 2.0). Key risk priorities for 2025 include:

- Enhancing portfolio reserving in compliance with IFRS 9 and IFRS 17.

- Implementing a Risk-Based Pricing (RBP) model.

- Advancing enterprise-wide stress-testing methodologies.

These initiatives are designed to strengthen ICIEC’s forward-looking risk capacity, enabling smarter decision-making and ensuring institutional resilience in a fast-changing world.

Capital Optimization and Financial Flexibility

ICIEC’s capital optimization journey gained momentum through the 3rd General Capital Increase (GCI), which raised the Authorized Capital to Islamic Dinar (ID) 1 billion (equivalent to USD1.4 billion). With over 87% of Member Country shares confirmed and phased payments already underway, ICIEC is significantly expanding its riskbearing capacity. The subscriptions so far have increased ICIEC’s insurance capacity by 57%.

Smart Growth Anchored in Resilience

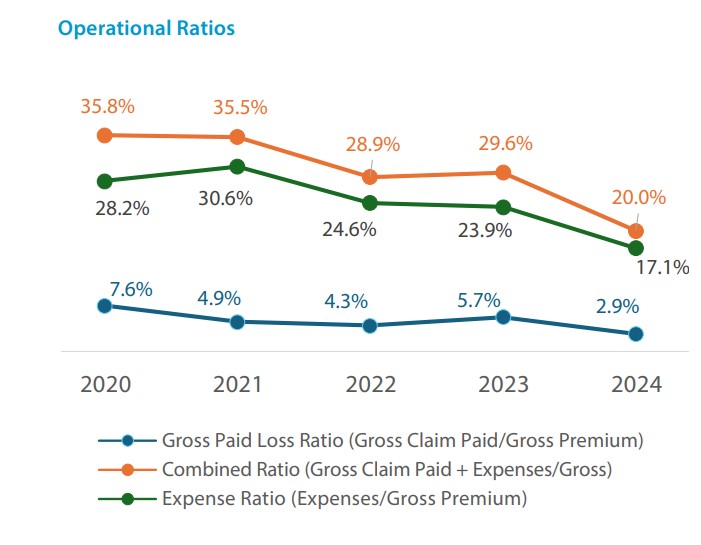

The outcomes of ICIEC’s redefined risk model are clearly visible. The Corporation posted a record net surplus of USD24.9 million in 2024, with its combined ratio improving to 20.0%, down from 35.8% in 2020. This was driven by enhanced underwriting and cost efficiencies.

From 2020 to 2024, ICIEC insured USD57.5 billion in new business, accounting for 47% of the cumulative total of USD121 billion since inception. Gross Written Premiums (GWP) rose 67%, from USD85.8 million in 2020 to USD143 million in 2024.

Gross exposure increased 16% annually. The 2024 exposure mix was 21% short-term (ST), 15% medium-term (MT), and 64% foreign investment insurance (FII).

Credit Rating and Capital Efficiency Impacts

ICIEC has maintained a Moody’s Insurance Financial Strength Rating (IFSR) of Aa3 for 17 consecutive years. In 2024, it secured an additional rating from S&P Global Ratings AA-, for both issuer credit and financial strength, which was reaffirmed in 2025 with a stable outlook. S&P also assessed ICIEC’s enterprise risk profile as strong and its financial risk profile as very strong. These high-grade ratings underscore strong market confidence in ICIEC’s risk management practices and financial resilience, positioning it among the top-rated institutions in its segment.

The AA- rating, further supported by the IsDB’s AAA umbrella effect, provides strong credit confidence and significantly enhances ICIEC’s stature in international financial markets. This high-grade rating allows financial institutions to assign only a 20% risk weight to exposures covered by ICIEC, thereby providing up to 80% capital relief under Basel regulatory frameworks. As a result, ICIEC becomes a more attractive partner for banks, reinsurers, and development finance institutions (DFIs).

For international reinsurers, the rating supports stronger capital calibration, enabling greater capacity for risk transfer involving ICIEC. Financial institutions and investors also view ICIEC-backed policies as high-quality instruments, improving their risk appetite.

Importantly for Member States, the AA- rating translates into more competitive pricing for ICIEC-covered capital market instruments, improving access to international finance and foreign direct investment (FDI). It also supports favourable treatment of ICIEC-guaranteed instruments as high-quality assets, thereby facilitating better financial terms and deeper investor confidence in projects across member states.

Looking Ahead: Risk as an Enabler of Transformation

ICIEC’s capital and liquidity planning, anchored in strategic alignment with the IsDB Group’s Strategic Framework and the phased GCI, positions it for sustainable expansion. Future initiatives include enhanced portfolio reserving, capital modelling improvements, and income efficiency analyses across business lines.

Looking ahead, key priorities include optimizing portfolio pricing, recalibrating capital modelling, and enhancing income efficiency across business lines. The annually published and quarterly updated Risk Perception and Portfolio Direction (RPPD) plays a central role in informing the Business Plan by guiding capital allocation across underwriting activities in line with the RAS.

For strategic and prudent capital allocation within ICIEC’s internal risk framework (EC based consumption), operating countries are classified into Low (Focus Market), Medium (Mixed Market), and High (Cautious Market) risk clusters, based on macroeconomic and geopolitical factors, providing a strategic framework for evaluating political and commercial risks.

Additionally, ICIEC is undertaking a comprehensive, forward-looking capital and risk assessment for 2026–2028, aligned with the upcoming IsDB Group strategic cycle. This assessment aims to integrate historical performance, capital consumption trends, and optimization metrics to ensure long-term solvency and capital efficiency. It is particularly timely as global trade and investment dynamics adjust to a new normal shaped by heightened political risk. The exercise also reinforces ICIEC’s commitment to developmental impact while maintaining financial resilience in an increasingly uncertain global risk landscape.

A Model for Smart Risk Management in Development Finance

At ICIEC, risk management has evolved from a traditional control function into a strategic enabler of institutional transformation. It now underpins the Corporation’s ability to deliver on its mandate with enhanced credit confidence, operational agility, and long-term sustainability.

This paradigm shift marks a fundamental redefinition—from merely preserving capital to prudently optimizing it for sustainable and inclusive growth. Risk Management now acts as a balancing mechanism and a bridge between business operations and the oversight role of internal audit, reinforcing its position as a second line of defense with strategic influence.

This transformation is especially timely as development finance institutions worldwide face mounting expectations to achieve greater impact within increasingly constrained capital and risk parameters. ICIEC’s smart risk approach directly responds to this imperative—balancing risk mitigation with the proactive pursuit of opportunity.

Amid global volatility, ICIEC has consistently outperformed expectations and demonstrated resilience—driven by a deeply embedded risk culture, sound governance, and a forward-leaning stance on economic and financial sustainability. It’s prudent underwriting and strategic capital optimization, and enterprise risk integration have positioned risk management not merely as a safeguard, but as a central catalyst for long-term development value creation.

ICIEC has maintained a Moody’s Insurance Financial Strength Rating (IFSR) of Aa3 for 17 consecutive years. In 2024, it secured an additional rating from S&P Global Ratings AA-, for both issuer credit and financial strength.

An Economy Undergoing Profound Structural Reforms and Transition How Nigeria Can Unleash Its Economic Potential

Economic Overview

Nigeria, Africa’s most populous nation and 4th largest economy by purchasing power parity, is undergoing a profound economic transition driven by structural reforms, rebalancing of fiscal policy, and renewed efforts to restore macroeconomic stability. The Government has embarked on a bold reform agenda aimed at reversing years of underperformance caused by oil dependence, fiscal leakages, and currency market distortions.

The Government focuses on large-scale privatization and asset sales as part of its economic stabilization measures. These measures aim to address balance-of-payment stresses and stabilize the economy.

According to the Central Bank of Nigeria (CBN), the economy is projected to grow by 4.17% in 2025, up from an estimated 2.9% in 2024. The International Monetary Fund (IMF) is slightly more conservative, forecasting 3.0% real GDP growth. Growth is supported by higher oil production volumes (approaching 1.6 million barrels/day), the full commissioning of the Dangote Refinery, improved FX liquidity, and rising non-oil sector contributions – particularly in agriculture, telecommunications, construction, and financial services.

Public investment is being catalysed by high-profile infrastructure projects, including the Lagos–Calabar Coastal Highway, rail line modernizations, and rural electrification schemes. The government also seeks to drive job creation through domestic value chains in agriculture, automotive assembly, and pharmaceuticals under its “Renewed Hope” economic agenda.

Nigeria does not currently have a formal IMF programme (such as an EFF or SBA), but maintains active engagement through technical consultations, surveillance missions, and Article IV assessments. The 2024 Article IV Consultation recognized the boldness of Nigeria’s initial reform momentum including fuel subsidy removal and FX liberalization but also warned of reform fatigue, inflation risks, and the need for better-targeted social safety nets.

While Nigeria has not pursued budgetary support from the IMF, it continues to draw on IMF policy advice to guide fiscal consolidation and monetary tightening. The IMF’s Debt Sustainability Analysis (DSA) rated Nigeria’s debt as sustainable but vulnerable to interest and exchange rate shocks, underscoring the importance of revenue mobilization and FX inflow management.

Nigeria remains a significant client of the International Development Association (IDA) and the International Bank for Reconstruction and Development (IBRD) and is implementing a wide range of Results-Based Financing (RBF) operations across education, power, social protection, and state-level reforms. One of the most notable developments in early 2025 is Nigeria’s decision to prepay USD500 million of its outstanding World Bank debt.

This prepayment is politically and economically significant as it reflects the renewed FX inflows and stronger fiscal buffers due to higher oil revenues and improved investor sentiment. It is designed to reduce debt service burden over the 2025–2027 period, freeing space for critical capital expenditures and potential market issuances (e.g., Sukuk). It also sends a positive signal to credit rating agencies and international capital markets, reinforcing Nigeria’s commitment to prudent debt management.

Ultimately and according to internal reports from the Federal Ministry of Finance and the DMO, the prepayment is also aligned with Nigeria’s broader Debt Management Strategy (2024–2027), which prioritizes:

1. Extending average debt maturities.

2. Increasing concessional debt-to-commercial debt ratios.

3. Using guaranteed and insured market instruments to access affordable long-term capital.

It is worth noting that in April 2025, Fitch Ratings upgraded Nigeria’s Long-Term Foreign-Currency Issuer Default Rating (IDR) to ‘B’ from ‘B-’ citing improved FX reserve buffers, strengthened fiscal management and fuel subsidy removal and stabilized and transparent exchange rate system through implementation of Bloomberg B-Matching System, progress in reducing inflation and rebuilding investor confidence.

Tackling Inflation

Nigeria faced intense inflationary pressure throughout 2023 and early 2024 due to subsidy reforms, FX devaluation, and food supply shocks. Headline inflation peaked at 34.8% in December 2024, before gradually easing to 24.48% in January 2025, driven by tighter monetary policy and relative currency stabilization. The IMF projects average inflation at 26.5% for 2025. The Monetary Policy Rate (MPR) currently stands at 24.75%, following successive hikes by the CBN’s Monetary Policy Committee to combat price instability.

The naira has seen reduced volatility after the unification of multiple exchange rates in mid-2023, with a more market-reflective FX window now in place. CBN has prioritized clearing its FX backlog and restoring investor confidence in the I&E window.

Current Account Situation

Nigeria has recorded a notable improvement in its current account position since 2023, marking a significant turnaround in its external balance sheet. In 2024, the country achieved a current account surplus of approximately USD6.83 billion, according to data from the CBN. This is a marked reversal from the USD3.3 billion deficit recorded in 2023.

This improvement was largely driven by a USD13.17 billion trade surplus, underpinned by robust oil exports and a sharp reduction in fuel import bills. Additionally, remittance inflows surged to USD20.9 billion in 2024, representing an 8.9% year-on-year increase. While service account deficits persisted, they narrowed compared to previous years, contributing modestly to the overall improvement.

On a quarterly basis, the current account surplus expanded from USD3.38 billion in Q1 2024 to USD5.14 billion in Q2 2024, reflecting stronger oil receipts, improved non-oil exports, and moderate import growth. Looking ahead, the IMF projects that the current account surplus will moderate, falling from 9.1% of GDP in 2024 to 6.9% in 2025, and further down to 5.2% in 2026, as oil prices stabilize and imports gradually pick up.

Foreign Exchange Liquidity

Foreign exchange (FX) liquidity in Nigeria has improved significantly since mid-2023, following the Central Bank of Nigeria’s decision to unify the multiple exchange rate windows and allow the naira to trade more freely under a managed float system.

This reform—implemented in June 2023—reversed years of rigid FX policies and was one of the most critical components of the new administration’s economic stabilization agenda. In the months following the reform, Nigeria faced acute FX shortages and volatile exchange rate movements, with the naira depreciating sharply in both official and parallel markets.

However, by early 2024, FX market conditions began to stabilize, supported by improved supply from oil exports, higher remittance inflows, and increased portfolio investment. CBN also undertook clearing of the FX backlog, estimated to be over USD6 billion in Q3 2023, with most of the backlog fully repaid by April 2024. This was a critical confidence-building measure for investors and foreign suppliers, many of whom had been waiting for months to repatriate funds or receive payments.

As of May 2025, Nigeria’s gross foreign reserves are estimated at approximately USD38.45 billion, up from USD33.1 billion in mid-2024. Net reserves, after accounting for swaps, forwards, and encumbrances, stood at USD23.11 billion at the end of 2024. The increase in reserves has been attributed to a combination of higher oil revenues, reduced fuel import costs, and inflows from Eurobond repayments, World Bank disbursements, and limited FX interventions by CBN.

To further deepen FX liquidity, the CBN has reintroduced and strengthened the “Willing Buyer, Willing Seller” window, allowing exporters, investors, and banks to set rates more transparently. The gap between the Investors’ and Exporters’ (I&E) window and the parallel market has narrowed considerably in 2025, declining from a peak of over 30% to below 10%, indicating increased confidence in the formal market.

Furthermore, FX turnover on the Nigerian Autonomous Foreign Exchange Market (NAFEM) has improved, with average daily trading volumes now surpassing USD200 million, compared to just USD75– USD100 million at the height of the FX crisis in 2023. The return of foreign portfolio investors to the Nigerian debt and equity markets – following the clearance of backlogs and interest rate normalization—has also provided fresh FX supply into the system.

However, despite these positive developments, structural FX demand pressures remain, especially for capital goods, refined fuel, and machinery. The government’s push for local production and import substitution under the Industrial Revitalization Roadmap, as well as the start of operations at the Dangote Refinery and other industrial zones, are expected to reduce long-term FX demand.

Debt Sustainability

The International Monetary Fund (IMF) concluded its 2024 Article IV Consultation with Nigeria in April 2024, providing a comprehensive assessment of the country’s economic landscape and debt sustainability. The IMF acknowledged the Nigerian government’s ambitious reform agenda aimed at restoring macroeconomic stability and promoting inclusive growth.

Nigeria’s public debt increased to approximately 46% of GDP by the end of 2023, largely due to the depreciation of the naira. While this debt level remains below the regional average for Sub-Saharan Africa, the burden of debt servicing has intensified. External debt accounts for roughly 16% of GDP and is primarily concessional, limiting exposure to commercial external risks. However, the country’s debt portfolio is heavily skewed toward domestic borrowing, which comes at high interest rates and presents rollover and cost-related challenges.

Nigeria: Public Debt Structure Indicators

Nigeria’s Active Cooperation with the IsDB Group

Nigeria is a significant and active member of the Islamic Development Bank (IsDB), having joined the institution on 3 November 1999. To date, Nigeria holds a capital subscription of ID4,298.51 million, representing 7.33% of total IsDB subscribed capital, making it the fifth largest shareholder in the Bank. The IsDB maintains a strong operational footprint in the country through its Regional Hub in Abuja, established in 2018, which also oversees development interventions in neighbouring West African states.

Nigeria has benefited from a wide-ranging IsDB Group portfolio, with more than 145 projects approved. Out of this, around 60% have been completed, covering critical sectors such as infrastructure, agriculture, education, and finance. The infrastructure sector alone accounts for over 89% of IsDB’s total financing in Nigeria, encompassing sub-sectors like transportation, water and sanitation, energy, information and communications, and urban development.

The Bank’s financing has been notably directed toward key national development priorities, with major investments in agriculture, education, finance and health, industry, and mining. IsDB Group entities have been active in Nigeria.

Since inception, the IsDB Group has approved a total funding of about USD2.2 billion for Nigeria. This includes USD1.24 billion in project financing by IsDB, USD333 million supported by ICD; USD537 million trade operations by ITFC, and USD90 million by other IsDB Group funds and operations.

Nigeria’s Special Relationship with ICIEC

Nigeria joined ICIEC in 2006, and since then the Corporation has insured over USD2 billion in cumulative transactions in Nigeria, historically focused on trade risk cover for Tier 1 banks. ICIEC is now expanding from traditional short-term trade finance to long-term investment guarantees and sovereign risk coverage. Since this shift, we were able to build up a comprehensive pipeline of transactions in several areas, including Islamic capital market instruments, as well as enhanced partnership with key local stakeholders.

ICIEC has successfully participated in the following initiatives and transactions:

- At the 2025 IsDB Group Annual Meetings in Algiers in May, ICIEC signed a strategic Memorandum of Understanding with NEXIM Bank, establishing a framework for collaboration in export credit insurance, reinsurance, joint product development, and institutional capacity building. The partnership aims to expand risk mitigation tools for Nigerian exporters and deepen NEXIM’s integration into the global Islamic insurance architecture.

- In 2024, ICIEC closed its first-of-its-kind sovereign-backed SOE (State Owned Enterprise) cover in Africa through Project Gazelle, a structured pre-export finance (PXF) transaction in favour of the Nigerian National Petroleum Company (NNPC). The cover mitigates payment risk while enabling NNPC to raise international financing based on its crude oil flows..

- Following the success of Project Gazelle, ICIEC has replicated this model through Project Leopard, which closed in 2025. Both transactions underscore ICIEC’s ability to innovate in complex structured trade finance and support national champions like NNPC through Shariah compliant risk mitigation..

- The Lagos-Calabar Coastal Highway, valued at USD1.067 billion (Phase 1 only), is backed by USD465.9 million in ICIEC insurance provided to major banks under a 7-year Islamic Murabaha structure with NHSFO cover. As ICIEC’s first sovereign NHSFO cover in Nigeria, the project is a milestone in regional infrastructure financing. It supports job creation, improves coastal connectivity, reduces travel time, and aligns with SDGs 8, 9, 11, and 13.

Berne Union Members Record Historic Highs in New Commitments in 2024 Despite Rising Geopolitical Risks and Supply Chain Disruptions as New Businesses and Investments in Green Clean Energy Flourish

Mr. Yuichiro AKITA ,

President of the Berne Union & Senior General Manager, International and Strategic Policy,

Nippon Export Insurance and Guarantees Company (NEXI) Japan’s Official Export Credit Agency

In times of global uncertainty comes both challenges and opportunities. As risk absorbers and mitigators the credit and investment insurance industry have a defining role to play to ensure the continued flow of trade and investment, the lifeblood of the global economy. In an exclusive interview, Mr. Yuichiro AKITA, President of the Berne Union (the International Union of Credit and Investment Insurers) discusses how members have consistently demonstrated resilience and innovation in responding to past crises, and through the development of new products, the launch of fresh initiatives, and enhanced collaboration with partner institutions, how they have actively worked to safeguard global trade and investment flows during these challenging times, and the unforeseen crises in the years ahead.

ICIEC Newsletter: The BU’s Export Credit and Investment Insurance 2024 Industry Report shows that members recorded a historic high of USD3.3 trillion in new commitments amid escalating geopolitical tensions, war, natural disasters, and economic headwinds. At the same time, members paid a record total of USD10 billion in claims across all business lines. Which aspects of the state of the industry is most heartening and gives hope that BU members and the industry at large are indeed in a good position to meet the current challenges in the industry and the global economic landscape?

Mr. Yuichiro AKITA: Amid rising geo-political risks, impacts of conflicts, and severe natural disasters increased supply chain disruption risks globally. Since recovery from the pandemic, inflation-driven costs increase deteriorated economics of projects globally. This has created headwinds for new businesses and investments, including clean energy technologies, such as offshore wind and EV sectors. Last year, in many developed countries, the ruling parties lost a significant number of seats in the national elections, the voters prioritized addressing domestic income equality, inflation countermeasures, and social instability, while interests in transition to a green or low-carbon economy or international cooperation in public policy issues appear to have become secondary.

Nevertheless, BU members recorded a historic high in new commitments. In relation to MLT (medium-and-long-term) space, the long-term trend towards increasing capacity of private insurers is evident, now they provide more than 20% of new MLT commitments annually. In addition, new commitments of renewable energy have increased steadily, amounting to USD15 billion in 2024 (2.5 times the level of 2019). We still expect to see solar and onshore wind power projects and other clean energy, such as geothermal biomass and nuclear power as well as sophisticated ancillary technologies, such as energy storage and carbon capture.

Lastly, the high claim payment showed the members’ indispensable function to increase clients’ resiliencies. It is important for BU members to promptly pay insurance claims for covered incidents to gain customers’ trust, which is also crucial for the future of the industry.

The mainstay of your tenure as BU President is the BU STRIDE initiative. Can you expand on the rationale behind this initiative and its progress towards strengthening the foundations of international trade and investment, and reaffirming the BU’s commitment to be “the guardians of free trade and foreign direct investment in this new era of uncertainty?

The theme of the BU Spring Meeting held in Croatia was “Resilience,” one of the pillars represented in STRIDE (Sustainability through Resilience, Innovation, Diversity, and Empowerment).

Among BU members, ECAs have played a vital role as national export credit agencies in complementing market failures during crises such as the global financial crisis and the COVID-19 pandemic, thereby supporting international trade and investment. Now, facing new uncertainties, we believe it is imperative – and indeed possible – to fully mobilize the tools developed and implemented over the years to fulfil our mission as guardians of trade and investment.

While this market-complementing role remains critical, the mission of ECAs has expanded significantly. Some ECAs now support the future export opportunities of their national industries, overseas investments, supply chain and resource security, and the growth of SMEs. In recent years, many ECAs have also engaged in supporting climate action, energy transitions, pandemic responses, and social infrastructure in emerging and developing countries. Even when these activities primarily aim to support national industries, they often bring social impact to developing countries. Moreover, in cases such as untied financing, the social impact in host countries itself becomes a primary purpose, rather than direct economic benefits to the provider country.

Given these realities, the work of ECAs can no longer be contained within the traditional framework of “export credit.” It is increasingly important for ECAs to recognize themselves as entities capable of contributing directly to sustainability and the SDGs. The BU STRIDE Presidential Platform that I advocate, as such, is a slogan to foster new innovations that enable BU to contribute to the realization of the SDGs, not only through ECAs but also in close collaboration with private insurers within BU and MDBs such as ICIEC and IsDB.

Under your erstwhile hat at NEXI you are familiar with ICIEC’s unique position as the world’s only Shariah-compliant multilateral insurer. Do you see an enhanced role for Islamic risk mitigation and credit enhancement solutions, albeit niche now, and what can the Berne Union do to help facilitate this?

Inter-agency cooperation requires significant energy and commitment, regardless of whether the partner is an Islamic finance institution or otherwise. A natural question arises: when one already has well-established relationships with trusted partners, why seek new collaborations? What benefits could outweigh the costs of building new partnerships? This question is shared by both parties when embarking on new relationships.

The challenge is even greater when partners have different approaches to business – differences in organizational missions, procurement rules, environmental and social safeguards, risk management methods, and risk appetites. Distinct characteristics, such as those found in Islamic finance, can further add to this complexity. However, collaboration becomes particularly meaningful when there are risk taking barriers that cannot be overcome alone but can be addressed together with a partner.

Reflecting on NEXI’s cooperation with ICIEC, despite differences in financing and insurance structuring, the partnership delivered greater benefits—such as enhanced intelligence, negotiation leverage, and deterrence in specific markets—making it easier to take on risks collectively.

It is essential to share the merits of such collaboration through mutual exchange of operational insights and case studies. BU serves precisely as such a platform, and we are eager to create further opportunities within BU to facilitate these meaningful engagements going forward.

A recent UNCTAD Report stresses that Political Risk Insurance (PRI) plays a vital role in de-risking investments and mobilizing finance towards achieving the UN’s SDGs. Between 2018 and 2022, PRI providers insured USD150 billion worth of projects in developing countries, including LDCs. UNCTAD findings point to low investor awareness, high costs, and inconsistent ESG standards as key barriers to credit insurance market entry. This has led to increased cost of finance due to higher risk premiums paid. Do you think that LDCs are getting a fair deal from the credit insurance industry?

The recent UNCTAD report has shed light on how Political Risk Insurance (PRI) can contribute to mobilizing private investment for the achievement of the SDGs, while also identifying the challenges that remain. For many years, the role of the BU and ECAs in advancing the SDGs has often been overlooked. In this context, it is highly encouraging and indeed groundbreaking that PRI has been highlighted so prominently. Furthermore, the outcome document of FFD4 has reaffirmed the importance of ECAs and the critical role of tools that mitigate risks associated with overseas investment. This report, therefore, marks a significant milestone in the field of development finance.

Although the importance of PRI is increasing amid rising geopolitical risks, a key challenge lies in the low awareness of PRI as a product and of Berne Union members who provide it. PRI is not new, yet only a limited number of national insurance providers actively offer it. Institutions such as SINOSURE, NEXI, and PwC on behalf of the German government have developed strong capacities, while many others possess limited underwriting experience or are not actively promoting PRI.

To address this, the Berne Union seeks to facilitate knowledge exchange among its members by sharing best practices in product design, underwriting, monitoring, and claims management. We also provide a forum to discuss marketing strategies and case studies, enabling members to learn how to re-enter the PRI market or expand their offerings.

Through these initiatives, the Berne Union is strengthening the PRI capabilities of its members, enhancing the global availability of PRI, and channelling greater private investment into SDG-relevant sectors. In doing so, we support sustainable development and resilience in emerging markets, contributing to a more stable and inclusive global economy.

In 2024, medium-and-long-term commitments by Berne Union members reached USD160 billion, with private insurers contributing over 20%, highlighting the growing synergy between public and private actors. In your view, how critical is this collaboration, particularly through instruments like untied support and working capital solutions for building resilience in the current global trade environment? Additionally, what role can the Berne Union play in facilitating more effective blended finance structures involving DFIs, ECAs, and MDBs to mobilize capital for sustainable trade and investment?

The role of ECAs is expanding well beyond traditional export credit to include support for overseas infrastructure development through untied financing, securing critical resources, and providing development finance that contributes directly to the SDGs. Alongside this, we are seeing greater participation by private insurers in the MLT finance sector, as well as increased reinsurance cooperation between ECAs and private insurers. Beyond ECAs, collaboration among MDBs, private insurers, and institutional investors through portfolio syndication and securitization is also gaining momentum. Such public-private partnerships are vital for expanding the industry’s overall risk capacity and for bridging gaps in trade finance and SDG financing.

Blended finance was one of the most widely discussed topics at FFD4. Currently, collaboration between MDBs and ECAs often involves a vertical risk split, with each institution cofinancing a distinct portion of a project. Looking ahead, we should advance to the next stage: horizontally slicing risk within a single project to leverage the differing risk appetites of ECAs— who back private investors and banks—and MDBs—who can assume higher political or project risks.

This approach can strengthen blended finance structures, attract greater private investment into high-impact SDG projects, and foster stronger, complementary roles among ECAs, DFIs, and MDBs to channel foreign direct investment more effectively while managing risks efficiently across all stakeholders.

As the Berne Union, we aim to provide a practical platform for deeper discussions that explore and advance this kind of ECA – MDB collaboration. Through this, we hope to contribute to further innovation in the field of blended finance and support sustainable development worldwide.

The International Credit Insurance and Surety Association (ICISA) recently highlighted the rising incidence of fraud and money laundering risks in credit insurance due to rising economic challenges, higher trade volumes and the appearance of advance fake document technology especially through the introduction of electronic trade documentation. How important is this development for Berne Union members and what is the Union doing to help member entities mitigate these risks?

There is a rapidly growing awareness among Berne Union members regarding the critical issue of fraud. This is a matter that directly impacts the trustworthiness and financial soundness of our industry, and it is essential that we address it collectively and effectively.

At the recent BU Spring Meeting, a dedicated session on fraud was held, where members actively shared their experiences and discussed current mitigation measures. This issue is particularly pressing for ECAs handling short-term export credit insurance, where the sheer volume of transactions exposes them to significant challenges, with numerous cases already identified in practice.

In July, the BU ECA Committee will host a dedicated exchange among ECA practitioners focused on fraud. While technological advancements continuously evolve alongside new fraudulent methods, we recognize fraud as a shared challenge for our industry. The Berne Union is committed to promoting ongoing information sharing among members as we work to safeguard the integrity and resilience of our sector.

Looking forward, what are the challenges ahead, and what are the lessons drawn from past crises such as the global financial crisis in 2008, the Covid-19 pandemic, and the ongoing conflict in Ukraine and the Middle East?

Berne Union members have consistently demonstrated resilience and innovation in responding to past crises, ensuring the continued flow of trade and investment—the lifeblood of the global economy. Through the development of new products, the launch of fresh initiatives, and enhanced collaboration with partner institutions, BU members have actively worked to safeguard global trade and investment flows during challenging times.

During the global financial crisis, members expanded untied financing to support working capital for domestic and international companies and developed direct lending mechanisms to secure short-term liquidity. These liquidity provision tools have since been effectively utilized during the European debt crisis and the COVID-19 pandemic. In Asia, even as the private trade credit insurance market contracted, a reinsurance network among ECAs was established to maintain regional trade flows, forming the foundation for ongoing ECA cooperation in the region.

Today, amid rising geopolitical risks and the ongoing war in Ukraine, untied financing is being used to support resource offtake projects for resource security. In the PRI domain, some ECAs have re-entered the market, offering innovative solutions that enable the underwriting of war-related risks even within conflict-affected regions.

We will undoubtedly face unforeseen crises in the years ahead. However, the tools developed during past crises and the strengthened inter-agency cooperation frameworks now in place have prepared us to launch new joint initiatives swiftly and effectively. The Berne Union is committed to serving as a catalyst for these collaborative efforts, ensuring our industry continues to support global trade and investment, even in the most challenging circumstances.

The global trade, investment, and business landscape is currently undergoing rapid changes and unpredictability, which requires an agile response across the spectrum of business and institutional functions, including resource mobilisation, risk mitigation, building resilience, and carrying out the mandates of multilateral institutions in line with the development agendas of their Member States. Mourad Mizouri, Manager of the MENA Region Division in the Business Development Department at ICIEC, discusses the challenges of volatility, uncertainty, complexity, and ambiguity in the post-pandemic era and how multilateral credit and investment insurers such as ICIEC are adapting and building organisational resilience going forward

The IsDB Group, as described by its Chairman H.E. Dr. Muhammad Al Jasser as being a Group “from the South, by the South, and for the South” will put in place 2 of 5 years of corporate strategy blocks to operationalise the recently approved 10-year Strategic Framework. The Group’s development interventions will focus on the Member Country, Regional (OIC) and Global levels.

During the past 50 years, the focus of the IsDB Group, was on utilizing its different services and group synergies with its private sector partners, facilitating resource mobilisation and investment inflows, unlocking trade opportunities, regional integration, and maintain the social wellbeing of our Member States.

ICIEC’s Shariah-Compliant Derisking Solutions

ICIEC as the insurance arm of the IsDB Group, has played an important role since its establishment more than 3 decades ago through facilitating more than USD121 billion of trade and investment transactions and projects in favour of our Member States, of which 80% was in trade and the remaining 20% in investment insurance.

In 2024, ICIEC, through its strong partnerships and diverse Shariah compliant de-risking instruments, facilitated more than USD12.9 billion of trade and investment transactions and projects benefiting 42 Member States with transactions spanning many sectors, especially the energy, infrastructure, agricultural, healthcare, and financial services sectors. These interventions helped create more than 45,000 jobs, reduced more than 300,000 tons of CO2 and supported more than 2,000 SMEs. Furthermore, more than 45% of our business insured in 2024 was under the South-South Cooperation framework, supporting also the mandate of boosting intra-OIC trade and investment, which will help in reaching the intra-OIC trade and investment target of 25% by 2025.

To support our Member States in difficult times, ICIEC has implemented a number of initiatives related to many key areas, including healthcare, food security, and renewable energy. In the healthcare sector and during the COVID era, ICIEC, in coordination with the Islamic Solidarity Fund (ISFD), set up an innovative structure, the ICIEC-ISFD COVID-19 Emergency Response Initiative (ICERI), to provide credit insurance to more than 20 Member States using ISFD grants. In this regard, ICIEC has been able to leverage the relatively small grant amount offered by ISFD by more than 270 times. The ICERI Programme helped unlock liquidity to finance at favourable terms and the inflow of critical supplies, which helped the beneficiary countries in recovering from the impacts of COVID-19.

Another important ongoing initiative is the IsDB Group’s Food Security Response Programme (FRSP), under which ICIEC has been able to provide more than USD1.12 billion in insurance coverage compared with a pledged amount of USD0.5 billion. Through such initiatives, ICIEC facilitated the import of essential goods by providing insurance against credit and political risks. It also stimulated foreign investment inflows to strengthen the supply chain, boost food production, and enhance storage capacities. Furthermore, ICIEC leveraged additional financial resources through well-planned reinsurance arrangements.

Similarly, ICIEC, since its establishment some three decades ago, has underwritten more than USD2.37 billion of business insured dedicated to the renewable energy sector, such as solar energy and wind energy farms used for infrastructure projects. Through this commitment to the UN Sustainable Development Goals – SDG 7 on Affordable and Clean Energy, we help our Member States’ transition to clean energy.

Importance of Synergies and Partnerships

From another perspective and given the importance of promoting the commercial and political risk insurance industry to support the efforts of Member States towards a sustainable economic development, especially at uncertain times, ICIEC continues to support their National Export Credit Insurance Agencies (ECAs) through reinsurance and capacity development programmes.

In this respect, ICIEC signed several reinsurance programmes with national ECAs in the form of a treaty or facultative reinsurance scheme in order to support them insure export and local sales contracts in their respective countries. Furthermore, ICIEC has provided capacity development programmes to the technical staff of these ECAs either directly or through an association such as the AMAN Union, the forum it jointly established in 2009 comprising commercial and non-commercial risk insurers and reinsurers (ECAs) in Member States of the Organization of Islamic Cooperation (OIC) and of the Arab Investment and Export Credit Guarantee Corporation (DHAMAN), with the mandate of enhancing the culture and business of trade and investment insurance in common Member States.

The AMAN Union plays a key role in promoting cooperation, information exchange, and capacity building among its members. It also offers a unique platform to strengthen business ties and risk mitigation strategies across Member States. (More information about the AMAN Union is available at: www.amanunion.org).

Going forward in 2025 and beyond, ICIEC is adapting its strategy in line with the IsDB Group’s new 10-year strategic framework anchored to the Member States’ current and evolving needs, through the implementation of an agile strategy and proactive strategic planning in line with the national development plans and priorities of Member States. This will require strengthening the current partnerships, mobilizing new resources, and adapting our business model.

According to the First Half 2025 results, and despite the current geopolitical tensions and financial difficulties affecting some of our Member States, ICIEC has been able to provide more than USD7.6 billion insurance coverage, a 28% increase compared with the same period last year. This achievement has been made with no claims paid. This shows ICIEC’s resilience thanks to its strong risk management culture and its readiness to always support Member States without jeopardizing our financial position and preserving our outstanding credit rating.

There are changing times in the global economy where no country is immune from their potentially disruptive consequences, which continue to unfold in the global trade, tariffs, and foreign direct investment (FDI) playbook. The order of the day seems to be fragmentation and reciprocity. For the credit and investment insurance industry, it means navigating new risks, but also new opportunities. Dr. Khalid Khalafalla, the CEO of ICIEC, surveys the cornucopia of current and future trends credit and political risk insurers must consider and how the industry, including ICIEC, is responding to the challenges and opportunities ahead.

Out of adversity from the uncertainties and disruptions in the ever evolving global economic, financial, and geopolitical landscape comes a remarkable propensity towards innovative out-of-the-box thinking as the credit and political risk insurance and guarantees industry become no exception.

In fact, it has doubled down in various facets with a dogged resilience, determination, and operational agility, which augurs well for the near-to-medium-term future of the industry.

The Berne Union (BU)’s Export Credit & Investment Insurance Industry Report 2024, unveiled at its Spring meeting in Dubrovnik in May 2025, for instance, reports that the new business underwritten by its members – including ICIEC in 2024, reached a record USD3.3 trillion directly supporting cross-border trade and investment. This was especially so for short-term Trade Credit Insurance (CTI) and political risk insurance (PRI), which increased year-on-year by 7% and 5%, respectively.

But beyond inherited legacy insurance models, the new playbook is already redefining and recalibrating risk metrics and approaches, including those relating to country risk, sovereign debt, and export credit and investment structures.

There is also the issue of emerging insurance taxonomies, such as the EU’s Omnibus 1 Package, aimed at helping Member States in their transition to a sustainable economy and ensuring the insurance sector is aligned with the EU climate goals and protecting financial stability.

While a proactive approach to navigating geopolitics is essential for businesses to thrive, especially in going beyond merely mitigating geopolitical risks to seizing the opportunities presented by the new world trade and investment order, they still need to contend with the manifold macroeconomic and industry trends that will impact the insurance sector in varying ways. These trends include:

1. According to Swiss Re Institute’s World Insurance Sigma Report, the global GDP growth (inflation adjusted) is expected to slow to 2.3% in 2025 and 2.4% in 2026 from 2.8% in 2024, and accordingly the global insurance industry is expected to follow the trend, with total premiums expected to slow to 2% this year from 5.2% in 2024, picking up marginally to 2.3% in 2026.

2. In the UK, the Financial Conduct Authority (FCA) is championing a more agile regulatory environment for financial services, including insurance, to become an engine for sustainable, innovation-led growth. The financial sector contributes over 8% of the UK’s GDP and represents a significant source of employment and trade. Regulation is seen as a growth catalyst, also encompassing a data-driven look at the evolving architecture of financial risk.

3. Sovereign credit ratings and OECD country risk classifications also exert a heavy influence on the ability of low-and-medium-income countries to access capital, influencing borrowing costs and investor appetites, a point that many ICIEC Member States have stressed is based on exaggerated perceptions of credit and country risk, legacy debt burdens, and short-term macro indicators, which in turn leads to higher costs of financing, including credit insurance and PRI premiums.

4. Electronic trade documentation and digitalisation facilitation, including in the insurance sector, according to a new study by UNCTAD, shows that countries continue to make progress in easing and digitising trade processes. The 6th UN Global Survey on Digital and Sustainable Trade Facilitation, conducted across 160 economies by UNCTAD, confirms that the global average implementation rate of trade facilitation measures currently stands at 72%, up from 68.6% in 2023. The survey shows improvements across all regions since 2023, with developed economies leading with an 86% implementation rate.

5. In fact, UNCTAD’s latest update reveals that global trade expanded by an estimated USD300 billion in H1 of 2025, despite a slower pace of growth, compared to a rise in global trade by about 1.5% in Q1, with a growth expected to accelerate to 2% in Q2.

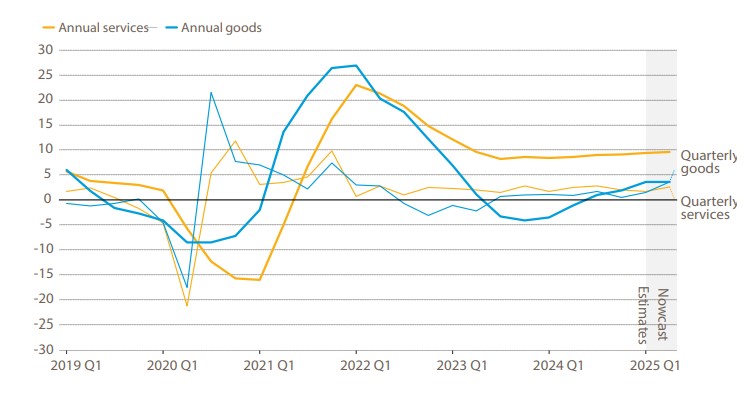

Global trade in goods and services remains strong in the first half of 2025

Annual and quarterly growth in the value of trade in goods and services, 2019–2025 Q1

Note: Quarterly growth is the quarter over quarter growth rate of seasonally adjusted values.

Annual growth is calculated using a trade-weighted moving average over the past four quarters.

Figures for Q1 2025 are estimates. Q2 2025 is a nowcast as of 17 June 2025.

Trade in services remained the main engine of annual growth, rising 9% over the last four quarters. Price increases contributed to the overall rise in trade value. Prices for traded goods edged up in Q1 and are likely to continue to rise in Q2, while trade volumes grew by just 1%.

Developed economies outpaced developing countries in Q1, reversing recent trends that had favoured the Global South. South-South trade stagnated overall, though Africa bucked the trend with exports up 5% and intraregional trade growing 16% year on year.

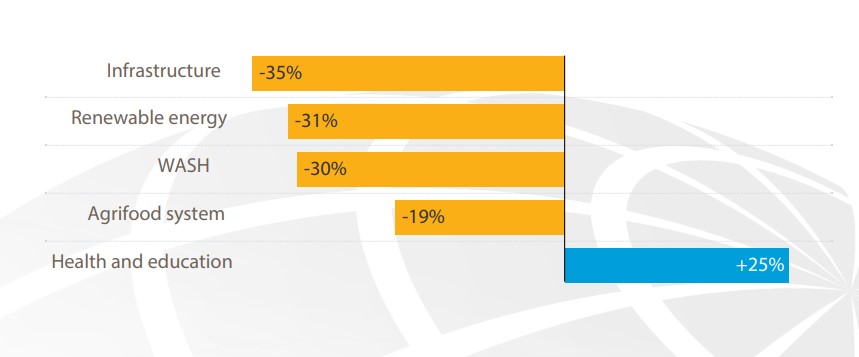

6. Similarly, global foreign direct investment (FDI) fell by 11%, marking the second consecutive year of decline and confirming a deepening slowdown in productive capital flows, according to the World Investment Report 2025, released by UNCTAD in June. Although global FDI rose by 4% in 2024 to USD1.5 trillion, the increase is the result of—among other factors—volatile financial conduit flows through several European economies, which often serve as transfer points for investments. The drop was especially steep in sectors critical to achieving the Sustainable Development Goals: renewable energy (-31%), transport (-32%), and water and sanitation (-30%).

Foreign investment in sustainable development fell sharply in 2024

International Investment in developing economies in Sustainable Development Goal sectors, percentage change of project values, 2023-2024

Note: WASH stands for water, sanitation, and hygiene

7. The credit and investment insurance preparedness playbook now encompasses several additional emerging trends. These include:

i. Digital resilience with agility by design, compliance, and automation all embedded. The bedrock remains collaboration in real time since risk, underwriting, and claims functions access the same data.

ii. In the dramatic rise in the resort to Artificial Intelligence (AI), the consensus seems to be that not every AI breakthrough warrants adoption. Insurers should focus on what delivers operational relevance and measurable added value.

iii. ECA collaboration is essential to accelerating project development and ensuring long-term resilience in critical mineral supply.

iv. The green energy industry and net zero momentum faced headwinds in 2024 from geopolitical tensions, trade barriers, and rising costs. While investments continue apace across sectors like wind, solar, and electrified transport, profitability and policy hurdles remain.

v. Rising debt burdens and tightening financing conditions are increasing pressure on low-income countries. Restructuring frameworks must now deliver greater coordination, clarity, and long-term sustainability, including possible write-offs.

vi. The Credit and Investment Insurance industry is similarly faced with rising fraud and AML/CTF risks, and fictitious trades and trade credit insurance claims are on the rise.

vii. The role of trade credit insurance in supporting SMEs, the backbone of economies worldwide, as governments are actively developing policies to support SMEs as a way of boosting productivity, innovation, and growth, albeit cost and margin management remain.

Perhaps the most interesting development emerged at the 4th International Conference on Financing for Development (FfD4), where global leaders addressed the widening gap between capital flows and development needs. The BU, UNCTAD, and the International Chamber of Commerce (ICC) convened a side event on ‘enhancing de-risking mechanisms for sustainable development’ to discuss how export credit guarantees, and political risk insurance (PRI) can be further leveraged to channel flows of long-term capital into developing economies and achieve sustainable economic development.

According to the BU, credit insurance and guarantees—both export-linked and untied—mitigate non-payment and political risks, enabling financiers to offer long-term financing for projects in developing countries that otherwise would not be feasible. These instruments support blended finance structures and improve access to affordable funding, especially in developing economies, making it possible for commercial banks to lend for renewable energy, health infrastructure, or public transport projects with reduced risk exposure. In fact, BU members currently hold USD507 billion in exposure in developing economies, a figure that has grown steadily since 2010 (USD323 billion). Within Least Developed Countries (LDCs), this figure has surged from USD15.9 billion in 2010 to nearly USD98 billion in 2024, demonstrating an increasing willingness to support the poorest countries.

UNCTAD at the FfD4 launched a policy review titled “Derisking investment for the SDGs: The role of political risk insurance.” Among investment derisking instruments, PRI, a type of insurance that protects cross-border investments from losses due to political events, such as expropriation, political violence, currency inconvertibility and breach of contract, has a critical and potentially growing role to play in fostering investment towards developing countries in general and LDCs in particular.

According to the Review, “PRI providers insured projects worth about USD150 billion in developing countries, including LDCs between 2018 and 2022. Developing countries (excluding LDCs) are the largest PRI beneficiaries (70% of the projects), where LDCs account for only 15% of projects covered by PRI. However, insured project values are equivalent to 28% FDI to LDCs, compared to 6% in other developing countries and 2% in developed countries. Export credit agencies (ECAs) are the primary providers of PRI, accounting for 78% of total issuance over the past decade, while multilateral institutions and private insurers account for 7% and 15%, respectively. Asia accounts for the largest share of PRI provided by ECAs and private insurers, reflecting China’s dual role as a major recipient of PRI and a leading provider, while Africa receives the most PRI from multilateral institutions.”

The investment gap to achieve the UN SDGs in developing countries by 2030, says UNCTAD, has widened from USD2.5 trillion to about USD4 trillion per year between 2014 and 2023. This chasm underscores the urgent need for effective solutions. The consensus is that public resources alone, including official development assistance, will be insufficient for bridging the financing gap, since mobilising private sector finance is critical, with a vital role for FDI to play.

The SDGs, in fact, have been a central tenet of ICIEC’s operations since they were introduced in 2015. We believe that trade and investment facilitation is an effective vehicle by which the SDGs could be achieved, as we are committed to supporting sustainable development, investing, and the SDGs. In this respect, ICIEC actively targets real impact and change in all its insured operations and acts as a catalyst for private sector capital mobilisation to be directed towards achieving the SDGs. This is done through ICIEC’s unique Shariah-compliant de-risking solutions, including the Non-Honouring of Sovereign Financial Obligations (NHSFO) Policy, the Foreign Investment Insurance Policy, Equity Investment Policy, and Reinsurance. This is achieved through forging Partnerships for Change in line with SDG 17 and with ICIEC’s Theory of Change strategy.

Rao Farid Khan,

Lead Legal Counsel and Head of

Claims and Recoveries at ICIEC

With some USD4 to USD64 trillion dollars wiped off US, European and global stocks in the two days after President Donald Trump’s declaration of “economic independence” and the imposition of a range of tariffs starting with a baseline 25% on steel and aluminium imports to the US, 10% tariffs for certain countries and a range of tariffs for other countries, the second-term Trump administration has disrupted the existing world trade, investment and business order. There are no signs of a retreat from this unilateral and isolationist US playbook which will impact every corner of the world including the US. Rao Farid Khan, Lead Legal Counsel and Head of Claims and Recoveries at ICIEC, considers the potential fallout for the credit and investment insurance industry and how the Corporation is positioning itself as a unique stabiliser and enabler of global and intra-OIC trade and investment.

President Donald Trump’s recent return to office and the policy shifts of his current administration have once again marked a critical juncture in the global economic landscape. Building on the disruptive strategies of his previous term, the renewed focus on protectionist trade policies, strategic decoupling, and a retreat from multilateral cooperation have intensified global economic uncertainty.

Actions such as renegotiating international trade agreements, reasserting national sovereignty over global institutions, and limiting U.S. engagement in global initiatives continue to challenge the foundations of international economic governance. These developments hold significant implications for global trade, investment flows, and credit insurance, potentially affecting the role and operations of multilateral institutions like ICIEC.

As a specialized multilateral insurer dedicated to promoting investment and trade among its 50 member states from the Global South, ICIEC now stands at a critical juncture. The current geopolitical and economic climate presents both elevated risks and profound strategic opportunities. The reinstatement of trade protectionism under Trump 2.0, marked by tariffs on imports from China, Europe, and various developing economies, has disrupted global supply chains and increased transaction costs. These changes have retendered cross-border commerce more unpredictable and significantly heightened the risk of defaults in international transactions. For the credit insurance industry, including ICIEC, this has led to a surge in demand for trade credit insurance, particularly from exporters in emerging markets who are increasingly seeking protection against non-payment risks and contractual disruptions.

In response to the current market challenges, ICIEC is uniquely positioned to play a crucial role in stabilizing and enabling trade. By enhancing its short-term credit insurance offerings and expanding its technical assistance services, ICIEC can develop robust credit insurance products tailored for high-risk markets, including the United States. This will provide vital support to exporters from its member states, helping them to remain resilient in the face of market volatility. Through these efforts, ICIEC not only fulfils its developmental mandate but also establishes itself as a dependable partner in an increasingly unpredictable trade environment.

Moreover, the U.S. retreat from key multilateral frameworks, such as the Paris Climate Accord and the World Health Organization (WHO), under President Trump has weakened the foundations of international cooperation. The diminished role of the United States in global governance has created institutional voids, particularly in areas such as public health and climate change. For multilateral insurers, this fragmentation imposes coordination challenges, undermining collective responses to systemic risks. However, this also presents a unique opportunity for ICIEC to assert leadership within its member states by deepening regional integration and fostering South-South cooperation.

ICIEC’s mission, grounded in Islamic principles of financial and insurance intermediation, allows it to offer a compelling alternative to the nationalist and isolationist rhetoric that has gained prominence. By promoting inclusive trade and investment models that prioritize sustainable development, ICIEC can emerge as a beacon of multilateralism and collaborative resilience amongst its member states. ICIEC’s ability to foster intra-OIC economic ties through innovative insurance mechanisms will be pivotal in offsetting the impact of global fragmentation.

Simultaneously, the Trump administration’s aggressive posture toward geopolitical hotspots such as Iran and China, has contributed to heightened regional instability and a more precarious global investment climate. These developments increase demand for Political Risk Insurance (PRI), which offers protection against risks such as expropriation, political violence, currency inconvertibility, and contract frustration. ICIEC can respond to this rising demand by broadening its PRI offerings and enhancing its insurance products tailored to infrastructure, energy, and social development projects in member states. By engaging in co-insurance and reinsurance partnerships with other Export Credit Agencies (ECAs) and private reinsurers, ICIEC effectively manages largescale exposures while supporting transformational projects that align with national development priorities.

The third pillar of the IsDB Group Strategic Realignment 2023-2025 focuses on driving green economic growth. By supporting climateresilient infrastructure projects and offering insurance solutions for green Sukuk and ESG-compliant investments, ICIEC facilitates sustainable development while managing emerging climate-related risks. This aligns with the strategic objective of driving green economic growth, as it promotes investments in sustainable and environmentally friendly projects, thereby contributing to the overall goal of green economic development. ICIEC’s Sukuk Insurance Policy, alongside its Non-Honouring of Sovereign/Sub-sovereign Policy, offers a framework through which it can mobilize capital for environmentally responsible projects and attract private sector participation in sustainable investment.

Perhaps the most defining feature of Trump-era economic policy is its unpredictability – a trait that intensifies demand for comprehensive risk mitigation instruments. In such a volatile global environment, credit and political risk insurance are not mere tools of financial prudence; they are essential components of resilience and continuity for governments, corporations, and SMEs alike. ICIEC can respond to this need by offering bundled insurance solutions that address both commercial and political risks, particularly in high-volatility markets. ICIEC’s ability to support small and medium enterprises (SMEs), which often lack the capacity to absorb shocks, will be critical in maintaining inclusive trade and investment flows.

By scaling up support for SMEs through agile credit insurance, diversifying political risk coverage, deepening regional collaboration, and pioneering climate-aligned insurance instruments, ICIEC can help build a more equitable and sustainable global economy.

Further, ICIEC can expand its capacity-building initiatives to enhance the risk mitigation capabilities of stakeholders in member states, thereby contributing to greater institutional and economic resilience.

The reality of Trump’s presidency and its current policies introduces new layers of complexity into the global trade and investment landscape, with potential trade wars, a NATO rethink, and the deportation of millions of migrants. Nevertheless, within this turbulence lies an opportunity for ICIEC to redefine its role and expand its influence. By embracing innovation, reinforcing strategic partnerships, and aligning its offerings with the values and aspirations of its member states, ICIEC can rise as a leader in the global credit and investment insurance domain. Its ability to navigate uncertainty while remaining committed to sustainable, inclusive, and ethical development will determine its trajectory in the years to come.

As the world continues to fragment and global leadership remains in flux, institutions like ICIEC are not only tasked with protecting trade and investment flows but also with enabling them in ways that are just, resilient, and aligned with long-term development goals. By scaling up support for SMEs through agile credit insurance, diversifying political risk coverage, deepening regional collaboration, and pioneering climate-aligned insurance instruments, ICIEC can help build a more equitable and sustainable global economy. The path forward demands strategic foresight, bold innovation, and a steadfast commitment to the developmental aspirations of the IsDB Group member countries. In this mission, ICIEC is not merely an insurer—it is also a catalyst for stability, growth, and shared prosperity.

Lotfi Zairi,

Associate Manager, Operations,

Sovereign Risks at ICIEC

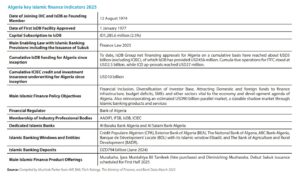

Lotfi Zairi, Associate Manager, Operations, Sovereign Risks at ICIEC, considers the important supportive and technical role that the IsDB Group and ICIEC could play in developing the Islamic finance industry in Algeria by enhancing its existing cooperation in trade and project finance and credit and political risk policy cover for Algerian entities through the Group’s Country Engagement Framework (CEF) and ICIEC’s pioneering Green Sukuk Insurance Policy.

Economic Context

In last July 2024, Algeria has gained back its position within the uppermiddle income category under the World Bank’s country income classification. The merits of this classification invoke the advances made by the country in “economic and human development, investing in infrastructure projects and introducing redistributive social policies that alleviated poverty and significantly improved human development indicators.”

A recent World Bank report highlighted Algeria’s “strong” economic performance in 2024. Growth in the first half of the year reached 3.9 percent, driven by “resilient” agricultural output.

Algeria is the largest country in Africa and the third largest economy in the Arab world. Aiming at addressing the predominance of the hydrocarbons in the economy which counts for almost 95 % of exports and 14% of GDP, Algeria has taken major steps to diversify its sources of revenues and improve employment prospects since 2020.

New laws on Hydrocarbons, on Investment, and on Money and Credit have been promulgated, lifting restrictions on the foreign ownership of domestic firms, to boost foreign and domestic investment. The country has clearly adopted a transition strategy towards private sector-led growth, rationalized public-spending, optimized imports and further developed non-hydrocarbon exports.