Technology and digitalisation possess significant potential in addressing the increasing demand for safe and nutritious food, efficient natural resource management, fostering high-quality productivity growth, and contributing to the attainment of the UN Sustainable Development Goals (SDG) Agenda. But the state of digitalisation in agriculture, water, and food systems in low-and-medium-countries (LMICs) in particular, varies widely, with ongoing efforts to leverage technology for sustainable development. Maher Salman, Team Lead, Agricultural Water Management, Food and Agriculture Organization (FAO) of the UN, in an exclusive interview discusses the importance of digital innovation in agriculture, water management, and building resilience in food systems, and emphasises its distinctive capabilities to bridge the rural-urban gap, create employment opportunities, enhance resilience in rural areas, and empower youth and women by providing access to information, technology, and markets.

ICIEC Quarterly Newsletter: Technology is critical to affecting change and driving development. In agriculture, it is said that digitalisation could be a game changer in boosting productivity, profitability, and resilience to climate change. An inclusive, digitally enabled agricultural transformation could help achieve meaningful livelihood improvements inter alia for smallholder farmers and pastoralists and could drive greater engagement in agriculture of women and youth and employment. What is the state of digitalisation in agriculture, water, and food systems in the low-and-medium-income countries (LMICs)? What is the economics of digitalisation in agriculture?

Maher Salman: Technologies and digitalisation possess significant potential in addressing the increasing demand for safe and nutritious food, efficient natural resource management, and fostering high-quality productivity growth. Furthermore, they play a crucial role in ensuring inclusivity and contributing to the attainment of Sustainable Development Goals. Digital innovation in particular has distinctive capabilities to bridge the rural-urban gap, create employment opportunities, enhance resilience in rural areas, and empower youth and women by providing access to information, technology, and markets.

The state of digitalisation in agriculture, water, and food systems in low- and medium-countries varied widely over the most recent years, with ongoing efforts to leverage technology for sustainable development. Digitalisation in these sectors holds significant potential for addressing key challenges linked to agricultural development, and hence to broader economic growth for several countries whereby agriculture is the leading sector. The status of digitalisation in these contexts is dynamic and shows both opportunities and challenges.

The adoption rate, for instance, varies across regions and countries, whereby some areas have made significant strides, while others may be lagging due to factors such as infrastructure limitations, education, and access to technology. Furthermore, technology in agriculture is becoming more and more a critical aid in decision-making. The collection and analysis of data is increasingly informing management processes, as well as investment decisions.

The economics of digitalisation in agriculture, on the other hand, involves a delicate balance of investment and returns. While initial costs are associated with adopting digital tools, the potential benefits include increased efficiency, improved market access, and elevated livelihoods for smallholder farmers and pastoralists. The inclusive nature of digitally enabled agricultural transformation also holds the promise of engaging a broader range of stakeholders, including women and youth, offering not only improved economic prospects but contributing to broader social and employment objectives.

In the face of economic slowdown and uncertainty, FAO has been playing a key role in advocating for the use of digital technologies to transform agrifood systems and agribusinesses. This involves advising on and promoting a policy agenda to address the digital divide and extend digital benefits on a mass scale, with a commitment to leaving no one behind. As part of its Digital Agriculture Program Priority Area, FAO has already initiated various programs to translate this vision into tangible support for its Member States.

To further advance this trajectory and bring digital innovation’s benefits closer to people, technology-based solutions need to be taken at scale and developed with inputs from final beneficiaries and local partners. FAO has been working in this direction, for instance, in Lebanon, with the development of the BlueHouse-Leb application that provides timely information on the irrigation needs of crops in unheated plastic greenhouses and thus contributes to improve the farm profitability and household-level food security of farmers.

What are the biggest threats, challenges and needs for sustainable agricultural development, quality land improvement and management, water and irrigation systems management, crop and land water productivity – in other words, for sustainable agri-food system transformation?

The sustainability and resilience of agri-food systems is seriously under threat unless current trends of drivers that are affecting them do change. An increase of food crises can be expected if we do not act immediately to transform the way we produce our food. Factors like the growing population and urbanization, economic uncertainties, poverty and disparities, conflicts, intensified competition for natural resources, are causing significant disruptions in socioeconomic structures and harmful effects on environmental systems.

Furthermore, the escalating threat of climate change, posing risks to crop yields, water availability, and overall land productivity poses serious challenges to the pursuit of sustainable agricultural development. Ensuring sustainable land management is hindered by factors such as soil degradation, deforestation, and inadequate land-use planning. The effective management of water and irrigation systems, critical for agricultural productivity, faces challenges related to water scarcity, inefficient irrigation practices, and the need for sustainable water resource governance.

Additionally, achieving optimal crop water productivity is impeded by the lack of access to advanced agricultural technologies, limited farmer education, and unequal distribution of resources. The overarching need lies in developing holistic approaches that integrate climate-resilient practices, advance sustainable land management, and promote efficient water resource utilization. The 2022 FAO “The Future of Food and Agriculture” report identifies four key triggers for the transformation of agri-food systems toward these objectives: improved governance; increased consumer awareness; better income and wealth distribution; widespread technological, social, and institutional innovations.

Moreover, the implementation of appropriate public strategies and policies, involving the active participation of all stakeholders are crucial. Addressing these challenges requires collaborative efforts, technology dissemination, policy support, and capacity building to foster a sustainable agri-food system transformation that is resilient, equitable, and environmentally sound.

The world is plagued by a cornucopia of negative metrics which tend to undermine progress towards achieving the 17 UN SDGs, of which sustainable agriculture, food security and universal digitalisation are key goals. I refer to policy inertia; lack of convergence on trade policies and tariffs; hidden protectionism through subsidies and other barriers to market entry; national interest; supply chain disruptions, land degradation and water pollution due to conflict, civil unrest, terrorism, polluting heavy industries, illegal mining, and logging; rising inequalities, and of course the impacts of the Covid-19 pandemic. What is the real economy, social, health and opportunity cost lost, and how do we future proof such challenges?

The number of challenges indeed poses formidable obstacles to the attainment of the Sustainable Development Goals, particularly in the domains of sustainable agriculture, food security, and universal digitalization. As pointed out by the UN Secretary-General and confirmed by the FAO report “Tracking Progress on Food and Agriculture-related SDG Indicators 2023”, many SDGs are off-track, including those to which agri-food systems are expected to contribute.

Issues like policy inertia, divergent trade policies, and hidden protectionism through subsidies are impeding global progress. Additionally, disruptions in supply chains, land degradation, water pollution from various sources including conflict, civil unrest, terrorism, and polluting industries intensify the complexity. The exacerbation of inequalities and the profound impacts of the Covid-19 pandemic further compound these challenges. The real costs, spanning the economy, society, and health sectors are highly significant, but so are the opportunities.

To future-proof against these challenges, a comprehensive approach is needed. This involves fostering international collaboration to address policy gaps, promoting transparent trade policies, and develop management and technical capacities of stakeholders at different levels. Moreover, investing in resilient supply chains, sustainable practices, and leveraging digital technologies for equitable access to resources are crucial steps. Building robust multipurpose infrastructures for both health and agricultural uses, and implementing social safety nets can enhance resilience, ensuring a more inclusive and sustainable future despite the multifaceted challenges we are confronted with.

The role of water is highlighted in the theme, “Water is life, Water is food. Leave no one behind,” of World Food Day 2023. There are over 2.4 billion people in water-stressed countries and 600 million reliant on aquatic food systems who face pollution, ecosystem degradation, and climate change impacts. Water scarcity, shortages and rationing are on the increase, and no country, irrespective of economic status and wealth, is spared. How did we get it so wrong, and in a world of poly-crises with competing demands for finance, how are we going to finance the remedial mechanisms required?

The thematic emphasis posed on water in this year World Food Day underscores the critical role of water in global food security. The statistics of over 2.4 billion people in water-stressed nations and 20% decline in the availability of freshwater resources are alarming. The escalating challenges of water scarcity, shortages, and accessibility are pervasive, and affect populations across nations and along economic spectrums. The question of how we reached this critical juncture prompts reflection on past resource management and policy decisions. In the contemporary context of poly-crises and competing financial demands, financing the necessary remedial mechanisms becomes a paramount concern.

Addressing water-related challenges requires innovative, collaborative solutions, a reallocation of financial resources, and a commitment to sustainable practices to ensure equitable access to water, safeguard aquatic ecosystems, and mitigate the impacts of climate change. The urgency of the situation calls for a global commitment to responsible water management, transcending economic boundaries to leave no one behind in the quest for water security and sustainable food systems. Agriculture, as the largest consumer of freshwater, has the biggest potential for impact, by changing the ways we produce our food.

In terms of governance, we need to strengthen partnerships between governments, researchers, business, and civil society to design science and evidence-based policies and improve coordination among sectors for better planning and management of water resources. As for financial solutions, more investment are required to enhance the efficiency of water resources and the development of irrigation systems based on ground-truth data, to be made available through accessible knowledge platforms.

Global water demand is likely to grow in the next three decades due to agriculture intensification, population growth, urbanization, and climate change. In water-stress regions, future demand will require the reallocation of 25 to 40 percent of water from lower to higher productivity and employment-oriented activities. These reallocations are likely to come from the agriculture sector due to its high share of current water use. Are you confident that new actions such as Smart Irrigation, Smart Wash, Land and Water Rehabilitation, Soil Enrichment will help to enhance increase water use efficiency, especially in irrigation, and enhance agricultural production and productivity?

The projection of increasing global water demand over the next three decades, driven by factors such as agricultural intensification, population growth, urbanization, and climate change, underscores the imperative for innovative solutions. The World Bank estimates that between 25 to 40 percent of water will need to be re-allocated from lower to higher productivity and employment-oriented activities in water-stressed regions.

Agriculture, once more can play a pivotal role and the FAO Strategic Framework hence indicates the need to increase global agricultural production by at least 40 percent by 2050, given the limited availability of water resources. Initiatives like the ones mentioned holds promise in enhancing water use efficiency and boosting agricultural production and productivity. In particular, the Smart Irrigation-Smart WASH approach, which was promoted under my lead by the Land and Water Division of FAO, addresses the concept of multiple water use and proposes solutions to enhance irrigation and provide WASH facilities to vulnerable communities, thus, responding to the critical needs in times of pandemic crisis.

With the Covid-19 emergency behind us, our focus is redirected to irrigation and its development to support the most efficient management of water resources. The “Irrigation Mapping of need and potential” initiative aims at supporting countries to mobilize sufficient resources for irrigation development and to sustain sound irrigation strategies with well-justified, prepared, and targeted action plans.

The objective is to ensure that irrigation meets actual needs, leverages untapped potential, and accommodates potential future scenarios, planning and decision-making processes. The initiative is developed by FAO through a broad partnership, including global and national stakeholders who share similar concerns about the need to enhance irrigation efficiency and are ready to promote effective solutions in countries worldwide.

In one of your recent papers, ‘Enabling pathways for intensifying drought finance flows’, you seem to suggest an important correlation between digitalisation and financial actors and recipients, and information management as the enabler of this process. Technology needs assessment, you stressed, can lead to the identification of bankable projects and support investors in establishing portfolios. You also mention customer clustering and value chain management. Making projects bankable, especially in drought prevention and mitigation is dependent on a whole range of metrics which are not readily evident in LMICs – credit enhancement, de-risking solutions, integrated policies and so on. Given that droughts are an increasing phenomenon in FAO member states, what is the outlook for increased drought finance and underwriting of the associated risks?

The report is formulated under the framework of the “Enabling Activities for Implementing UNCCD COP Drought Decisions.” project, executed in partnership with the United Nations Convention to Combat Desertification (UNCCD) and financially supported by the Global Environment Facility (GEF).

The primary focus of the publication is to delve into the complexities, alternatives, and mechanisms associated with drought finance. It is meant as a contribution to the creation of a conducive framework for the comprehensive management of drought, aligning with the overarching goal of integrated drought management. In the publication a number of short-term and readily implemented strategies are presented as pathways to drive drought finance forward, which include information management, digitalization, drought awareness, technology needs assessment, customer clustering and value chain management.

Recognizing the complexities inherent in drought prevention and mitigation projects, such alternative enablers of drought finance should be considered, especially in low- and middle-income countries (LMICs), where metrics like credit enhancement, de-risking solutions, and integrated policies are not always available. The growing recognition of the urgency and severity of drought occurrences confirms the need for increased drought finance and underwriting of associated risks, but the outlook is still far from the requirement.

Digitalization, coupled with innovative financial instruments, has the potential to unlock new avenues for financing. Moreover, the focus on customer clustering and value chain management contributes to creating a conducive environment for making drought-related projects more bankable. The imperative lies in sustained collaboration, international partnerships, and continued efforts to bridge financial gaps, ultimately fortifying the resilience of member states in the face of escalating drought challenges.

Digitalisation is a source of new growth and new efficiencies but also of new risks. The talk is about smart agriculture, precision agriculture and building agri-resilience through greater digitalisation. Risks include policy, market, water, investment, technology, cyber and insurance risks. At the same time, increased dependency on digital infrastructure especially in large-scale food systems, makes such assets more vulnerable to business interruption and cyberattacks. How do you mitigate these risks, especially for LMICs? Is targeted involvement and innovation of credit and investment insurance a potential answer?

FAO promotes inclusive and adapted innovative technologies, including digitalisation for sustainable production and improved market access, as key accelerators for the sustainable transformation of agri-food systems. There is considerable optimism that the integration of digitalization into agri-food systems, encompassing aspects like input management, disease control, supply chain management, and automation, holds the potential to enhance operational efficiency and concurrently reduce environmental impacts.

The infusion of information as a valuable resource has paved the way for big data platforms to enter the agri-food landscape, however, potentially assuming dominant positions. The issue has progressively come under the UN radar, especially for LMICs, as highlighted in the 2020 Report by the Secretary-General. This transition has given rise to novel and disruptive business models, particularly evident in the shifts observed since the onset of the COVID-19 pandemic.

However, concerns have emerged regarding the concentration of both big data and analytical capabilities in the hands of a select few entities. Without appropriate regulation, this concentration threatens to accelerate power imbalances, foster greater inequality, and marginalize impoverished and unskilled workers. Rural families and farmers, in LMICs and worldwide, are particularly at risk, as they lack the digital competences to stay updated in increasingly digitalized food markets and their employment opportunities are limited. In the light of these considerations the importance of carefully managing the integration of digital technologies to ensure equitable outcomes in agri-food systems emerges clearly, and so does the need to keep looking for suitable answers.

Global Trade and Digitalisation Prospects – Growth but Slower Growth

Global trade has supposedly been a force for economic recovery, resilience and near normalisation in the wake of a receding COVID-19 pandemic. But in 2022, says the latest World Trade Statistical Review (WTSR) 2023 of the World Trade Organisation (WTO), global trade has lost momentum, largely due to the supply chain disruptions due to the conflict in Ukraine and global economic shocks, including high inflation, the inevitable monetary tightening, and widespread debt distress. But can digitalisation and technology kick start trade and FDI flows recovery to pre-pandemic and its associated economic stability levels in a world of increasing and polymorphous uncertainties? Mushtak Parker explores the latest developments and prospects for digitalized global trade, especially in ICIEC member states.

There is no doubt that the prospects for global trade and investment over the short-to-medium term at best, are mixed, ranging from subdued to weak growth given the numerous downside risks exacerbated by the on-going conflict in Ukraine and, in recent weeks, the conflagration in the Middle East.

“Prior to the COVID-19 pandemic,” says WTO Director-General Ngozi Okonjo-Iweala, “we were accustomed to strong growth in global trade, which typically exceeded the rate of GDP growth. Even at the height of the pandemic, trade remained relatively resilient, and we saw a powerful rebound in 2021 as the global economy reopened and economic activity picked up. Since 2022, we have been following a different trajectory, with slower trade growth due to the disruption to supply chains in, for example, the energy and agricultural sectors as a result of the Russia-Ukraine war, and due to broader geopolitical tensions elevated global inflation and high interest rates, among other causes.”

Despite these shifts, she adds, the role of trade, as well as trade and supply chain finance products, is more important than ever. As the geopolitical and economic environment becomes more challenging, access to liquidity and risk mitigation is increasingly valued. In addition, the desire – and need – to digitise has accelerated innovation in the trade and supply chain finance space. Her optimism that “global trade growth has remained positive,” on the back of a slow-down in its underlying growth trajectory, is tempered by the stark reality that trade growth remains weak in the near term into 2023 due “to numerous downside risks, from geopolitical tensions to potential financial instability, which are clouding the medium-term outlook for both trade and overall output.”

Data dichotomy and overload lends itself to a morass of interpretations enough to suit almost any narrative in this highly complex global trade matrix. Take, for instance, the ‘volume versus value’ metric across a spectrum of cohorts – merchandise trade, intermediate trade, trade in goods and services, trade in manufacturing goods and so on. In volume terms, world merchandise trade rose by 2.7% in 2022, which is well below the 12.4% growth in value terms. This was largely reflected by the effect of high global commodity prices, which continues to affect consumers all over the world, but disproportionately in developing countries, as a cost-of-living crisis continues to bite because of stubborn food and energy price inflation. Trade in goods and services amounted to US$31 trillion in 2022, a 13% rise year-on-year. While trade in goods exceeded pre-pandemic levels already in 2021, trade in services caught up in 2022.

Any complacency over a receding pandemic and its impact on global trade too could be misplaced. The latest World Health Organisation (WHO) update on COVID-19 on 3rd August reported over one million new cases and over 3,100 deaths globally in the month of July 2023. The pandemic, at the end of July 2023, has seen over 768 million confirmed cases and over 6.9 million deaths globally. “Currently, reported cases do not accurately represent infection rates due to the reduction in testing and reporting globally. During this 28-day period, 46% (107 of 234) of countries and territories reported at least one case to WHO – a proportion that has been declining since mid-2022,” said WHO.

For a multilateral insurer such as ICIEC, global trade should also be considered in the context of food security, nutrition and global hunger – helping to alleviate it in member states, some of which are the poorest on earth, being a core mandate. The latest State of Food Security and Nutrition in the World (SOFI) report, published jointly in mid-July by five UN specialized agencies, reveals that 735 million people are currently facing hunger, compared to 613 million in 2019. This represents an increase of 122 million people compared to 2019, before the pandemic.

“If trends remain as they are, the UN Sustainable Development Goal 2 of ending hunger by 2030 will not be reached. Indeed, it is projected that almost 600 million people will still be facing hunger in 2030. While some areas have made some progress in hunger reduction, there are many places in the world facing deepening food crises. Africa remains the worst affected region with one in five people facing hunger on the continent, more than twice the global average,” concludes the SOFI report. Similarly, FAO (the Food and Agriculture Organisation of the UN) recently warned that global food commodity prices rose in July, influenced by the termination of the Black Sea Grain Initiative and new Indian export restrictions on rice.

African Challenges and Arab Development Finance Support

Not surprisingly, least-developed countries (LDCs), especially in Africa, in general, are faced with the biggest challenges in trade flows and dynamics, beholden to anachronistic world trade rules to the detriment of LDCs – a major failure of the global trade system. In 2022, for instance, resource rich Africa accounted for less than 1% share of world exports.

Even where exports of goods and services from LDCs increased by 31% between 2019 and 2022, this was more to do with a greater upside of 41% in value terms, once again reflecting higher global commodity prices. Africa’s trade deficit in intermediate goods (IG) – inputs used to produce a final product – shrank to US$4.4 billion in 2022. This is partly due to growth in its exports of IG, which totalled US$292 billion in 2022, an increase of 47% compared with its pre-COVID-19 level in 2019. Again, the rise in value terms is due to high commodity prices.

The fact that Africa accounted for only 14% of intra-African merchandise trade in 2022 (down from 16% in 2018) – the lowest of all the global regions – underlines the huge gap and challenges faced in realising the African Union’s Agenda 2063 vision of economic integration and inclusive socio-economic development on time, and the trade-led development ambitions of the African Continental Free Trade Area (AfCFTA), which seeks to bring together 55 African countries and create an integrated market of 1.3 billion people, with a combined GDP of over US$3 trillion.

A major development is the allocation of up to US$50 billion to help build resilient infrastructure and inclusive societies in the African continent by the Arab Coordination Group (ACG) at the recent Arab-Africa and Saudi-Africa Summits’ Economic Conference in Riyadh. The ACG is a strategic alliance that provides a coordinated response to development finance. Current members are the Abu Dhabi Fund for Development, the Arab Bank for Economic Development in Africa, the Arab Fund for Economic and Social Development, the Arab Gulf Programme for Development, the Arab Monetary Fund, the Islamic Development Bank, the Kuwait Fund for Arab Economic Development, the OPEC Fund for International Development, the Qatar Fund for Development, and the Saudi Fund for Development.

The ACG has been a long-standing supporter of African partner countries and has cumulatively invested over US$220 billion in the region to date. “We reaffirm our commitment to supporting the sustainable development of countries in Africa. Recognizing that the link between sustainable development and climate financing is cross-cutting and complex, the ACG reaffirms its commitment to scaling up financial assistance for climate change in line with the Paris Climate Agreement and to helping bridge investment gaps in energy access, including low-carbon energy sources, climate mitigation, adaptation, and resilience, as well as food security,” said the Group in a statement.

On the global GDP growth front, the outlook is equally mixed. Moody’s Investors Service, in its latest forecast, expects global G-20 growth to moderate in 2024 to 2.1% from 2.8% in 2023 and accelerate in 2025 to 2.6%, the firm said in its Global Macroeconomic Outlook 2024-25. “We forecast real economic activity in advanced G-20 economies to decelerate from an estimated 1.7% in 2023 to just 1.0% in 2024 and recover to 1.8% in 2025,” said Madhavi Bokil, Senior Vice President CSR, at Moody’s. “Growth in G-20 emerging markets will slow from 4.4% in 2023 to 3.7% in 2024 and 3.8% in 2025. Excluding China, G-20 EM growth will decelerate to 3.3% in 2024 from an estimated 3.5% in 2023 before accelerating to 3.5% in 2025.

The main reason, according to Dr Bokil, is that a Synchronous growth slowdown is expected in 2024 owing to the ongoing tightening in monetary and financial conditions in advanced economies. Traditional sources of strength will not buoy growth for too long – financial conditions have tightened even more in the last two months, which will further continue to dampen spending and investment. To him, economic strength across emerging market countries varies considerably, with some like India, Brazil, Mexico and Indonesia outperforming expectations, while outlooks for Türkiye and Argentina are highly uncertain.

Proliferation of Platform-base Trade

The 2023 ICC Trade Register Summary Report gives a more nuanced vista of the dynamics of global trade prospects, which will be increasingly subject to the impact of regulatory changes, especially due to the new reporting requirements from the Financial Accounting Standards Board (FASB), and the ongoing digitisation and future of platform-based trade. The geopolitical and macroeconomic challenges of 2022 have continued and have even intensified, in some cases, fueled by weak global growth, elevated inflation, and high interest rates. On the demand side, observes the ICC, consumption slowed from the post-pandemic bounce but remained strong. Households continued to spend the savings they had accumulated during the pandemic, while government spending continued apace, for example, in relation to the US Inflation Reduction Act (IRA).

On the supply side, while the shipping constraints of 2021 abated, supply chains remained disrupted, partly due to new trade policies across many countries. According to the ICC Trade Report, international goods trade flows reached US$23.8 trillion in 2022, up 10.7% from 2021. This was a softening in trade growth relative to the 25.5% jump in 2021, as the post-pandemic recovery eased in 2022. But this growth in 2022 was primarily driven by inflation rather than an increase in volume, as commodity prices jumped: in real, or inflation-adjusted, terms, goods trade flows grew only 3% in 2022 versus 2021.

The services trade tells a different story. Trade in services reached $6.8 trillion in 2022, up 14% from 2021, driven by strong growth across all regions in a continued post-pandemic recovery. Europe continues to be the regional leader, with a 53% share of global services exports in 2022. Services trade grew at a faster rate than goods trade in 2022, the opposite of what we saw in 2021 (where services trade grew at 19% vs. 26% for goods trade). This was due to a more sustained post-pandemic recovery for services than for goods. Its forecast for 2023 and beyond is to the point ‘Growth, but Slower Growth.’

Boston Consulting Group (BCG), which contributed to the ICC Trade Report, projects global exports of goods, excluding services and FX receipts, to reach US$23.8 trillion in 2023, rising by 4.6% to US$37.4 trillion in 2032.

Following the sharp increase in trade finance revenues by 28.2% in 2021 relative to 2020, BCG estimates that nominal trade and supply chain finance revenues grew a pace of 6.3% in 2021 to 2022, reaching a total of US$63 billion. The slowdown was due to softening of both volume growth and product penetration, as some businesses chose to go without trade and supply chain finance products to avoid the higher costs. A narrowing of margins also played a role in squeezing revenue growth in 2022.

The prospects for trade finance in 2023 are turning out to be a more challenging year. BCG forecasts nominal trade and supply chain finance revenues to fall by 7.4% in 2022 to 2023. Looking further ahead, trade and supply chain finance revenues are forecast to grow modestly in the year 2023 to 2024 before picking up and growing by 3.8% per annum from 2022 to 2032, reaching $91 billion by 2032 on a nominal basis. “Growth in open account products is slowing but is expected to remain strong as its speed, ease and cost effectiveness outweigh the risk mitigation properties of documentary trade. The ease of digitisation of open account also works in its favour,” said BCG.

BCG also stresses the importance of ongoing digitisation and the future of platform-based trade. Digitisation is going from strength to strength, with the majority of players investing heavily in their trade and supply chain infrastructure in order to:

- Modernise the customer experience,

- Provide new product functionalities across the full procure-to-pay value chain (e.g. pre-shipment finance, distributor finance, etc.),

- Enable greater platform and ecosystem connectivity in order to originate transactions where customers do business (rather than customers coming direct to bank),

- Enable greater modernisation to reduce cost and improve processing times, and

- Improve data and reporting and to enable balance sheet velocity of documentary trade through asset distribution which is expected to grow as legacy systems are replaced or upgraded, and data becomes more widely available.

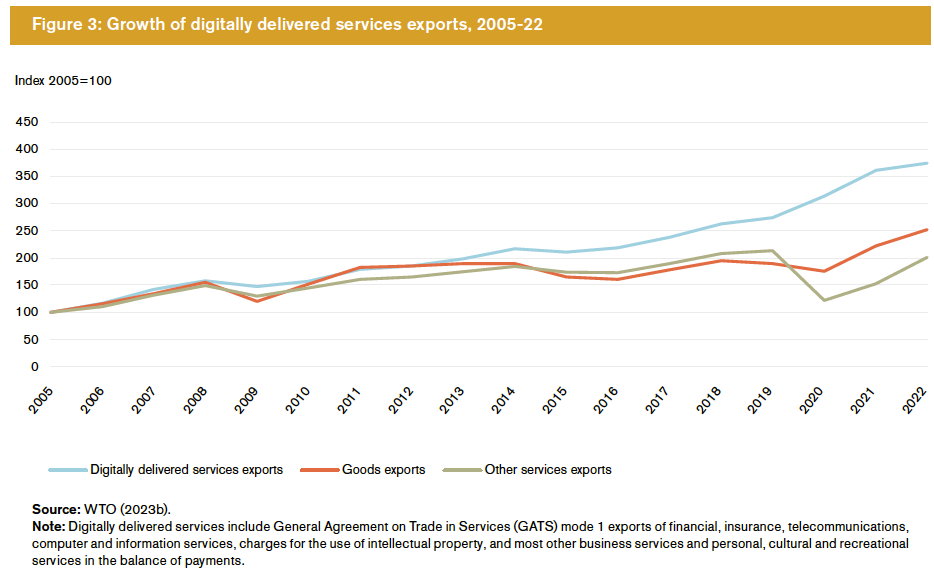

The real economy impact for ICIEC member states is implicit. According to WTO estimates, Bangladesh’s total exports of digitally delivered services for instance, have been growing by 15% annually since 2005, compared with 11% for goods, albeit from a very low base. Bangladesh has put digitalization at the core of its development. Around 14% of the online freelance global workforce originates and resides in Bangladesh, making it the top supplier of the online workforce in creative and multimedia services. As such, business-to-customer e-commerce is expected to grow by 18% per cent annually.

Digitisation has also been enabled by the growth in platform-based trade, where FinTechs and challengers are innovating on new ways to capture market share and scale. Many banks are now participating in digital trade platforms, e.g., for e-invoicing, payables automation, supply chain financing and working capital management. These platforms vary by geographic reach, product and client focus, and underlying technology, but the market has been somewhat bifurcated.

“While digitisation supports the shift to open account through the development of new products, it also improves the efficiency and security of documentary trade, underpinning its continued importance in the product mix. Moreover, digitisation not only facilitates broad industry growth but also supports inclusive growth. It is seen as key to reducing the “trade finance gap” for SMEs, which has widened recently due to higher interest rates,” maintains BCG.

Advances in Electronic Trade Documentation

The three major and potentially game-changing developments in the electronic trade documentation architecture are the Electronic Trade Documents Act (ETDC) 2023 in the UK receiving Royal Assent from King Charles the III on 20July, becoming legally effective on 20 September in an effort to make Global Britain’s trade with partners all over the world more straightforward, efficient and sustainable , the enhancement of the Model Law on Electronic Transferable Records (MLETR) , and the World Trade Organisation (WTO’s) initiative in including work on trade-related aspects of e-commerce as part of the organisation’s Joint Statement Initiative (JSI) on E-commerce in future WTO negotiations.

Perhaps the biggest potential leap change in the near-to-medium term may come in digital underwriting and digitalization in commercial insurance lines using targeted Generative AI, according to Swiss Re. It is important in the current climate of AI hype not to over-think nor over-talk the significance of AI in order to facilitate an orderly transformation to this very disruptive and yet inevitable technology.

“Along with the use of big data,” says Swiss Re, “AI is expected to be eventually used widely in risk assessment and underwriting. Given the level of confidence needed to deploy new technologies in underwriting, fully digitalised/automated AI and Machine Learning (ML) enabled systems are still not accurate enough for use at scale. This also means that algorithms cannot be relied on to fully replace traditional risk assessment, except in simpler lines of business such as motor. This said digitalisation can complement existing processes, including classifying and segmenting risk as finely as possible for more accurate risk pricing.”

Increasingly, commercial insurers are making use of digital technology in portfolio steering and risk selection. The benefits are important. “By leveraging third-party digital data overlaid with their own information,” stresses Swiss Re, “they can derive insights on potential risk accumulation, such as that caused by a concentration of high-value properties exposed to specific hazards. For example, the utility sectors’ liability exposure is increasing due to infrastructure that can spark fires. Utilities may operate in wildfire prone regions (eg, network operators, tree cutters). Using third-party digital data on, for instance, locating sources of ignition such as power lines and rail tracks, insurers have a deeper view as to areas of potential fire risk accumulation.”

The importance of the above developments cannot be ignored. The WTO initiative for instance, involves 89 (as of July 2023) member states, accounting for over 90% of global trade. These negotiations span a broad range of critical topics such as online consumer protection, electronic signatures and authentication, electronic contracts, transparency, paperless trading, open internet access, and data flows and data localization.

In this respect, the WTO Informal Working Group on Micro-and-Small-and Medium-sized-Enterprises (MSMEs) continues to discuss challenges for MSME access to digital trade, including cyber readiness, standardizing trade digitalization, and single windows (or access points) to access trade information. Recommendations like these, stressed the WTO, will be critical for increasing the inclusiveness of the international trade environment and should also be included in discussions at the WTO and in regional trade agreements (RTAs).

The benefits are real albeit incremental, and in need of urgent domestic and global trade system structural development, according to the world trade body. Automation and digitalization of production processes will continue because they increase productivity, allow firms to remain competitive in international markets, improve product quality and provide greater flexibility in responding to changes in the market.

Embracing a strengthened multilateral trading system through re-globalization would support inclusiveness by facilitating GVC-led industrialization and services-led growth. Growth in services trade, particularly digitally delivered services, needs agreements on services domestic regulation, e-commerce, and investment facilitation. WTO members can help facilitate a more inclusive global trading system by negotiating new accessions, extending their commitments, updating trade rules at the multilateral level, and working with other international organizations to ensure more people benefit from world trade.

Digitalization of trade could be a great equaliser and facilitator by providing new opportunities for those economies that have so far been left behind by allowing them to overcome some of the most important barriers to trade that they face, such as transportation costs and institutional disadvantages.

More importantly, it would also provide new opportunities for small firms, people living in remote areas, and women. Digital trade allows people globally to directly access international markets and supply their services even if there is no longer an industry domestically. Promoting more international cooperation, however, would need to be accompanied by requisite domestic policies without compromising the ethos of individual countries’ development agendas, as they play an important role in helping make globalization more inclusive.

ETDA’s £1.14 Billion Boost

There is no doubt that the biggest boost can come from the UK’s ETDA, with the British Government’s initial estimate that the UK economy is set to receive a £1.14 billion boost over the next decade through the “Innovative Trade Digitalisation Act.” With less chance of sensitive paper documents being lost, and stronger safeguards through the use of technology, digitalising trade documents is also set to give businesses that trade internationally greater security and peace of mind.

“The Electronic Trade Documents Act,” says Chris Southworth, Secretary General of the UK Chapter of the International Chamber of Commerce (ICC), “is a game changing piece of law not just for the UK but also for world trade. The act will enable companies to finally remove all the paper and inefficiency that exists in trade today and ensure that future trade is far cheaper, faster, simpler and more sustainable. This presents a once in a generation opportunity to transform the trading system and help us drive much needed economic growth.” The ICC estimates that 80% of trade documents around the world are based off English law, and this act serves as the cornerstone to truly digitalising international trade.

With English law being the very foundation of international trade, several Islamic finance contracts such as the Commodity and Syndicated Murabaha and Sukuk issuance, this act puts the UK ahead and in the lead of not only other G7 countries but almost all other countries in the world. The UK, says Minister for International Trade, Nigel Huddleston, is widely seen as a leader in digital trade, and this new act will make it easier for businesses to trade efficiently with each other, cutting costs and growing the UK economy by billions over time. “It’s exciting to see the power of technology being harnessed to benefit all industries, reduce paper waste and modernise our trading laws, an approach which the rest of the world will seek to follow,” he added.

Indeed, the Electronic Trade Documents Act recently implemented in the UK, according to the WTO, removes requirements for the majority of paper trade documentation. Varying degrees of progress are also being made towards implementation in the remaining G7 countries, with each taking unique approaches to amend and introduce legislation.

The Model Law on Electronic Transferable Records (MLETR) has already been in use since 2018 in a range of emerging markets, such as the UAE and Bahrain. The digitisation of trade finance documents has the capability to improve efficiency, reduce costs, enhance security, and diminish the extensive carbon footprint of paper documentation. More broadly, progress is being made to remove legal barriers to trade in many countries, such as France, Germany, the US under the African Growth and Opportunity Act (AGOA) and the UK.

The stakes are high for both AGOA-acceded countries and the US. Since its inception in 2000, AGOA has been at the core of US economic policy and commercial engagement with Africa. AGOA provides 32 eligible SSA countries with duty-free access to the U.S. market for over 1,800 products, in addition to over 5,000 products that are eligible for duty-free access under the WTO’s Generalized System of Preferences programme.

Harnessing the Next Phase of Digitalization Opportunities in Re-globalisation of World Trade and Investment

The post-Covid 19 acceleration in digitalization across economic and societal sectors presents not only a source of growth opportunities and new efficiencies, but also a spate of new risks for the insurance industry, especially the credit and investment insurance cohort. Oussama Kaissi, CEO of ICIEC, considers the state of digitalisation in trade, investment and insurance, new developments in closing the digital divide between developed and emerging economies, and the opportunities and pitfalls relating to over-reliance on digitalisation, as ICIEC member states seek to build on their trade and FDI potential, attractiveness and resilience.

The talk in the corridors of power at the World Trade Organisation (WTO) these days is that of re-globalisation instead of trade fragmentation. WTO’s 2023 World Trade Report (WTR) published in September stresses evidenced-based benefits of “broader, more inclusive economic integration as early indications of trade fragmentation threaten to unwind growth and development.” The findings, perhaps more importantly, highlight how re-globalization – or increased international cooperation and broader integration – can support security, inclusiveness, and environmental sustainability.

Trade, according to the WTO and industry organisations, has also become more digital, green and inclusive. The digital revolution has bolstered trade in digitally delivered services by sharply reducing the costs of trading these services. The value of global trade in environmental goods and services has increased rapidly, outpacing total goods trade, and global value chains (GVCs) have expanded to encompass more economies.

The UN Global Sustainable Development Report (GSDR) 2023 similarly identifies digitalization as one of the six dynamic conditions shaping the achievement of the 17 Sustainable Development Goals (SDGs) by 2030, to which ICIEC is committed to helping its 49 member states progress towards achieving the goals in their development agenda through its financing, credit enhancement and risk mitigation solutions. The other five conditions include climate change, biodiversity and nature loss, demographic change and inequality 7- all of which are also embedded in the policies and services offered by ICIEC. The Corporation, of course, is also a signatory to the Principles for Responsible Insurance.

As great as digitalisation is as a game-changing disruptor and a perceived force for socio-economic good given the latest ‘advancements’ in terms of Generative Artificial Intelligence (AI), Data Analytics, Blockchain, Internet-of-Things, Electronic Trade Documentation and so on, the reality of a digital divide between advanced economies and low-and-medium-income-countries (LMICs) is similarly evident.

Digitalisation as a Double-Edged Sword

But digitalisation like any other societal phenomenon can also be a double-edged sword. As such it needs careful and proactive harnessing, articulation, monitoring, regulation and enforcement, especially in the multi trillion-dollar finance, insurance, trade and investment universe. Inaction, delays and lack of adequate oversight could be costly and impact negatively on the global trade and investment ecosystem, which would give succour to disguised protectionism unfair trade and investment terms and conditions, which would exacerbate entrenched existing inequalities.

Digital value creation, says Swiss Re Institute (SRI), has led to an increase of insurance firms intangible assets, including digital data. At the same time, increased dependency on digital infrastructure makes such assets more vulnerable, for example, to business interruption and continuity, online fraud and scams, and malicious cyberattacks.

In a recent report titled “The economics of digitalisation in insurance”, SRI found that potential benefits across countries and throughout the insurance value chain are far from exhausted. Take, for instance Continental Africa, where some 27 IsDB member states are located, the 2023 WTR Projections based on the WTO Global Trade Model suggest that digitalization has the potential to increase African exports of services by over 7% per year or an aggregate US$74 billion from 2023 to 2040.

“Africa has been increasingly active in various joint initiatives undertaken by large groups of WTO Members,” explained WTO Deputy Director-General Angela Ellard in a recent speech. “Around 20 African members participate in our new investment facilitation for development agreement, designed to make developing countries more attractive for investment. Several African countries participate in discussions on e-commerce, and many are engaged in our e-commerce work program designed to bridge the digital divide and use digital trade as an engine for development. African countries are deeply engaged in discussions about how trade can contribute to economic sustainability. Today, 40% of funds under the WTO’s flagship Aid for Trade programme go to Africa.”

The challenges for insurers in general and credit and investment insurers in particular are clear and present. For ICIEC, uniquely the only Shariah-compliant multilateral insurer in the world, there are additional layers of compliance and operational risk metrics in play.

Digitalisation in Insurance

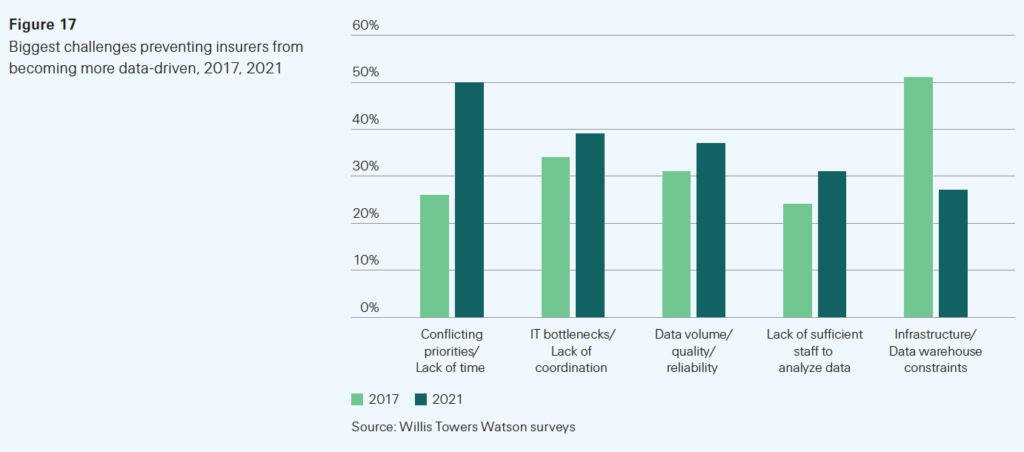

Swiss Re Institute (SRI), in “The economics of digitalisation in insurance” report, rightly stresses that digitalisation enables insurers to monitor, mitigate and price risks more efficiently, allowing for more tailored insurance solutions that can help close insurance protection gaps. Hence its call for “insurance innovation” and warning against any complacency and orthodoxy. In this respect, insurers are targeting a 3–8 percentage point improvement in loss ratios and savings of 10–20% in other parts of the value chain through digital transformation.

In the report, SRI, in fact, introduced the Insurance Digitalisation Index (IDI), which tracks the progress made in 29 sample countries with respect to the digitalisation of their insurance markets. South Korea came out on top of the index, followed by Sweden, Finland and the US. “While advanced markets with strong physical infrastructure and high internet access rates have made the most progress in digitalising their economies and insurance sectors, emerging markets should benefit from faster catch-up growth because they can jump straight into adopting newer digital technologies rather than transitioning from legacy systems,” stressed the report.

Another initiative aimed at bridging the gap between standards and adoption within the supply chain finance and insurance industry is the recent launch in Dubai by the International Chamber of Commerce (ICC) UAE Chapter of the ICC Digital Standards Initiative (DSI) as part of its expanded digital standards recommendations under its current Key Trade Documents and Data Elements (KTDDE) practice.

“The DSI’s continued efforts to expand the understanding of digital standards in international Trade,” explained Robert Beideman, Vice-Chair of the ICC DSI Industry Advisory Board, “represents a significant step forward in streamlining global commerce. By promoting data reusability and consistency across supply chains, we are facilitating more efficient and secure transactions for businesses across the globe.”

Despite the rapid digital transformation of the insurance industry, accelerated by recent advancements in cutting-edge technology, the consensus is that there are still significant potential and growth opportunities to make insurance more accessible and affordable for consumers, which behoves insurance providers and guarantors to continue investing in innovative solutions and adapting to emerging risks.

For consumers, says the SRI, online marketplaces lead to greater price transparency, present multiple insurance products and providers in a single place and allow customers to seamlessly complete the onboarding process online, making insurance more accessible and affordable. Aside from distribution, investments in insurance technology have shifted towards efficiency gains and improving underwriting and claims.

Resilience as a Function of Digitalisation

Indeed, Jerome Haegeli, Group Chief Economist at Swiss Re, maintains that there is a positive correlation between resilience and digitalisation. For society, he adds, digitalisation is a force for giving more people access to insurance and thereby closing protection gaps. For insurers, gains from better underwriting, risk mitigation and risk measurement from the digitalisation of insurance improve the quality and efficiency of their work.

The digitalisation of the wider economy, will also create new risk pools, opening up opportunities for insurers, especially in sharing-economy business models, which have resulted in fundamental shifts in operational risks and liabilities that require innovative insurance risk transfer solutions. With the shift from producing physical goods to providing information and services, the global value of intangible assets of listed companies has increased fivefold over the past 20 years, to US$76 trillion in 2021. Close to 80% of that value remains uninsured.

As such, insurers will need protection against digital risks, for example, business interruption and cyber risks, as well as the emerging liability risks related to AI. Cyber security, says Swiss Re, is a key concern for businesses globally, as reflected by the rapid growth in demand for cyber insurance. Swiss Re Institute estimates global cyber premiums will reach US$16 billion in 2023, up 60% from 2021 and US$25 billion by 2026.

Some key takeaways for insurers, according to the Swiss Re Institute, as they develop their digitalisation strategies going forward include:

- The impact of digitalisation is mis-measured which gives an underreporting of product structures, pricing, progress, challenges and market awareness and penetration.

- While workplace technology, in general, improves productivity by saving labour input, for example, through automation, the socio-economic costs can be huge. This raises the prospect of “technological unemployment”, which could put strains on existing unemployment insurance and worker’s compensation schemes.

- The correlation between the introduction of digital technology and disinflationary impact, although increasing digitalisation does not necessarily mean general deflation.

- Typically, countries that are more digital show greater resilience to health, mortality, natural catastrophes and agriculture, which affect LMICs disproportionately.

- The high value of intangible assets in business today are significantly uninsured: just an estimated 16.6% of intangibles are insured, compared with 58% of tangible assets. Digital transformation has given rise to new types of business models, most notably the sharing economy. Businesses will need more protection against the risk that intangible pose.

- Digitalisation has reshaped market dynamics, creating concentration risks. Dependencies on critical digital infrastructure create supply-chain risks. Many insurers themselves are exposed to digital infrastructure risks, although multilateral insurers such as ICIEC can mitigate these through reinsurance treaties and their special status with the ministries and agencies of member states.

- The first wave of digitalisation made the value chain more efficient. The next wave will better connect critical processes and improve digital connectivity across the processes, and thus increase operational efficiency, which potentially can reduce claims costs by 3-8%.

- Technology applications have enabled insurers to bring products significantly more quickly to market.

- Insurtechs, technological innovators in the processes of insurance business, are a good place to observe digitalisation trends in the industry’s value chain.

A Changing Global Landscape

The global trading landscape keeps evolving with advances in technology and science. The trade of tomorrow will be green and digital, and we need to make sure that our member states are able to transition smoothly to this new reality. ICIEC’s various policies, services and programmes offer an opportunity to build stronger partnerships for food security, digital connectivity, just transition to clean energy, and mainstreaming trade and investment.

Digital technology allows insurers to gather and process large sets of data using connected devices, data analytics and machine learning. This will allow more holistic and accurate risk assessments and better pricing of risks. Digital solutions can also automate standardised tasks, such as data collection and analysis for underwriting, driving down costs and ultimately leading to lower premiums. An important component of this transition includes capacity building of member states, their agencies, financial and insurance institutions and market players on the pivotal role of information sharing, business intelligence, digitalization and automation in supporting trade and investment decisions.

This initiative comes under the widely acknowledged capacity-building programme for users of the OIC Business Intelligence Centre (OBIC), whose thrusts are i) How digitalization and business intelligence can support trade and investment and the transformative potential of digitalization for economic growth and investment promotion utilizing digital transformation roadmaps for SMEs, and the digitalization of investment promotion services , ii) The importance of reliable credit information, reporting and sharing, and of digital IDs in fostering financial inclusion and trade promotion , and iii) The value of efficient utilization of statistical sources of information on credit, trade, and investment.

Addressing the Digital Divide

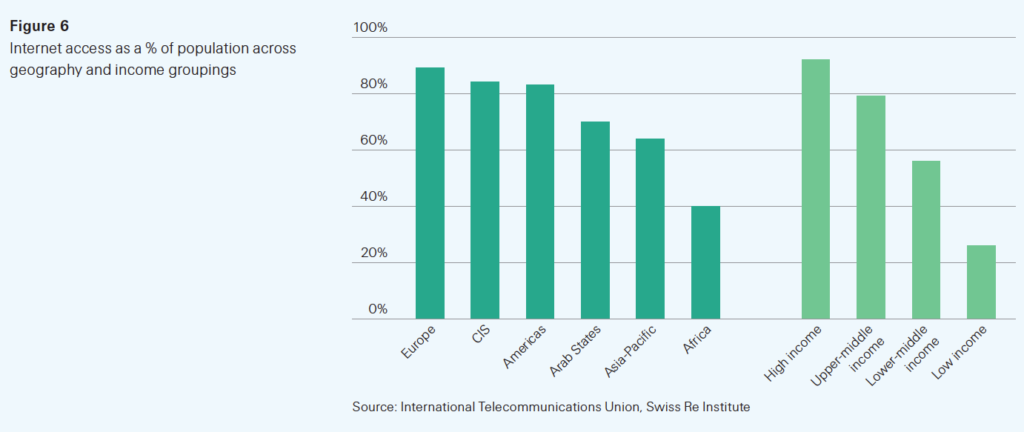

While the pandemic did give rise to an unprecedented acceleration in the digitalization of goods and services, including in the use of mobile telephony in e-commerce and payments where Africa is leading the world, all stakeholders, especially governments, multilaterals, banks, insurers, trade bodies, and digital and technology enablers and facilitators must never lose sight of the reality on the ground where, according to the International Telecommunication Union (ITU), although 66% of the global population or 5.3 billion people used the Internet in 2022, up from 54% in 2019, some 2.7 billion people globally have yet to access the Internet, including SMEs and the self-employed – often the backbone of LMICs economies.

“They are missing out on vital services provided digitally. Adequate and resilient infrastructure is a prerequisite for all the SDGs, and even before the pandemic, infrastructure was far from adequate. Some 1 billion people live more than a mile from a road, and 450 million live beyond the range of a broadband signal. With fiscal tightening and the end of low borrowing costs, infrastructure updates and investments are likely to be below what is needed. The war in Ukraine and the subdued economic growth in China is expected to continue to dampen the slow investment recovery following the pandemic,” emphasised the UN GSDR study.

As such, one way in which emerging markets can begin to close their digital divide with advanced markets at a structural level are through investments in internet accessibility. And here, the role of all stakeholders, including insurers, is not only in their immediate area of business, such as underwriting and providing guarantees as in the case of entities such as ICIEC, but also in supporting the harnessing of the wider digitalisation ecosystem, which primarily includes accessibility and infrastructure investment.

The good news is that digital transformation remains high on the insurance industry agenda. The initial focus was on distribution, seemingly to good effect. Insurers are experimenting with digitalisation across the value chain for efficiency gains. Today, 31 of the 50 largest re/insurers invest in Insurtech in pursuit of a first-mover advantage!

The UK Electronic Trade Documents Bill – a Gamechanger in Digitalized International Trade?

The UK Electronic Trade Documents Bill 2023 (ETDB 2023) completed its final Committee Stage in the House of Lords in February 2023 and is now with the House of Commons for final approval before going to King Charles III for Royal Assent, hopefully before the end of this year. Under the Bill, digital trade documents will be put on the same legal footing as their paper-based equivalents to give UK businesses more choice and flexibility in how they trade. Could ETDB 2023 evolve into a global governing model akin to the pre-eminent role English Law plays as the governing law for the documentation in the global bond and Sukuk market? What are the implications for Data Protection, Privacy, Credit and Investment Insurance and UK Trade Relations with OIC Member States? Mushtak Parker discusses the potential impacts of ETDB 2023 and prospects for global trade.

The imminent adoption of ETDB 2023 in the UK could not be timelier. One of the unintended consequences of the COVID-19 pandemic was the massive acceleration towards digitisation in almost all spheres of human activity, whether in e-Government, e-commerce, online banking and insurance, multimedia, data harvesting, healthcare, industry and so on.

Digitization has brought huge opportunities not only in reach, instant messaging, marketing, cost efficiencies and savings, and boosting trade and investment flows, but also for cybercriminals armed with a growing epidemic of scams, compounded by the apathy of the tech giants, who after all are the technological ‘facilitators’, albeit unintended, of online fraud and scams, and the shortcomings of regulators who are always a step or two behind the innovators and increasingly sophisticated cybercriminals.

In a world preoccupied by the sheer scale and pace of technological innovations in Artificial Intelligence, Metaverse and Blockchain, digitization and cybersecurity, especially in global trade and investment activity, must be a shared responsibility. But as Belgium-based SWIFT, the world’s leading provider of secure financial messaging services, “not all jurisdictions and regulators use the same terminology or have the same classifications when defining fraud and cybercrime. This can lead to fragmentation in an understanding of the data and statistics because they’re not always comparable.”

Technology, the World Trade Organisation (WTO) tells us, is a potentially empowering enabler of trade and investment, despite the tendency towards protectionism in times of geopolitical and economic uncertainty. As such, a defining moment will come when the UK’s Electronic Trade Documents Bill 2023 gets imminent Royal Assent and enacted in law. It will not only reduce the cost of trade transactions but also be good for the environment.

While this transformation to digital trade documents has taken some 131 years since the adoption of the Bills of Exchange Act in 1882, the UK government projects a major boost for the country’s international trade, already worth more than £1.4 trillion, and will reduce the estimated 28.5 billion paper trade documents printed and flown around the world daily. Business-to-business documents such as bills of lading – a contract between parties involved in shipping goods and bills of exchange used to help importers and exporters complete transactions currently have to be paper-based due to longstanding laws. According to the International Chamber of Commerce, digitalizing trade documents could generate £25 billion in new economic growth in the UK by 2024, and free up £224 billion in efficiency savings.

Policy Rationale

The rationale behind launching ETDB 2023 is simplicity itself. In their joint Impact Assessment (IA) of the Bill, the UK Departments for Digital, Culture, Media & Sports and for Science Innovation and Technology stress that “the operation of many documents important to international trade, including bills of lading and bills of exchange, is premised on their possession. The person in possession of the relevant document can claim performance of the obligation recorded in the document and can transfer the right to claim performance of that obligation by transferring (physical) possession of the document.”

However, in this fast-evolving digital age, there are deficiencies in the current legal position which prevent the move to electronic versions of the above documents. English law – like many other trade jurisdictions around the world – does not currently recognise intangible things as being amenable to possession. This means that electronic forms of trade documentation, which are considered to be intangible, cannot be possessed and cannot, therefore, be used in the same way as their paper equivalents. “This,” said the IA, “was not an issue when technology did not exist to make electronic documents with the same relevant properties. However, technology has now developed which can provide an electronic equivalent of a paper trade document. The legal system has not kept pace with this technological development. The proposed legislation will correct this problem, allowing electronic trade documents to have the same legal effects as their paper equivalents. Without (primary) legislative change, trade will continue to be paper-based and thus more costly, complex, and time-consuming than it otherwise could be.”

The IA assessed two options. Doing nothing, it concluded, would yield no additional benefits. Businesses would have to continue to deal with unnecessary costs, complexity and time delays (all of which have been exacerbated by the pandemic). Inaction could also diminish the primacy of English and Welsh Law as the governing law for international trade transactions, as traders may instead switch to using US or Singaporean laws to underpin their transactions. For many OIC countries with their historical, kith and kin, and diaspora relations with Britain, London as the global financial centre and the most proactive non-Muslim jurisdiction for Islamic financial transactions, including Murabaha and Sukuk, and the pre-eminence of English law as the governing law for the documentation of the above transactions in the international market, the implications could be important.

The chosen approach is to introduce primary legislation to recognise electronic trade documents on an equal legal footing to physical trade documents. “This allows for take-up according to the preference of firms and technology coordination across industries. Benefits include increased growth through improved trade efficiency.”

However, the adoption of the Bill will not necessarily see a rush to electronic trade documentation migration. Nor will it be a panacea to seamless trade documentation, as some have claimed. Only those businesses, says the UK government, that see benefits as outweighing the costs will switch to using electronic trade documents. It is expected that once larger businesses and organisations make the switch, then smaller firms will soon follow. ETDB 2023, says its promoters, “is an incredibly important piece of legislation, small, succinct, and simple with just one clear aim – to allow the digitization of trade documents.” Not surprisingly, there is no associated secondary legislation.

Monetised Benefits and Costs

These include:

i. The total costs saved by businesses that shift to electronic trade document systems, through saving on the costs and time associated with producing and handling these documents, or experience issues such as paper documents being lost or information being re-keyed incorrectly – which have until now been a significant cost to the business.

ii. The initial transition costs, for example, developing new internal processes, purchasing the required technological capabilities and training staff to use the new system.

iii. Familiarisation costs incurred by businesses, whether they ultimately adopt electronic systems or not.

iv. Ongoing costs associated with operating the electronic trade document systems, including continuous staff training and technology maintenance/upgrades.

Not surprisingly, there is no associated secondary legislation. The International Chamber of Commerce (ICC) is confident that the digitalisation of trade documentation is expected to lower transaction costs and promote greater efficiency, transparency and security in international trade. It stresses that there is a strong desire in industry to transition towards digitized ways of doing business.

Given the cross-jurisdictional nature of international trade, global legal reform is essential to facilitate the use of electronic trade documents. In recognition of this international coordination problem, the UN proposed a Model Law on Electronic Transferable Records (UNMLETR). However, whilst some smaller jurisdictions, such as Singapore and Bahrain, have enacted legislation consistent with the model law, no major economy is yet fully compliant. Given the extent to which international trade transactions (even those not involving the UK) are based on the Law of England and Wales, it is most likely that UK legal reform in line with UNMLETR would act as a model and significant catalyst towards global legal reform and the development of an electronic trade document ecosystem.

Under its 2021 G7 Presidency, the UK secured an agreement amongst G7 countries to work together to progress coordinated legal reforms in line with UNMLETR. The UK government commissioned the Law Commission of England and Wales to examine the provisions of UNMLETR and make recommendations on how to bring UK law into conformity, which has resulted in the current ETDB Bill. “This legislation is permissive and stipulates that business-to-business electronic trade documents which satisfy certain criteria should be treated as functional equivalents of their paper counterparts. The proposed reforms cannot be made in any other way than through primary legislation because there are no existing legislative powers which could be used to implement this measure to cover the range of trade documents covered by the Bill,” said the IA.

Data Protection Adequacy

There is one other important implication, including for OIC/ICIEC member states dealing with or through institutions in the UK. On 18 July 2023, the UK and Türkiye announced plans to begin talks on an updated free trade agreement (FTA). The deal would replace the existing UK- Türkiye FTA, which was rolled over when the UK left the European Union and doesn’t cover key areas of the UK economy like services, digital and data. The UK is the second biggest services exporter in the world – behind only the US, and the services sector contributes around 80% of the UK’s GDP.

“Türkiye is an important trading partner for the UK,” stresses British Business and Trade Secretary Kemi Badenoch, “and this deal is the latest example of how we are using our status as an independent trading nation post-Brexit to negotiate deals that are tailored to the UK’s economic strengths.”

Bilateral trade between Türkiye and the UK reached £23.5 billion in 2022 – up more than 30% from the previous year. “The new FTA is an opportunity to strike a 21st century deal that is better suited to the modern economies of both the UK and Türkiye, covering areas such as digital trade and services, and could also potentially lead to cheaper goods and more choice for UK and Turkish consumers,” she added.

Türkiye is a major supplier of goods such as vehicles, clothing and electrical machinery and goods to the UK, which is its 4th largest goods export market, in return for £6.4 billion of UK goods exports, including power generators and metals.

In terms of data privacy and transfer, Türkiye could be a beneficiary of London’s policy to grant prioritised countries data adequacy status so that UK-based organisations can transfer personal data to these countries without restrictions or safeguards, subject to them passing the impact assessment. South Korea is the latest country to be afforded this “Green Rated – Fit for Purpose” New International Data Transfers Adequacy status by the UK Department for Digital, Culture, Media (DDCM) and Sport after approval from the UK’s Regulatory Policy Committee. The Status is considered fit-for-purpose for various business sizes, including small and micro businesses.

According to the DDCM, the status proposal aims to reduce barriers and burdens to organisations transferring personal data to the Republic of Korea while providing trust and confidence that all citizens’ data rights are upheld. The proposal is expected to be net-beneficial to businesses as they would no longer be required to purchase International Data Transfer Agreements (IDTA) to send data to the above country.

Export, Insure and Thrive – KazakhExport Stresses the Integration of Islamic Finance into the National Agenda of Kazakhstan Can Lead to the Expansion of Credit Insurance

Of the six Central Asian Republics, Kazakhstan has enjoyed the most proactive partnership with the IsDB Group, having acceded to membership of the multilateral development bank in 1995 and of ICIEC in 2003. Since then, ICIEC has insured a total of US$7.2 billion for trade transactions in Kazakhstan. In addition, ICIEC, through its risk mitigation solutions – credit and investment insurance, guarantees and reinsurance – supports infrastructure development and projects in line with achieving the goals of the UN SDGs, the Paris climate agreement towards Net Zero and Kazakhstan’s Green Growth agenda. The Corporation enjoys an excellent relationship with KazakhExport, the national ECA of Kazakhstan. Kazakhstan, blessed with natural resources, is also seeking to diversify its economy away from reliance on hydrocarbons, and to boost exports, especially non-commodity products, both to neighbouring Central Asian markets and beyond. The signs are of much greater support from KazakhExport to local manufacturers and exporters and cooperation with ICIEC. Mr. Aslan Kaligazin, Chairman of the Management Board of KazakhExport, in an exclusive interview, discusses the importance of credit and investment insurance and cooperation with ICIEC as a driver of dynamic growth in the economy in an era of global trade tensions and economic uncertainties, and the supporting role of KazakhExport in accelerating the country’s export ambitions.

Aslan Kaligazin: The Export Insurance Company (KazakhExport) is a relative newcomer as an export credit agency established as a national company on 10th March 2017, whose sole shareholder is the National Managing Holding Company, Baiterek JSC. In the context of your Development Plan (2014-2023), what is the state of the credit and investment insurance culture in Kazakhstan, especially in a world in which new risks and uncertainties keep materializing?

We believe that in the face of the emergence of new risks and uncertainties, the culture of credit and investment insurance in Kazakhstan shows dynamic growth. I would like to note that within the framework of the National Development Plan (2014-2023) and with the forthcoming creation of an Export Credit Agency, KazakhExport made significant efforts to strengthen the credit and investment insurance culture and industry in the country.

In general, geopolitical and trade tensions around the world have affected many of the key markets for Kazakh exporters. However, such changes could also create opportunities for Kazakh businesses through economic diversification based on increased investment in the non-commodity sector. Therefore, it is important for exporting companies to improve the culture of trade insurance. This will ensure financial stability, protection against unforeseen losses and will promote the development of exports and investment.

In general, the growth of the culture of insurance and the level of risk management in companies, as well as the increase in the degree of confidence in development institutions on the part of exporters, have a positive effect on the development potential of KazakhExport, i.e. the potential involvement of Kazakh manufacturers in export activities will help increase the number of our company’s clients and the volume of government support measures provided.

According to your own figures, the volume of your support for Kazakh exporters increased by 27% to 259.1 billion tenge (US$580 million) in 2022 compared to 90.2 billion tenge (US$237 million) in 2018. This suggests a low starting base, but a huge potential for business opportunities across several market segments. What are your priorities for 2023 and beyond in the context of your own business strategy and objectives and Kazakhstan’s National Export Strategy and development agenda? What is the potential to increase the above figures substantially as the country accelerates its export strategy, its inward FDI requirements, especially to finance projects in key sectors, including mining, transport, agribusiness and infrastructure in general?

In 2023, KazakhExport will continue its main activities to support Kazakh exporters in the manufacturing sector, to implement sectoral measures for legislative improvement and present KazakhExport as a single operator for the promotion of non-commodity exports.

The main goal of the state policy in the field of exports is to diversify the export basket and ensure the growth of non-primary exports at a faster pace. As part of stimulating the export potential of Kazakhstan, as well as diversifying exports with a focus on high added value, a strategically important area of activity for KazakhExport will be strengthening of financial support for exporters.

As part of assistance in increasing the export potential, KazakhExport sets itself the goal of increasing the volume of supported noncommodity exports, which will be carried out through the implementation of such tasks as: expanding the range of services provided to support exporters and improving existing instruments of financial support for exports. To do this, we plan to constantly monitor the needs of the market, based on the needs of customers, taking into account the place and role of KazakhExport in supporting Kazakh exports. In general, in the implementation of the above goals, we see significant potential for a significant increase in the performance of our Company.